BlackJack3D/iStock via Getty Images

Investment Thesis

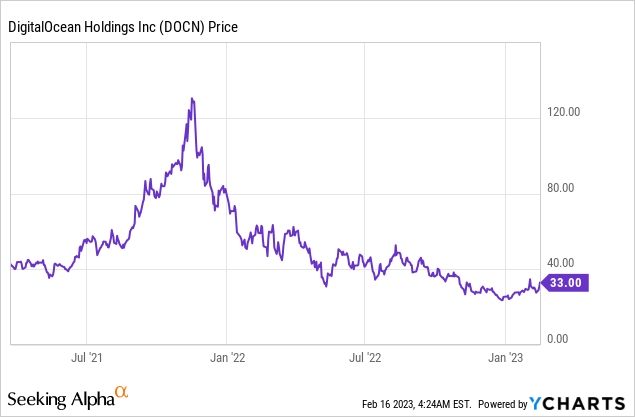

DigitalOcean (NYSE:DOCN) went public back in early 2021. The company saw strong traction initially with shares up over 200% in just a few months. But as the market starts to pullback later that year, it also plummeted. It is now trading nearly 80% below its all-time high.

The company has a massive addressable market and is benefiting from the strong tailwind of digital transformation. The latest earnings results continue to demonstrate solid top-line growth with the bottom line being profitable as well. After the massive drop in share price, the company’s valuation seems attractive. Its multiples are way below cloud peers with similar growth rates. I believe a lot of negativity is already priced in the current price levels should offer decent upside potential. Therefore I rate the company as a buy.

Market Opportunity

DigitalOcean is a US-based technology company founded in 2011. It provides cloud infrastructure solutions to mostly SMBs (small and medium businesses) and startups. The company competes with the likes of Azure (MSFT) and AWS (AMZN) but it is able to win in the space as it offers much lower pricing and is less complicated to use compared to the hyperscalers. For context, DigitalOcean’s pricing can be over 40% cheaper compared to AWS. It is also much easier to set up and manage which is a huge appeal to beginners. The company currently has over 600,000 customers with 15 data centers globally.

