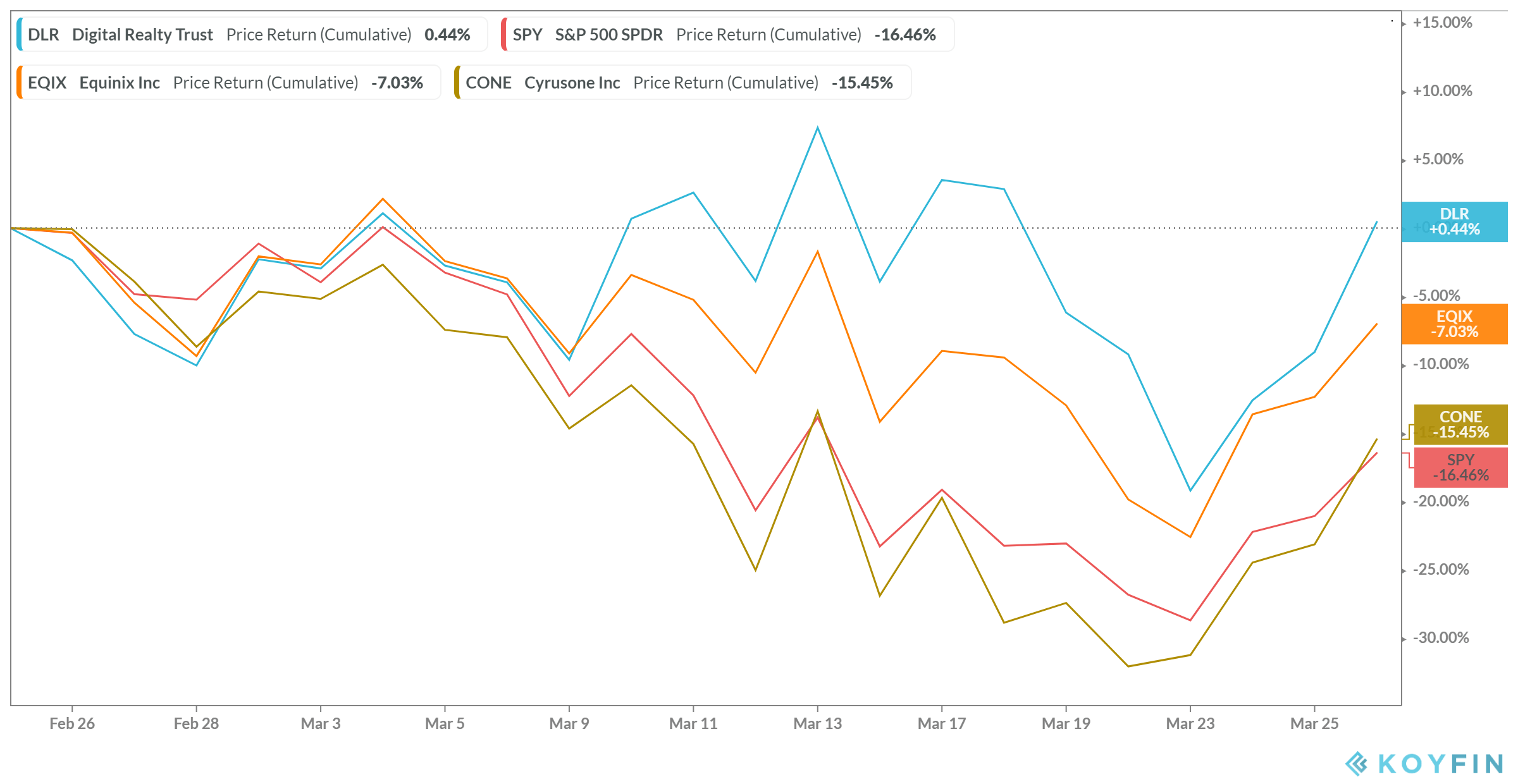

Few stocks have evaded the historical selloff of the past month. Even the real estate sector took a massive beating, despite being considered one of the safest in terms of cash flow stability, as I highlighted in my latest article.

