bymuratdeniz

General Overview

2022 has been a year of booms and busts for big energy. The onset of the war in Ukraine saw a spike in energy costs as the West sanctioned Russia. With barrels off the market and inflationary pressures rising, the energy industry became a political punching ball.

Apparently it was un-American for big energy, which had experienced a horrible few years of underperformance previously, to refuse ramping up drilling.

Forget the free hand of capitalism, this was an open attempt by the Biden government to force oil companies to drill. The irony was telling given his persistent Green New Deal sustainable energy mantra.

Apparently, there were not enough windmills to quell skyrocketing inflation. Big energy became the over-politicized whipping boy by politicians looking to score points and convince the public that inflation was unrelated to policymakers.

Continually demonized and chastised as big, bad polluting energy, it was natural that the supermajors shelved development projects and returned money to shareholders. This trend along with a progressively weakening dollar will be critical contributors to a supportive price environment. With little luck in convincing oil firms to drill, the Biden administration then saw it apt to drain the strategic petroleum reserve.

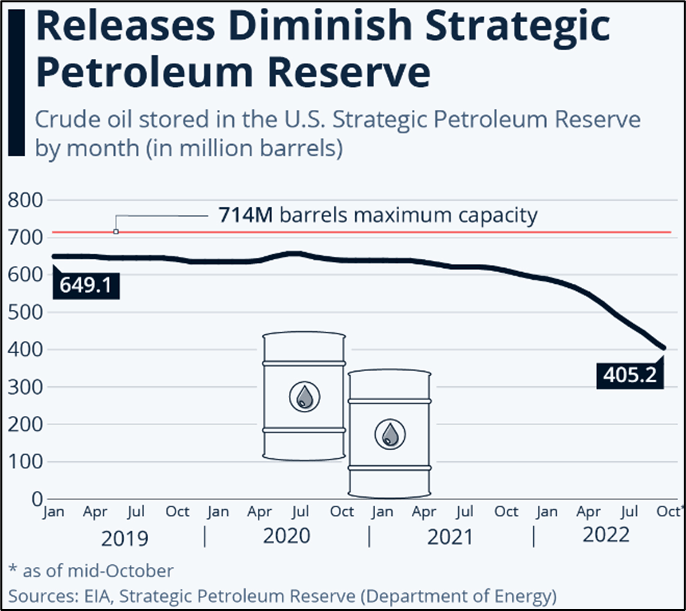

EIA

The strategic petroleum reserve has been drained by the current US administration as it tries to resolve extensive inflation.

From circa 650M barrels, the reserve was drained to around 400M, delaying the problem. Given that the strategic petroleum reserve was designed for emergencies such as war, the likelihood that the US government becomes a buyer of first order at a later stage is extremely probable. Would it be an open case of kicking the can down the road? Whatever the case may be, this too is supportive of energy prices in the future.