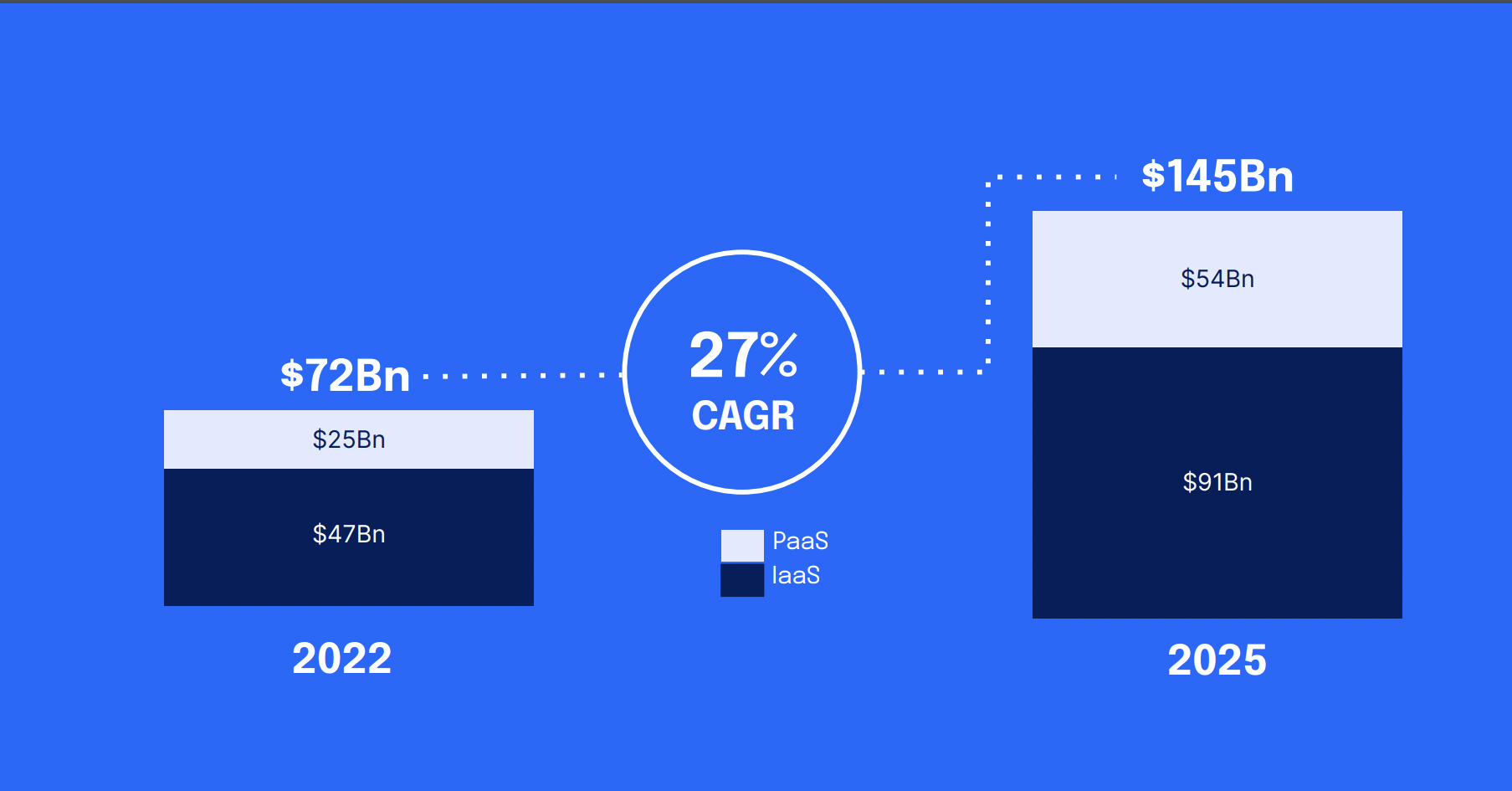

The market opportunity of cloud is massive. According to Grand View Research, the global TAM (total addressable market) is forecasted to grow from $484 billion in 2022 to $1.55 billion in 2030, representing a strong CAGR (compounded annual growth rate) of 15.7%. The company themselves estimates its TAM to grow from $72 billion to $145 billion in 2025, representing an even higher CAGR of 27%.

The shift to cloud is only in its early innings and there are multiple catalysts driving the expansion. For example, streaming services have been growing quickly with the launch of Disney+ (DIS) and HBO Max (WBD) which vastly increased the demand for cloud infrastructures. With the ongoing adoption of IoT (internet of things), the number of connected devices such as connected vehicles is also growing rapidly. Not to mention the latest trending AI (artificial intelligence) technologies such as ChatGPT which require substantially more computing power. The overall acceleration of digital transformation should continue to be a strong tailwind.

DigitalOcean

Q4 Earnings

DigitalOcean just announced its fourth-quarter earnings and it recorded yet another double beat. Top-line growth continues to be strong while the bottom line also improved. The company reported revenue of $163 million, up 36% YoY (year over year) compared to $119.7 million. ARR for the quarter was $659 million compared to $490 million, up 34% YoY. The growth is driven by the increase in customers paying $50/month, which grew 45% from 99,000 to 144,000. The net dollar retention rate was 112%, down slightly from 116%. Due to inflationary pressure, costs of revenue was up 42.8% YoY from $44.4 million to $63.4 million. This resulted in the gross profit margin dropping 200 basis points from 63% to 61%. Gross profit was up 32.3% YoY from $75.3 million to $99.6 million.