Real estate has massively transformed over the past decade. Investors would find significant growth in malls and residential REITs. However, nowadays, the appeal has remarkably shifted towards data centers, cell towers, and even storage REITs. I am a bigger fan of data centers, because of the massive growth of the cloud and the Infrastructure-as-a-Service (IaaS) market, which has been evolving at a rapid pace, with no end in sight. One such stock is Digital Realty (DLR), which, in my view, is one of the best dividend growth stocks in the market right now.

I base this statement on Digital Realty’s:

- Minimal cash flow disturbance risk caused by Covid-19

- Excellent turnover and dividend growth record

- Limitless growth potential, executed by an experienced management team with shareholder-aligned interests.

Covid-19

Digital Realty is one of the few stocks that have seen little to no suffering over the past month, compared to the overall market. The reason is because of its security in terms of its cash flow. While the market has been swiftly selling equities in an attempt to price in the coronavirus impact on companies’ income statement, Digital Realty has proudly stood still.

On the retail side of REITs, we have seen tenants like The Cheesecake Factory (NASDAQ:CAKE), failing to meet their rent obligations, and asking for the landlords’ understanding and help. In this case, landlords will have to take the hit, and compromise, as this affects every brick-and-mortar business (ex. groceries, pharmacies, etc). To kick restaurants and retailers out would be pointless and would benefit no one, both in the short and in the long run.

However, when it comes to Digital Realty and data centers in general, there are two significant differences.

- Unlike, say The Cheesecake Factory whose customer traffic has plunged amid closings, digital traffic has seen growth. Both Facebook (FB) and Netflix (NFLX) have recently reduced their video streaming quality amid unexpected traffic. With people self-isolating, physical traffic has turned into digital.

- In comparison to other businesses, data centers cannot simply shut down. Unlike, say a restaurant, firms that rent Digital Realty’s centers cannot suspend their usage of data centers, especially now, since online traffic is hitting all-time highs. If anything, the demand for the company’s centers should be going up.