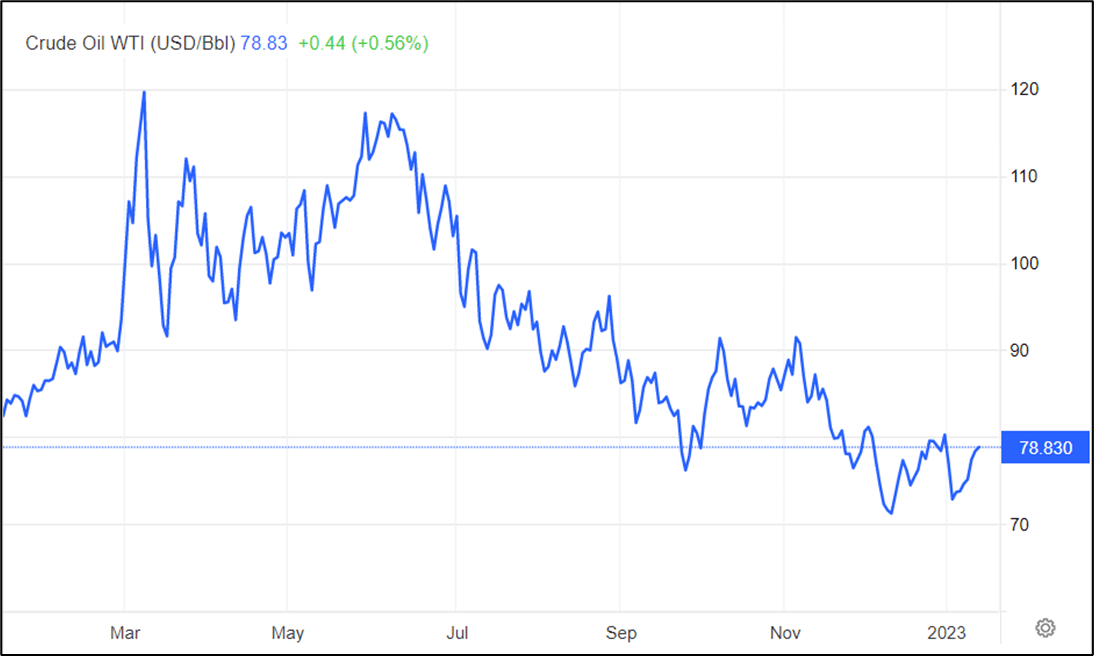

Trading Economics

After a post Ukraine boom, energy prices have tapered as the US dollar strengthened, risk assets weakened, and the global economy moved towards a recession.

China now appears to have dumped Draconian Covid lockdowns, bringing one of the biggest consumers back on the market. While the Chinese economy is presently in a holding pattern, the likelihood that energy consumption starts to rise remains strong.

Continued global conflict, the emptying of the SPR, the re-opening of the Chinese economy, the shelving of future energy projects and the weakening of the US dollar are a few of the reasons my outlook for the energy industry remains positive.

Product Overview

Direxion Daily S&P Oil & Gas Exploration & Production Bull 2x Shares (NYSEARCA:GUSH) utilizes derivatives and other securities of firms operating across global energy, including oil and gas exploration and production sectors. Derivatives such as futures and swaps provide the fund with its leverage.

Its objective is to provide 2x daily returns of the performance of the S&P Oil & Gas Exploration & Production Select Industry Index. As most energy securities are heavily correlated with returns in West Texas Intermediate, any position needs to be accompanied by an outlook on oil prices.

It is also important to grasp differences in the energy value chain, specifically between upstream exploration and downstream refining and petroleum distribution. Exploration tends to be characterized by a riskier but more profitable part of the value chain, with downstream activities characterized by lower value activities dictated by cost inputs in feedstock.

In times of low energy prices, downstream activities benefit from lower feedstock costs, boosting profit margins. However, this puts a natural break on exploration activity required to bring new projects online.

With the demonization of energy majors by politicians, watchdogs, and lobbyists, an increasing trend has been the shelving of new projects in favor of distributing returns to shareholders. This is likely to support future energy prices as growth in demand in not satisfied by new projects online.

Koyfin

The fund has proven to have volatile returns driven by the prolific use of leverage.

As the name suggests, this ETF should be traded “daily”. Its leveraged nature matched with daily resets and compounding mean that returns may not match those described in the fund prospectus. This is an extremely important trait of the fund.

Product Structure

The product is structured synthetically – meaning it resorts to OTC derivative contracts such as futures and swaps to replicate the return in the index. This implies counterparty risk linked to the make-up of the fund, as in times of extreme volatility, a failing of one of the counterparties would limit their ability to make good on the contractual obligations described in the derivative contract. This trait is characteristic of leveraged exchange traded funds.

