greenbutterfly

Summary

I recommend going long DigitalOcean (NYSE:DOCN). The growth in the number of SMBs worldwide and the shift towards multi-cloud deployments by businesses are underlying trends that will drive demand for DOCN’s services.

Company overview

DOCN helps software developers, startups, and small and medium-sized businesses (SMBs) by providing them with on-demand infrastructure and platform tools for application development, deployment, and scaling.

Plenty of underlying trends for DOCN to ride on

The use of technology in customer service, corporate administration, and the pursuit of a competitive edge is revolutionizing organizations of all kinds. Due to the worldwide phenomena of technology-powered growth and innovation, practically all businesses must focus on using technology through cloud services. Companies are increasingly adopting cloud computing as their preferred IT infrastructure due to its scalability, adaptability, and dependability. With cloud computing, companies can focus on customer-facing applications rather than on building out costly in-house IT systems. Particularly appealing to new ventures and SMBs is the fact that cloud computing enables them to access and use advanced features that would be prohibitively expensive or difficult to implement on-premises.

Considering that there are 32.5 million SMBs in the United States and around 400 million SMBs worldwide, I think DOCN has a huge market opportunity. Additionally, I believe this number will continue to rise in part because there are less constraints placed on would-be business owners. In addition, many SMB’s founding teams increasingly consist of a considerably more diverse set of people than only technical people. These people can launch firms with the help of readily available and inexpensive cloud computing and simple, dependable programming tools. Due to the advantages of cloud computing in terms of speed, cost, and ease of management, a growing number of new businesses and established SMBs are adopting this model.

Another significant shift I’ve seen is the widespread adoption of numerous cloud platforms by enterprises. Rather than relying on a single provider for their IT needs, businesses and individuals are increasingly turning to multi-cloud deployments in order to better tailor their applications to the most appropriate tech stacks and model for operating them, while avoiding the vendor lock-in that is typical of traditional IT infrastructure services. In my opinion, the growing popularity of using several cloud services will have a positive long-term impact on the worldwide cloud computing market.

DOCN solution is simple and cost transparent

The primary issue for SMBs is that the solutions provided by major vendors are designed for enterprise applications. These companies’ offerings usually aren’t made with SMB in mind. These products and services likely don’t provide what users need, are overly complicated, have no clear price or billing structure, and typically have substantial hidden fees. Therefore, many SMBs lack the resources necessary to fully gain from adopting these cloud computing capabilities from large vendors.

The DOCN platform was made to speed up the time it takes to go from inquiring to deploying a solution, all without the need for substantial preparation or training. What this means is that the fundamental barrier to adoption, the difficulty in deployment, is effectively removed. The platform is also made to accommodate developers for a wide variety of use cases, and it can be deployed in minutes. (Note: I encourage readers to go through DOCN product page for full understanding of Droplet technicalities).

SMBs rely heavily on cash flow, so unexpected costs can seriously affect their financial picture. Therefore, I think that open pricing is a major factor encouraging SMBs to adopt DOCN solutions. Due to DOCN’s transparent pricing structure (consumption-based and renewed on a monthly basis), optimizing deployments for customers is a breeze. DOCN enables users to monitor their monthly budget and avoid unpleasant surprises.

Customer acquisition model stems from community ecosystem

DOCN is responsible for establishing one of the most extensive online communities for developer education. The S-1 claims that there are about 3.5 million monthly unique visits due to the strength and growth of the DOCN community ecosystem. I see this as a major competitive advantage in terms of attracting new customers. As the network’s user base expands and more valuable material is produced, DOCN benefits from a greater number of paying subscribers and a more robust self-service infrastructure. The additional benefits of this are as follows:

- A platform where DOCN can gain insights on what are the upcoming products that developers demand

- A platform where developers can gain confidence with DOCN’s products and capabilities before testing out the product itself

In my opinion, DOCN has a sizable window of opportunity to significantly broaden its current customer base. An example of DOCN is the hiring of more inside salespeople, potentially even in other countries.

Acquisition of Cloudways

The acquisition is an excellent one in my opinion. The expansion of Cloudways’ market access for DOCN provides new opportunities for expansion.

Customers’ lack of self-assurance in their abilities to manage cloud infrastructure is cited as a leading cause of their departure from the DOCN platform during the first 90 days. Management thinks it can retain and boost ARPU with Cloudways’ SMB clients by offering more managed services to those customers. This makes sense to me as it is the lowest hanging fruit to extract synergies.

DOCN has been the foundation for the success of many ecommerce-specific managed hosting companies. DOCN’s move into the same final market could put it in direct competition with some of its current clientele. However, I don’t think this will be a major problem because the TAM is so big. Ultimately, I think this is a smart business move that will help DOCN grow faster.

3Q was good but also indicates near-term risks

The third quarter was DOCN’s best ever, with revenue up 3% and EBIT up 850 basis points from the previous year. DOCN provided quantitative details about the effects on its model, such as a 900bps headwind to 3Q due to poor macro, declining blockchain trends, and the impact from the Russia/Ukraine war. On the flipside, this was somewhat countered by a 12% price hike on July 1. On guidance, I believe 4Q targets for 35% revenue growth implies a further deceleration in underlying growth, given that Cloudway and a pricing step up are included.

Another thing to highlight is that DOCN is enacting to foster long-term growth despite macroeconomic constraints. Put simply:

- By controlling OPEX growth

- Improving mix shift through continued spending on features like better storage and security. Management believes storage revenue could double in mix

- Optimizing pricing strategy

I anticipate that these levers will result in long-term structural improvements. Having said that, I believe there are some near-term risks because demand in key end markets is expected to remain weak until 2023.

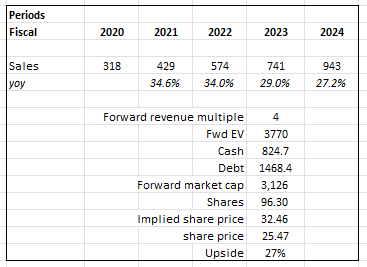

Valuation

I think investors can expect a 27% return based on my model.

My model assumption is based on my belief that, given the size of the TAM, DOCN stock will continue to grow at a rapid pace. Having said that, I anticipate a slowing of growth from 30%+ to the high 20%’s in 2023. This is to reflect end-market pressure.

Over time, as DOCN grows and expands its margins (Gross margin and EBITDA margin), I believe the valuation will return to historical levels (not at 4x, which is near an all-time low). However, given the near-term headwinds, I believe valuation will remain unchanged.

Own calculations

Risks

Increased competition

Given the scale and growth of the public cloud market for SMBs, it seems only logical for larger public cloud companies to compete in this market. DigitalOcean’s competitive position could weaken if this happens.

Execution

Direct sales growth, brand awareness expansion, upselling existing customers, and improved customer retention are all ways in which DOCN might speed up its revenue development. If these sales, marketing, and customer success playbooks aren’t implemented properly, future growth may be jeopardized.

Conclusion

DOCN is a cloud computing company that helps software developers, startups, and SMBs access on-demand infrastructure and platform tools for application development, deployment, and scaling. The trend towards businesses adopting cloud computing, particularly SMBs, is a major opportunity for DOCN. Additionally, the growing popularity of multi-cloud deployments means that businesses are increasingly turning to multiple cloud platforms, rather than just one provider. DOCN’s platform is designed to be simple and cost-effective, with a transparent pricing structure and optimized for ease of deployment. Overall, DOCN appears to have a strong market opportunity and attractive offerings for its target users.

Be the first to comment