Robust Financials

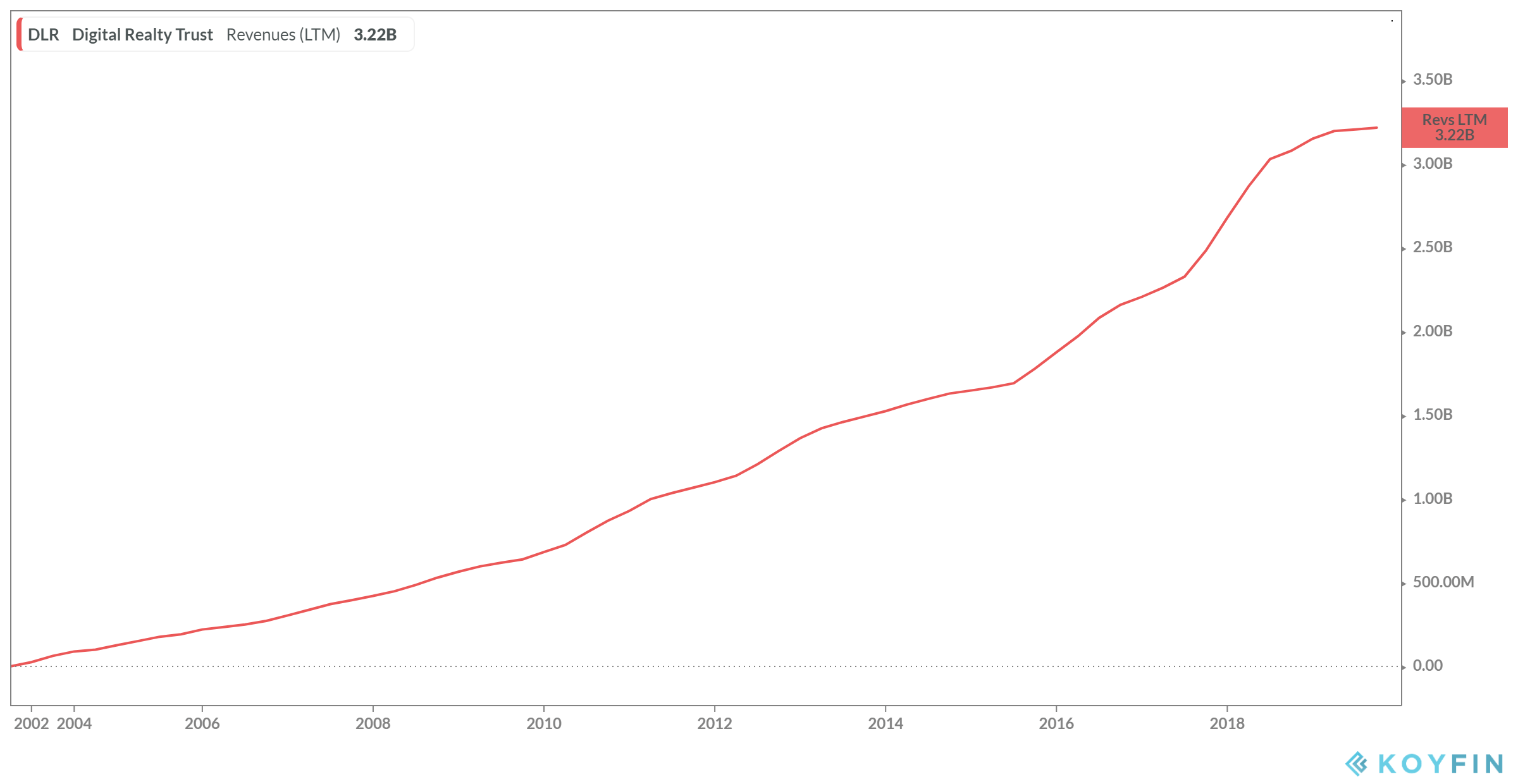

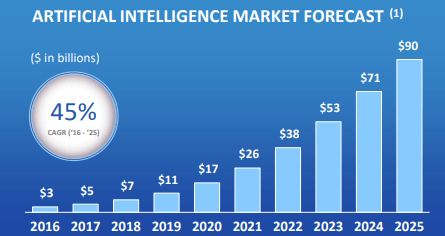

The company’s excellent past record of growth has been a result of the increasing demand for firms to house their servers and network equipment. Revenues have been on a continuous climb on a yearly basis. To bolster my earlier point, revenues were soaring on the Great Recession, as you can see in the graph. Growth was hovering between the range of 30% and 40%. Plugging off servers is not that easy.  Management is very bullish on the rise of data center demand, especially when it comes to artificial intelligence, internet-of-things, autonomous vehicles, and virtual/augmented reality. Artificial intelligence, for example, is expected to grow by a CAGR of 45% (2016-2025). Artificial Intelligence is the more predictable of the four ones and therefore displayed, just to be prudent.

Management is very bullish on the rise of data center demand, especially when it comes to artificial intelligence, internet-of-things, autonomous vehicles, and virtual/augmented reality. Artificial intelligence, for example, is expected to grow by a CAGR of 45% (2016-2025). Artificial Intelligence is the more predictable of the four ones and therefore displayed, just to be prudent.

Source: Corporate presentation

Outstanding FFO/dividend growth

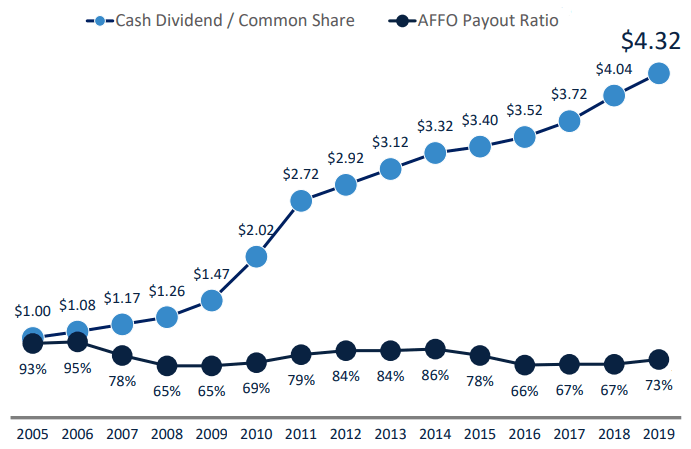

Digital Realty’s dividend growth is phenomenal, as the article’s title suggests. Being a REIT, said growth is driven by the underlying advance of FFO (Funds From Operations), which has been growing at 12% CAGR since the Trust’s IPO in 2005. Moreover, dividends per share have been growing at a CAGR of 11% for that same period. Not only is this an incredible dividend growth rate over 15 years, but since it’s slightly lower than the AFFO’s CAGR, the company’s payout ratio has been maintained at an optimal level, never having reached worrying levels.