Koyfin

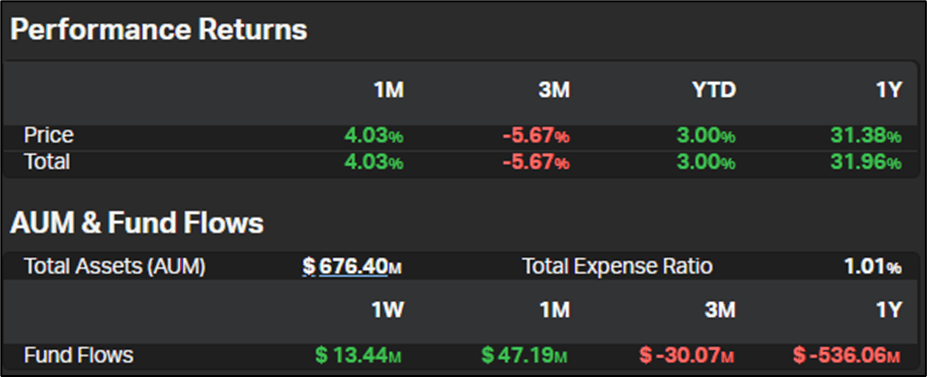

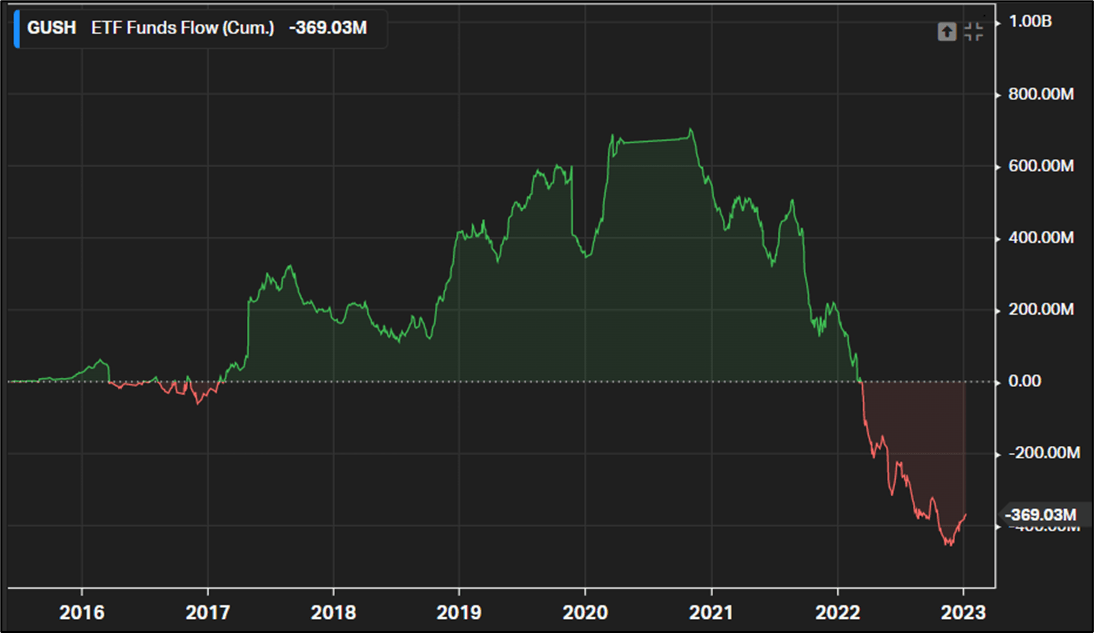

As oil prices have moderated, fund inflows have tapered. This is likely to change should any reversal in oil fortunes occur.

Fund inflows have dwindled as trades pull money out of the leveraged fund on the back of flatter energy prices. The $676M fund lost around $370M in 2022 – a meaningful chunk of assets under management.

Koyfin

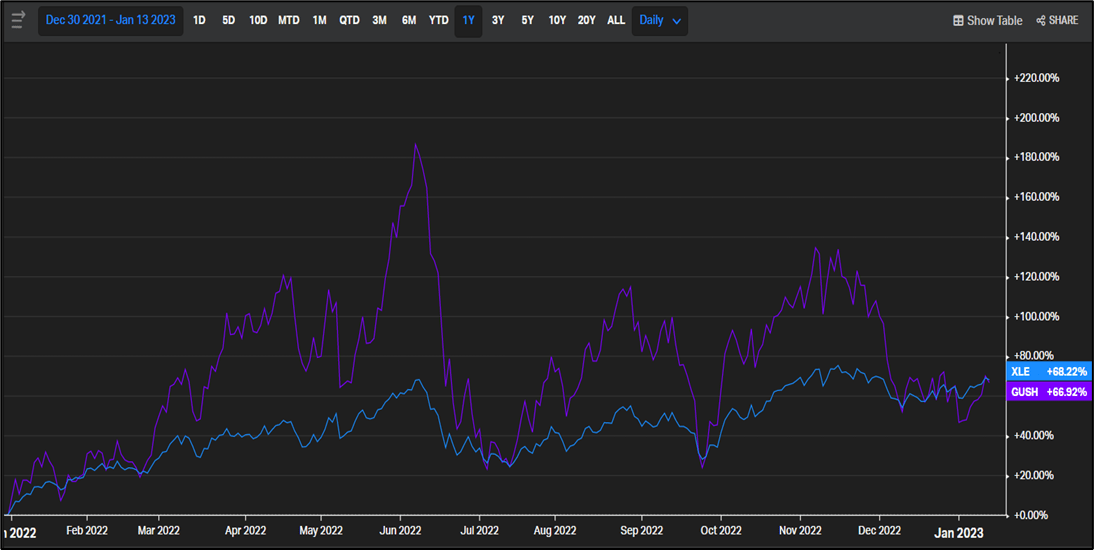

Returns over the last 12 months have essentially matched the more widely known XLE, yet leverage shows how volatile returns can be over that period.

