Dilok Klaisataporn/iStock via Getty Images

Thesis

With the 10-year yield exploding higher today (it is at 4.269% as we are writing this article) we are revisiting the leveraged short treasuries vehicle Direxion Daily 7-10 Year Treasury Bear 3X Shares (NYSEARCA:TYO). The fund is an inverse ETF tracking the ICE U.S. Treasury 7-10 Year Bond Index. As per its literature:

The ICE U.S. Treasury 7-10 Year Bond Index (IDCOT7TR) is a market value weighted index that includes publicly issued U.S. Treasury securities that have a remaining maturity of greater than seven years and less than or equal to ten years. Eligible securities must be fixed rate, denominated in U.S. dollars, and have $300 million or more of outstanding face value, excluding amounts held by the Federal Reserve. Securities excluded from the Index are inflation-linked securities, Treasury bills, cash management bills, any government agency debt issued with or without a government guarantee and zero-coupon issues that have been stripped from coupon-paying bonds.

The vehicle aims to provide a daily return equivalent to -300% of the return for the benchmark for a single day. The vehicle has a duration of 7.95 years. At the beginning of October, as we saw an artificial decrease in yields, we advised buying TYO:

10 Year Yields (Investing.com)

The rally in yields has been almost vertical! Up almost 70 bps in under 30 days is almost unprecedented. Today’s market is relentless, and it wants to get to a terminal rate faster rather than slower. As behind the curve the Fed has been, it has been able to rely on its messaging to get the market to tighten financial conditions for them. Just keep in mind that the current Fed Funds target is 3% to 3.25%!

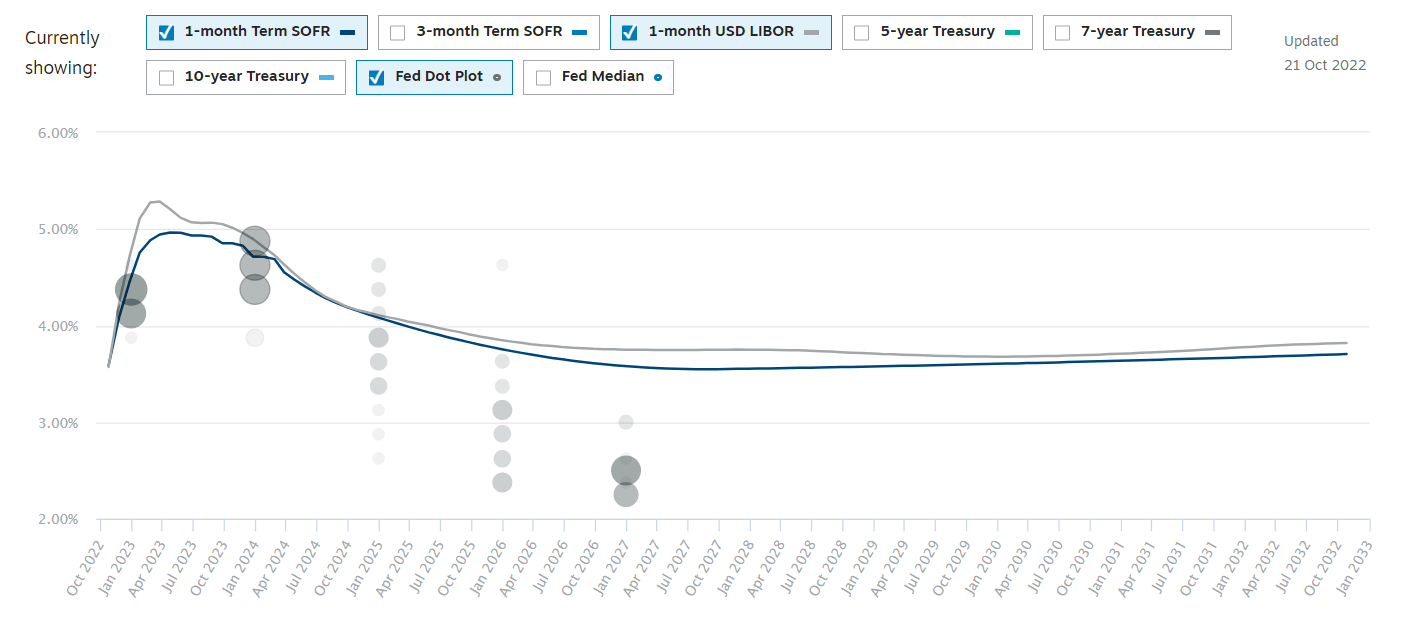

Inflation readings have not abated, hence the massive move up in the terminal rate. The market is now pricing in peak Fed Funds around the 5% mark:

Rate Curves (Chatham)

The rates market is forward-looking, so it tends to go where traders think the Fed is going to end up. Through its “dot plot” the Fed has signaled a terminal rate around 5%. The market priced in a “pivot” continuously until the last inflation read that came in above expectations. The front of the curve is now quite close to the terminal rate.