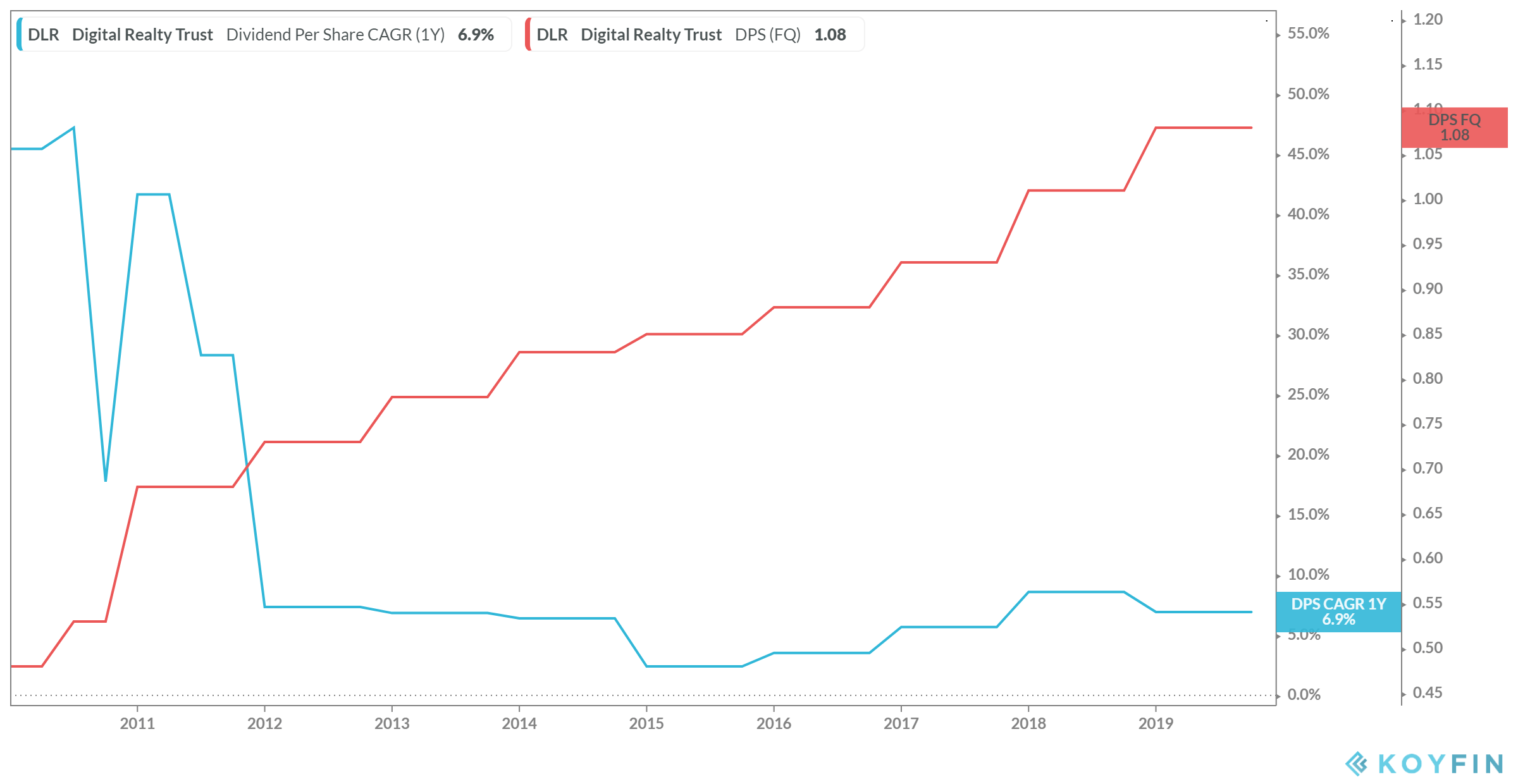

Even over the past few years, for which dividend growth has come down to more reasonable levels, it remains solid. At its lowest point, in 2015, the 2.4% rise was enough to cover for inflation, while the last two increases (6.9% for FY2019 and the current 4% for FY2020) are more than appealing, if I may say.