While the fund aims to provide leveraged exposure to an index focused on energy exploration and production, history indicates that returns between the leveraged fund over the past year have simply tracked the renowned energy proxy (XLE) Both funds delivered circa 68% with the distinguishing factor being GUSH’s volatility.

Risk Profile

The risk profile of the ETF is common to other levered packages. Use of leverage is a major risk factor and should not be ignored. The way the leverage is generated is also a critical risk; synthetic instruments are traded over the counter between financial intermediaries.

Without a clearing house between the parties, the risk of failure of one in case of an exogenous shock to markets, and a consequent capitulation of the fund is possible.

The fund detains the “daily” badge, inferring short-term holding. Any holding beyond that period will provide less predictable returns as daily resets and compounding start to impact returns.

Derivative use is another key risk; the fund depends on the use of a wide range of derivatives to provide it its levered characteristics. All in, leveraged funds are extremely risky.

Make sure you carefully read the term sheet, understand product risks and are familiarized with leveraged before taking a position.

Spreadsheet developed by author

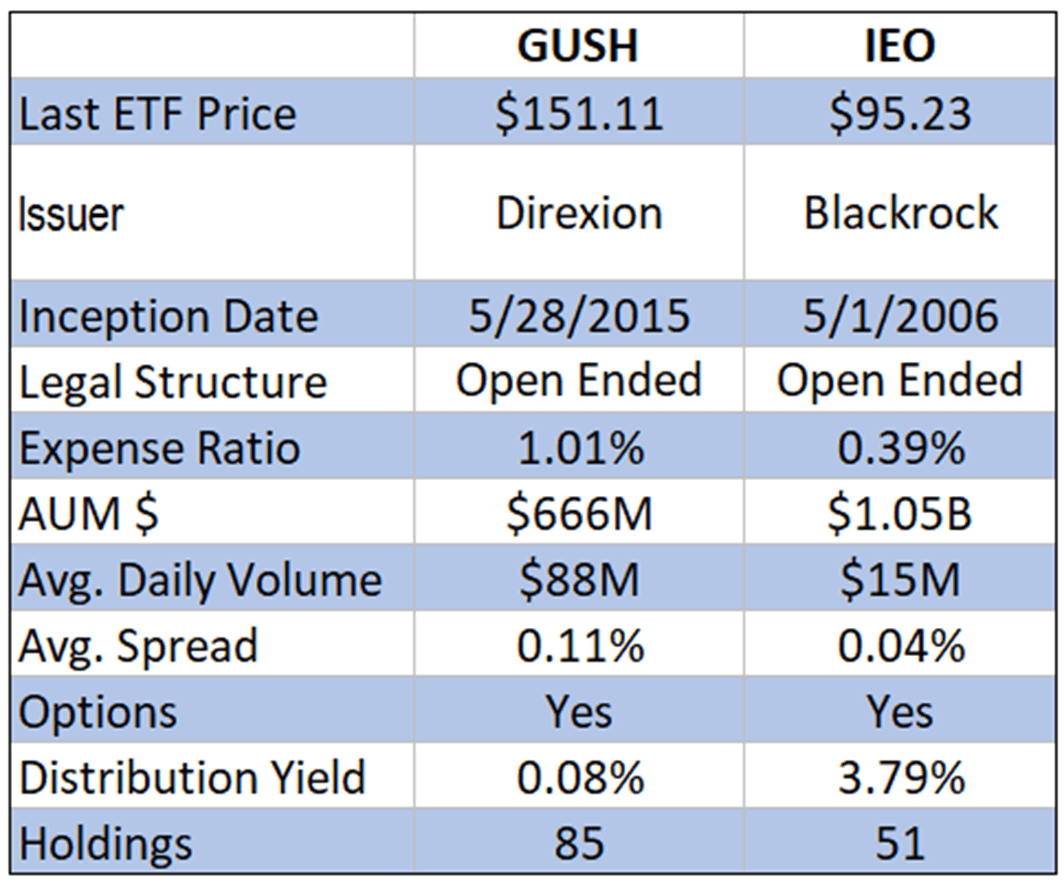

Comparative analysis GUSH v IEO

Key Takeaways

GUSH provides traders leveraged exposure to movements in global energy, by using derivatives to emulate accentuated price movements. Leverage is the key risk to the package, with daily resets meaning 2x returns become less predictable.

Ideal for a punctual directional trade on big oil, the ETF should be handled with care, regardless of the macro upside linked to big oil as the world slowly recovers from a global slowdown.

Be the first to comment