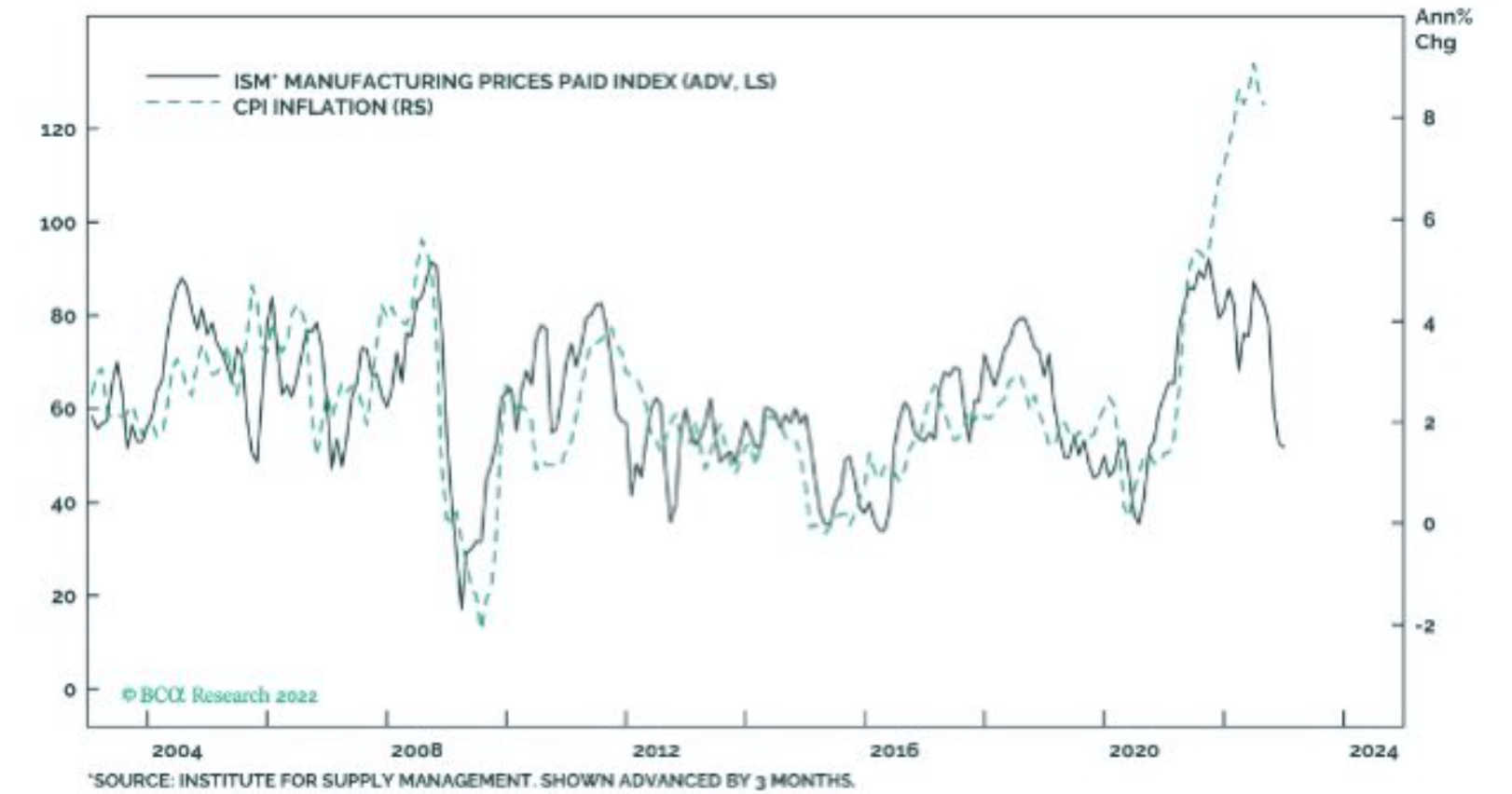

Monetary policy is a tool with a significant lag. The Fed is aware of this, and that is the reason they wanted to front-load their rate hikes as much as possible. The first tremors are now felt in the housing market, which is basically freezing over at current mortgage rates. We are of the opinion peak inflation is behind us and the Fed is going to go 75bps, 50bps and then 25bps before stopping:

ISM Prices Paid (ISM)

In our view, 10-year yields are going to end up somewhere around 4.5%, but with significant monthly volatility. We believe bond market volatility is here to stay, and that it was artificially suppressed for long periods of time.

2022 has been an unprecedented period in the market. This year has seen one of the most violent bear markets in bonds, with yields in many cases rising almost vertically. Just keep in mind that one year ago, 10-year yields were at 1.5%! Fed’s incompetence has resulted in the wild swings in yields and the almost vertical move up at times.

TYO is a 3x leveraged fund, not a buy-and-hold instrument. A retail investor who now understands the product needs to put strict targets in place and adhere to them. We are happy with 10-year yields being close to our target and happy with the 13% plus profit on the trade. We are therefore moving from Buy to Hold on TYO.

Performance

Since our article, the fund is up more than 13%:

Performance (Seeking Alpha)

We were fairly specific regarding our target return and yield level in our original article:

With 10-year yields down almost 40 bps on the week, driven by profit taking and talk about another “Fed pivot”, we feel the current 3.67% level is unsustainable. We are of the opinion that the Fed is crystal clear regarding its desire to front load rate hikes and use 2023 to go to neutral, and similarly to Goldman Sachs, we see 10-year yields above 4% by year end. That view translates into a 15% plus return for TYO for the remainder of the year.

Leveraged funds need tight targets in place. TYO is not a fund to be held for long periods of time, given its leveraged nature.

Conclusion

TYO is a 3x leveraged fund that increases in value as 10-year yields rise. The fund is an inverse ETF tracking the ICE U.S. Treasury 7-10 Year Bond Index. We wrote a piece regarding TYO at the beginning of October, when 10-year yields were artificially low in our opinion. TYO is a leveraged product, not a buy-and-hold instrument, thus strict targets need to be put in place by a retail investor. In our case, we were targeting 10-year yields close to 4.5%. With the significant rally in yields today, we are close to the target and feel TYO is now a Hold. We expect bond volatility to remain elevated going forward given the artificial suppression in the past, but feel the vertical move up in yields is now firmly behind us.

Be the first to comment