{kind=link}

With 14 years of consecutive dividend increases and a healthy payout ratio, I believe that it is fair to say that the company is more than likely to become a dividend aristocrat as well. The stock currently yields ~3.4%.

Risks

REITs are constantly raising money through debt and equity to fund further acquisitions since they tend to distribute the majority of their profits in the form of dividends. However, both of these could end up being potential long-term risks, as they sit on the liabilities side of the balance sheet.

Debt

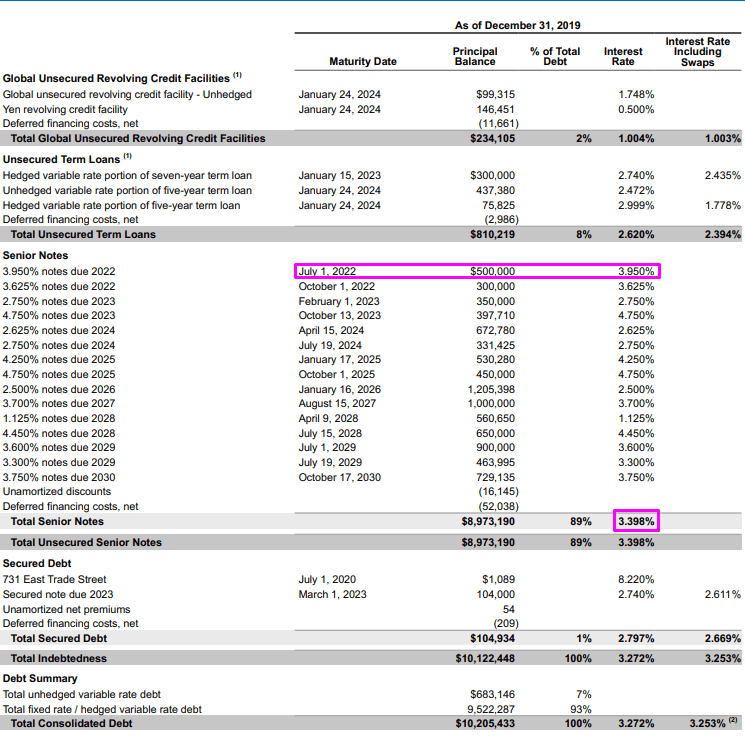

Digital Realty’s long-term debt position has been significantly growing over the years, currently sitting at a whopping $10.12B. That is certainly not petty, considering the company’s enterprise value of $38B. However, considerable amounts of debt are not necessarily troubling. Assuming sound execution and low rates, debt can be very beneficial.

More specifically, the next maturity on the company’s way is more than two years away, on July 1, 2022. Not only is this a relaxed time frame towards the payment, but the company is most likely to refinance the debt, considering the current low-rate environment. Speaking of low rates, the average interest charged for Digital Realty’s total unsecured notes (which make for 89% of total debt) is ~3.4%, which is common for the sector and favor debt issuance in comparison to equity.