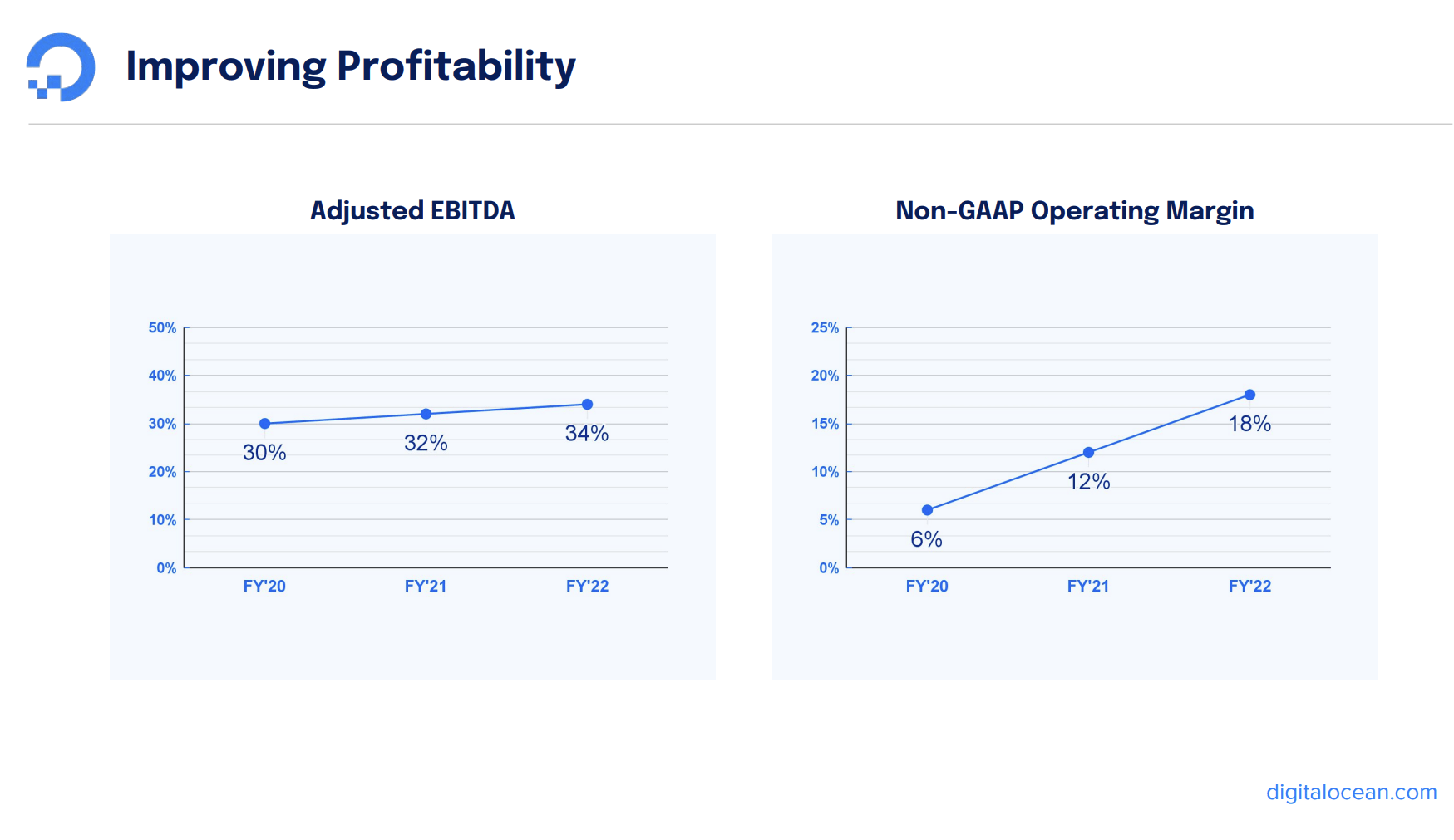

The bottom line also improve as it continued to show operating leverage. Adjusted EBITDA was $51 million compared to $37.8 million, up 34.9% YoY. Adjusted EBITDA margin of 31.3% was essentially flat YoY compared to 31.6%. Non-GAAP operating income increased 78.9% from $14.7 million to $26.3 million. Non-GAAP operating margin also increased from 12.3% to 15.9%. It posted a free cash flow of $35.7 million compared to just $173,000. The free cash flow was 22%. Non-GAAP diluted net income per share was $0.28 compared to $0.11, up 155% YoY.

DigitalOcean

The company also initiated guidance for FY23. Revenue growth was slightly below consensus which is kind of expected due to macro weakness, but guidance for the bottom line came in much stronger than most have expected. It guided revenue to be $700 to $720 million which represents revenue growth of 23% at the midpoint. Non-GAAP diluted net income per share of $1.65 to $1.69 translates to a whopping growth of 77.7% at the midpoint. Adjusted EBITDA margin of 38% to 39% and FCF margin of 21% to 22% is also a further step up from the current year.

Investors Takeaway

I believe the current price presents a good buying opportunity for DigitalOcean. The company has a huge and expanding TAM which should continue to fuel growth moving forward. Its low pricing and easy-to-use strategy differentiate them from hyperscalers and attract SMB customers. The latest quarter is very strong as revenue growth remains robust despite facing a tough macro backdrop. Bottom line continues to improve with income and cash flow up significantly. Guidance for revenue growth was soft but I don’t mind it at all as bottom-line metrics look really solid. After the huge drop, the company is now trading at a PS ratio of 6.98x which is pretty cheap given the substantial growth. Cloud peers with similar growth rates such as Datadog (DDOG) and CrowdStrike (CRWD) are trading at a PS ratio of 18.3x and 13.5x respectively, which represent a significant premium. Considering the current growth, profitability, and valuation, the company should be trading at levels closer to peers in my opinion. This implies meaningful upside potential therefore I rate the company as a buy.

Be the first to comment