Vladimir_Timofeev

Digital Realty Trust (NYSE:DLR) is a large data center real estate investment trust. Data center REITs like DLR have been successful investments for several years, including getting a boost from Covid-19 related accelerated digitization. Many REITs, including DLR, have not performed well in 2022, and it appears likely that DLR will remain range-bound for the near term.

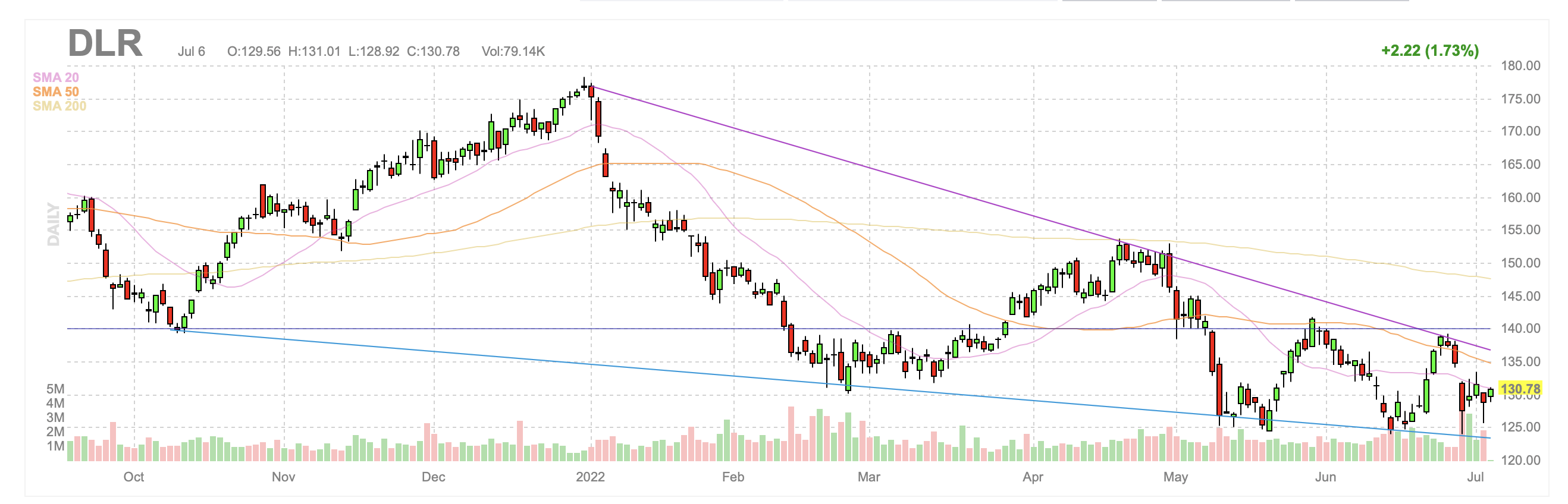

DLR daily candlestick (Finviz.com)

Data centers are necessary for storing and processing digital information and transactions. Growing demand for data center capacity has driven several years of increased supply. Digital Realty, among others, has grown its data center portfolio through both constructing and acquiring capacity. Much like the broader industry, a fair amount of the growth has been international.

Digital Realty has also grown its domestic capacity, including within New York and Virginia, among the over two dozen global metropolitan areas in which it is currently developing additional projects. It is probable that some pricing pressure would develop in a market that gets saturated with supply, which could occur here.

Reasons for concern would include reduced value of international business converted back into stronger dollars, as well as possible margin pressure due to market capacity. The strength of the dollar will end up being a substantial headwind to full-year revenue and core funds from operations.

A hike in the interest rate is also a major concern for Digital Realty. Increased rates make it more expensive to develop real estate. Also, REITs often act as alternatives and/or supplements to fixed income, because they must distribute most of their income as dividends in order to avoid taxation, and that dividend becomes less compelling when compared to a higher free rate of return.

In the first quarter of 2022, DLR increased its quarterly cash payout to $1.22 per share. This was a 5.2% increase from the prior dividend of $1.16. DLR’s ability to continue to further increase its dividend could be lessened by existing higher rates and weak foreign currencies. Increased energy and construction costs could exacerbate the situation.

Another concern, recently highlighted by short-selling investor Jim Chanos is that many of the largest tech companies are or will directly compete with data centers by developing their own capacity. This takes large customers out of the demand pool, and it makes them ruthless competitors that may be willing to accept much lower margins.

Such risks have always existed for Digital Realty and the data centers, so this is not an unknown risk, but also a very real one. With current supply chain constraints, it is unlikely many new competitors would enter the market here and now, so several may reduce plans. DLR’s focus obligates them to push forward through spiking costs and supply chain bottlenecks. Mega-cap competitors could easily eat such costs, and their existing development may be contributing to various capacity constraints.

I believe the greater risk to DLR, and most REITs, remains interest rates. High-yielding equities are vulnerable to spiking interest rates. Also, REITs pay a non-qualified dividend, which makes their distributions taxable at the same rate as a fixed income product, as compared to a qualified corporate dividend. In either case, a higher risk-free rate of return reduces the value of higher risk dividends. Similarly, increases to borrowing costs will make it more difficult to finance the paying of dividends and make it more costly to finance the development of capacity.

Higher rates also reduce the ability to finance acquisitions. DLR should find it more costly to finance M&A activity, as well as perform planned construction. It may be the case that the multiple at which data centers were previously being valued was too high, and often included a buy-out premium. This premium may now be leaving the industry. It will probably take a few quarters for the major data centers to prove their plans, and also to confirm where interest rates move in the market.

Conclusion

Digital Realty Trust has a strong data center business that is growing, but it appears that data center valuations may have peaked in early 2022. If that is the case, DLR should remain rangebound for the near term.

DLR shares appear to be in a reasonably defined range of resistance at about $140 and support at around $120. I prefer to wait to see DLR contend with either.

Be the first to comment