Source: Supplementary information

Equity

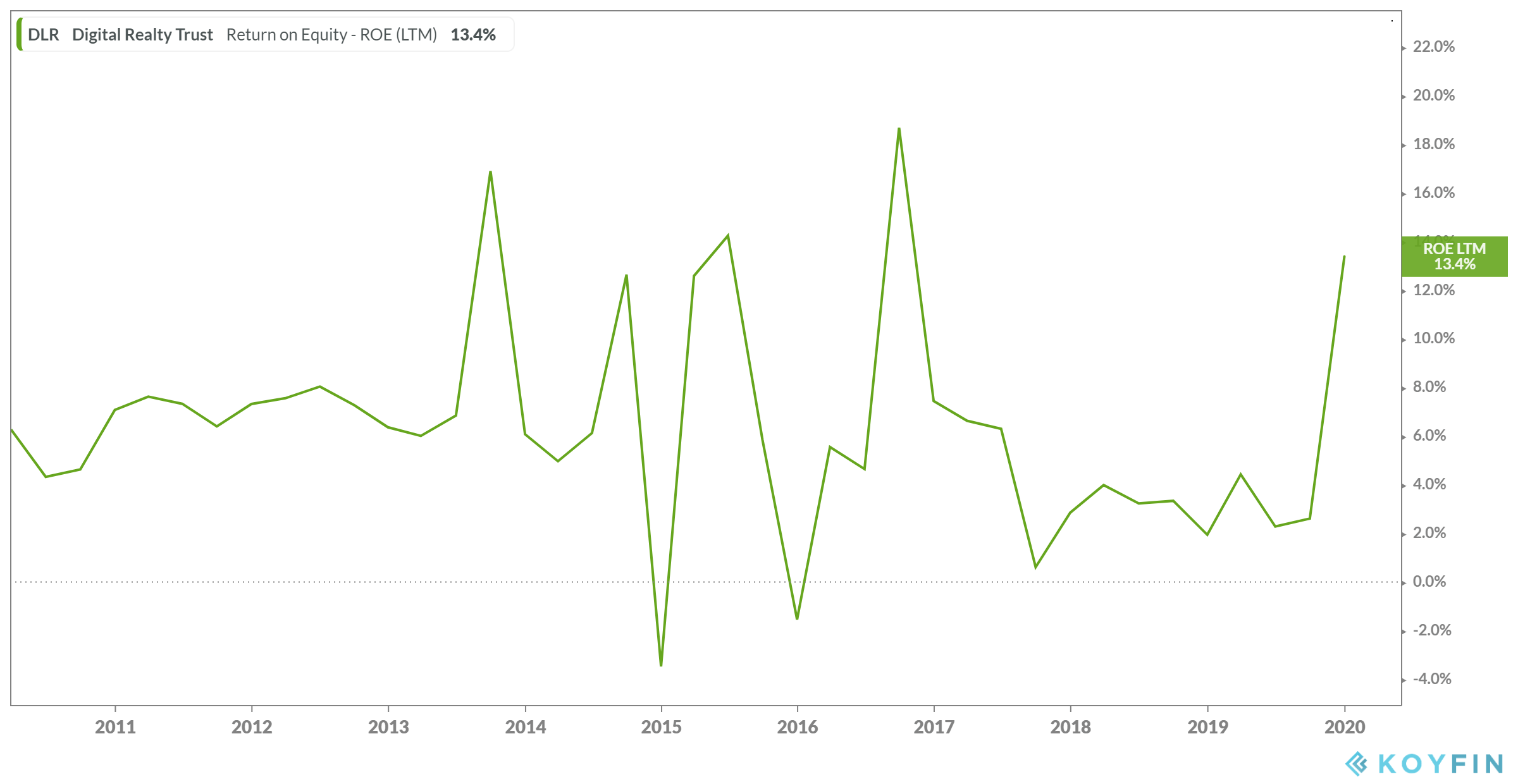

As I mentioned, raising debt instead of equity makes sense, since the company can return much higher on the current low rates charged. Consider its ROE (Return on Equity). Shareholders’ equity is equal to a company’s assets minus its debt. Therefore, ROE is considered the return on net assets. ROE highlights how effectively management is using Digital Realty’s assets to generate profits. As you can see, for example, the company’s ROE for LMT (Last Twelve Months) is 13.4%, while the overall ratio hovers anywhere from 4% to 18%. With such value created, the company’s debt is being used wisely.

Additionally, it would make sense for the company to avoid issuing lots of equity since it is clearly more expensive to do so. Not only is it diluting existing shareholders, but it also has to increase its total dividends paid to match the distributions on the existing shares.

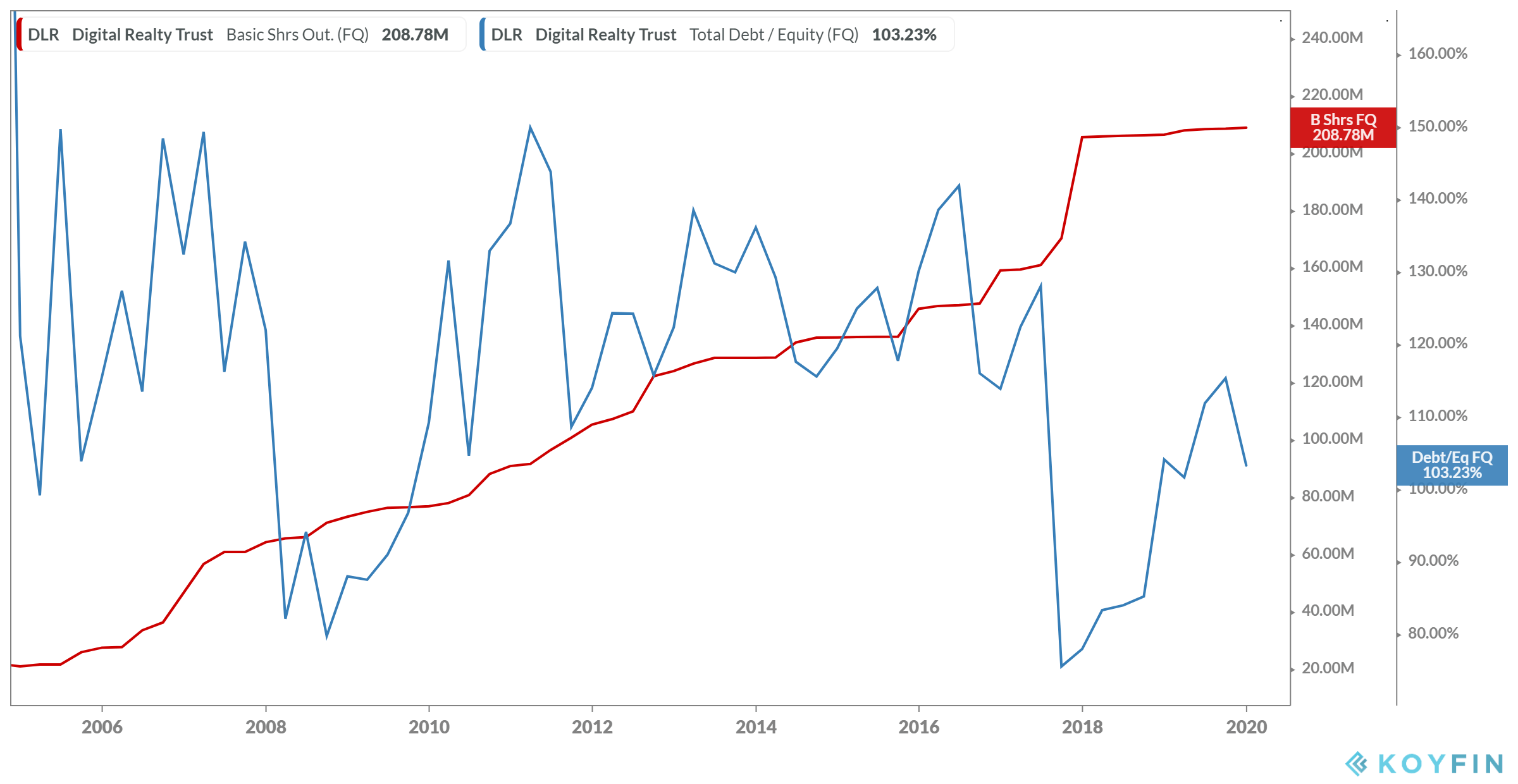

However, share issuance cannot be avoided as well, since the debt/equity ratio must be maintained to an acceptable level. As you can see, total shares outstanding are now ten times higher since the company’s IPO. The curve has recently flattened with minimal issuance of shares, as the firm brings its debt/equity ratio to a more reasonable 13.23%, though still being quite leveraged. Overall, management has excellently brought in funds both from shares and debt to create superior value, considering the costs. Since the stock’s dividend is currently close to the average debt rate, investors should expect a mix of both for future fundraisers.

Overall, management has excellently brought in funds both from shares and debt to create superior value, considering the costs. Since the stock’s dividend is currently close to the average debt rate, investors should expect a mix of both for future fundraisers.

Conclusion

Digital Realty has evolved into a data center behemoth, heavily rewarding its shareholders in terms of both capital gains and dividend growth. Moreover, the company has established shareholder-friendly policies to align management’s interests as well. The company has implemented minimum stock ownership requirements for its directors and senior executive officers.

More specifically, the policy requires ownership of the company’s common stock in amounts of six times the base salary for the Chief Executive Officer; three times the base salary for the CEO’s direct reports; and one and a half times the base salary for certain other executive officers. A similar policy applies to the rest of the directors as well.

Considering the company’s excellent track record, shareholder-friendly policies, and limitless potential on the digital real estate side of the REIT sector, I believe that the stock is a superior long-term hold. That goes especially towards dividend growth investors, who seek an attractive income play, at an ultra-low rate environment.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment