Gearstd/iStock via Getty Images

The COVID pandemic and the government’s reaction to it created a number of unsustainable surges in revenues and profits for many industries. The government poured in almost $4 trillion in stimulus into the economy in 4 packages concentrated in less than a year. This was way more than ever done before and way more than what was lost to the pandemic. Consumers and businesses were left with massive amounts of unexpected cash and they went on a spending spree. The surge in demand created the most inflationary environment in 40 years and broke down many supply chains. It also took existing bubbles in hyper growth stocks and expanded them even further. New bubbles in IPOs, SPACs and meme stocks were also created.

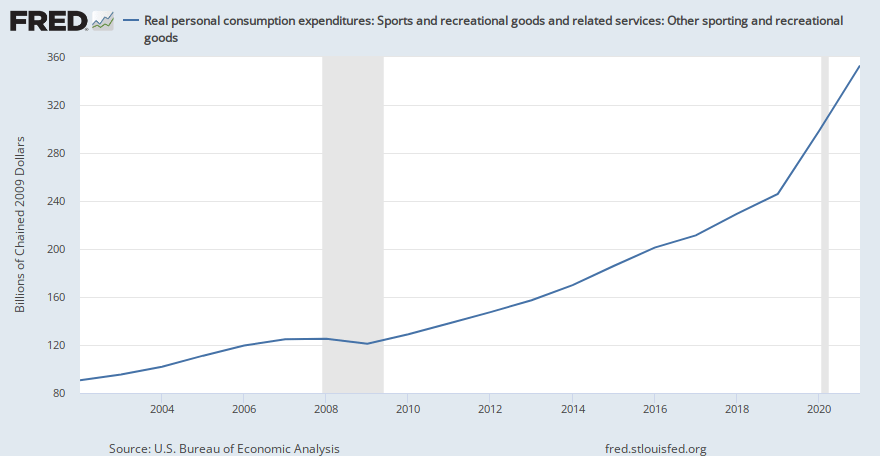

The sports equipment retail industry benefitted more than most industries. In addition to the massive stimulus, new demand was created by people cooped up at home. The BEA chart below shows an acceleration in sporting goods purchases starting in 2020.

U.S. Bureau of Economic Statistics

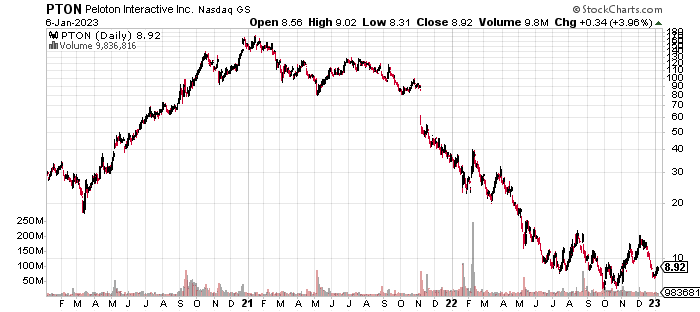

A prime example of this phenomenon was Peloton (PTON), an exercise equipment manufacturer and retailer. As shown below the stock surged during the pandemic over 300% to a peak in December 2020, and has since dropped 94%.

StockCharts.com

Peloton is an extreme example but the whole sporting goods industry has enjoyed a surge in both revenues and profit margins. What happened to Peloton is likely to happen to the industry to a lesser degree.

DICK’S Background

DICK’S Sporting Goods, Inc. (NYSE:DKS) is based in Coraopolis, Pennsylvania and is the largest pure play sporting goods retailer in the U.S. As of October 29, 2022, DICK’S operated 732 DICK’S stores and 136 other stores under the names Golf Galaxy, Field & Stream, Public Lands, and Going, Going, Gone! The 868 total stores increased by 2 from one year earlier.

The fiscal year ends each January. In fiscal 2021 (ended 1/2022), 44% of sales were hardlines such as sporting goods equipment, fitness equipment, golf equipment and hunting and fishing gear. Another 34% was apparel and 21% footwear. Online sales represented 21% of sales in fiscal 2021, up from 16% in 2019. Seventy percent of online sales were fulfilled in stores in fiscal 2021.

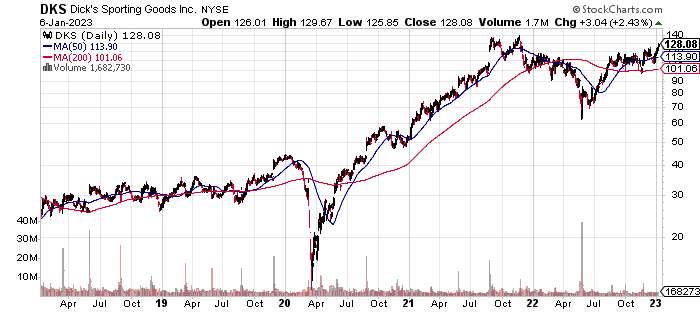

The stock price of DICK’S as shown below increased over 3X since the pandemic started in early 2020 and 4X since 2019 as shown below.

StockCharts.com

The company pays a modest dividend with a current yield of 1.56%.

Financials

Operating results surged during the pandemic. Net sales increased 40.5% in FYE 1/22 compared to FYE 1/20, the last full year before the pandemic. Gross margins increased 910 basis points during that period. P re-tax income grew from 4.7% of revenues in FYE 1/20 to 16.2% in FYE 1/22. The chart below shows operating results over the past 6 years.

SEC filings

As shown above, DICK’S for years had a net income margin of 3-4%. This actually stretches back to 2016. Prior to that it was in the 4-6% range going back to 2010. The surge in sales was across the board in all 3 primary categories; hardlines, apparel and footwear. This current fiscal year, the profit margin has been 9.2%, double to triple historical numbers. That is down from 12.4% in FYE 1/22 despite management noting no falloff in consumer behavior due to economic weakness, even at the low end.

Earnings were strong in the most recent quarter at $2.60, beating estimates of $2.21. However, weakness was noted in apparel. CEO Lauren Hobart said

“Apparel was an issue this past quarter, and we will be aggressive to clean up whatever needs to be cleaned up in Q4.”

The balance sheet is strong. As of October 29, 2022, tangible net worth was $2.0 billion. While there was $1.6 billion of interest bearing debt, this was mostly offset by $1.4 billion in cash on that date. Liquidity was also strong with $2.2 billion of working capital on October 29, 2022.

Headwinds

There are a number of headwinds that are gathering for DICK’S making it unlikely it can maintain its profit or gross margin anywhere near the levels of the past two years.

1. Margins Unsustainable

As noted above, the profit margin has historically been 3-4% from 2016 to 2019, and 4-6% previously. It popped up to 12.4% in FYE 1/2022 before falling back some to 9.2% in the first nine months of fiscal 2022. DICK’S peers, which are shown later in this report, had a similar surge. This indicates the surge in revenues and profit margins was mostly an industry related phenomenon, not something they did to improve the business. This surge was due to two major factors occurring at the same time, a pandemic and massive fiscal and monetary stimulus. The pandemic created more demand for outdoor sports and exercise activities.

People are returning to normal lives and the fiscal stimulus has ended. The monetary stimulus has reversed as the Federal Reserve has rapidly increased interest rates. While management is optimistic, it does not expect margins to stay anywhere near current levels based on this comment by CEO Hobart from its most recent conference call.

“we still believe that we will be able to retain a significant amount of our merch margin gains.”

CFO Navdeep addressed this later in the call this way:

“we are still guiding that we will maintain a meaningful portion of that margin gain”

I read this to mean management expects a large drop in their margins. This is without any assumption of a recession as they were talking about long term.

On January 9, 2023, athletic apparel company Lululemon preannounced that 4Q gross margins were expected

“to decline 90 to110 basis points compared to its previous expectation.”

This is a very recent shift downward for the leading player in the space.

2. Demand Pulled Forward

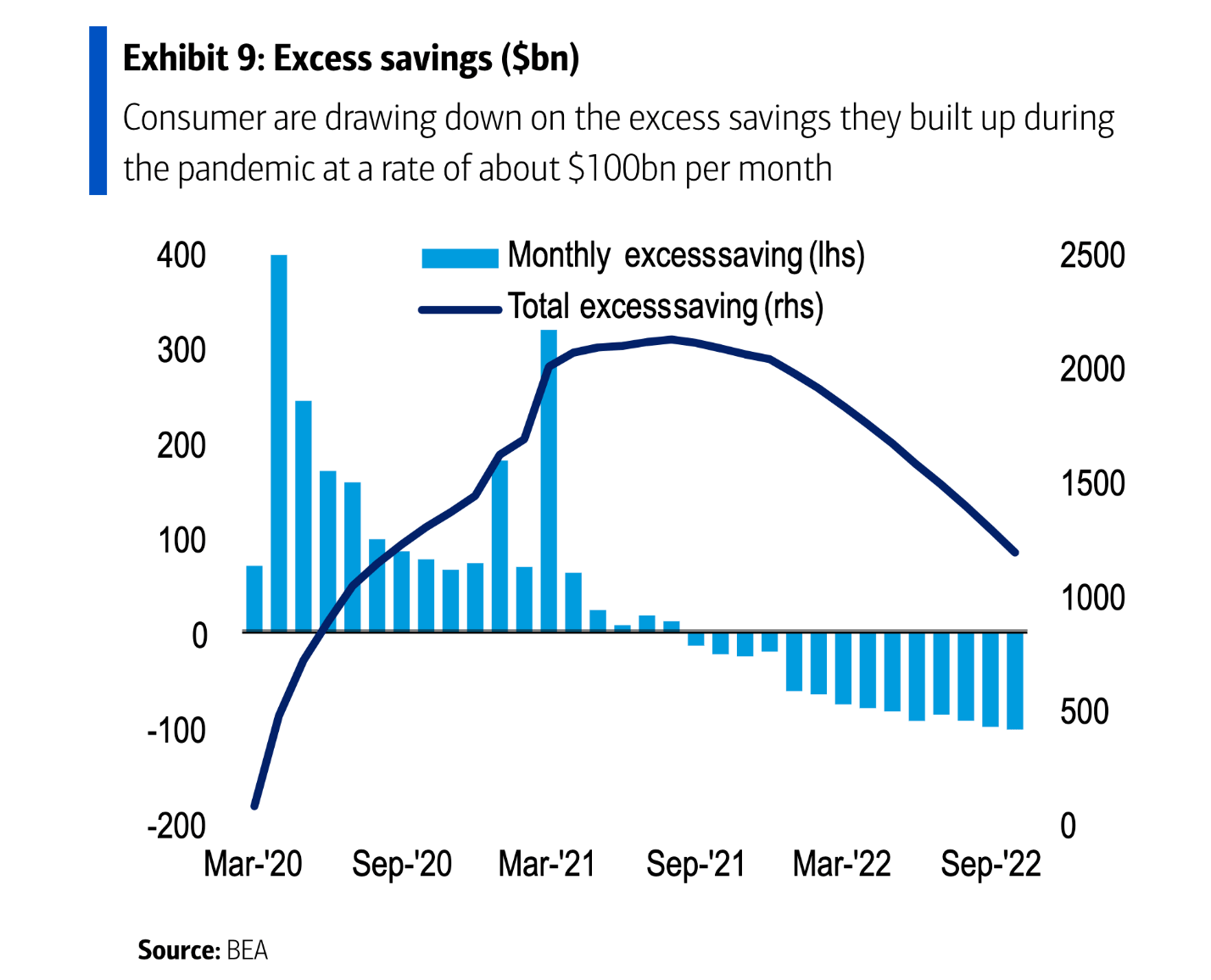

Pent up demand is one of the most powerful economic factors. It has gotten us out of every recession, though in a couple cases (1937 and 1982) it wasn’t strong enough to prevent a double dip. The reverse of pent up demand is pulled forward demand. That is what we have now. The massive $4 trillion of fiscal stimulus dwarfs anything ever done. As the chart below shows, at one point, consumers had well over $2 trillion in excess savings. That is now rapidly being drawn down. This will exacerbate the reversion to the mean for margins and possibly cause it to swing past prior historical norms.

U.S. Bureau of Economic Statistics

Another aspect to this is how many new basketballs, running shoes, and tee shirts do people actually need? There should be quite a lull in consumer spending on sporting goods after all the purchases in 2021 and 2022.

3. Inventory Is High

As of October 29, 2022, inventory was $3.36 billion, up from $2.49 billion one year earlier. This is a 34.9% increase. Sales increased 7.7% in the quarter ended October 29, 2022, but are down year to date. Management claims part of this increase was catch up from supply chain issues faced earlier. But analysts expect sales to drop 0.8% this fiscal year and be relatively flat in the next one. In my opinion, the analysts are too optimistic. Based on the prior two negative factors I mentioned, I expect revenues to drop significantly in the next fiscal year. DICK’S has done a good job of maintaining its sales surge levels in recent quarters, which I believe has fooled the analysts. The inventory level may be OK if the company can maintain the current level of sales, but I find that unlikely based on the headwinds mentioned in this article. If sales start to drop there will be a lot of markdowns needed which will further reduce margins.

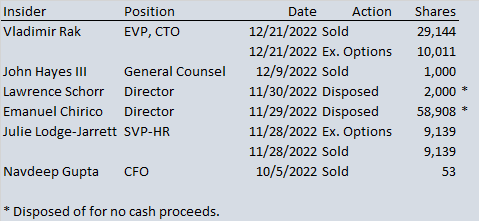

4. Insider Sales

The insiders are showing little confidence that current profits can be maintained as shown by a slew of recent stock sales by them. The chart below shows insider activity over just the past 3 months. The only acquisitions were option exercises all of which were promptly entirely sold.

SEC Filings

5. Competition

Quite often when profit margins improve it is because of less competition. This industry remains competitive and has in fact changed little since 2019. In addition to the pure player peers shown later in this report, DICK’S competes with Amazon (AMZN), Walmart (WMT), Target (TGT), Foot Locker, Cabela’s, Bass Pro and many others. What is important here is that DICK’S does not appear to have a secret sauce or moat to protect it from this competition, many of which are much larger.

6. Recession Likely

Many economists, and perhaps a majority, now expect a recession to start in 2023. This is highly unusual as I have never seen a recession actually predicted by economists. This may be the first. I was early as I wrote 3 articles in May and June 2022, explaining why I expect a recession. The last can be found here. In those I listed 17 headwinds shown below:

- Inflation

- Interest rates

- War in Ukraine

- Demand pulled forward by massive stimulus

- Stimulus fading

- Consumer sentiment is near historic lows by some measures

- IPO and secondary filings have fallen off a cliff

- Corporate warnings about growth

- Housing starting to decline after massive growth

- Strength of the dollar

- Bubbles bursting (primary cause of the 2000 and 2007-2009 recessions)

- Chinese declining housing prices and Covid lockdowns

- Inventory overstocked

- The un-wealth effect of declining stock, bond, and housing prices

- Refinance cash out spigot shut off

- Consumer credit balances increasing again

- Executives expect a recession

All of these are still relevant and many are becoming bigger issues. Many are specific threats to DICK’S including; interest rates, demand pulled forward, stimulus fading, consumer sentiment, housing declines, inventory overstocked, the un-wealth effect, and consumer credit balances increasing.

By the way, don’t expect a recurrence of the massive stimulus we just had if a recession occurs in 2023. The Republicans have retaken the House of Representatives. In my opinion, they are likely to stop any excessive spending since the last time it led to a huge rise in inflation. That was the main issue holding Representative Kevin McCarthy back from the Speakership he has now secured.

7. Discretionary Merchandise

Another factor specific to DICK’S is its revenues are mostly discretionary items. Discretionary items are usually the first that consumers stop spending on in a time of economic weakness. If money gets tight, what are you going to let go first; the mortgage, food, utilities or sports equipment?

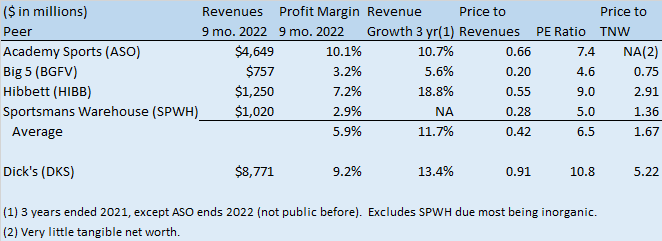

8. Valued Well Above Peers

DICK’S is the largest pure play sporting goods retailer but has several publicly traded peers. The chart below shows how they stack up.

EC filings, Value Line and Yahoo Finance

DICK’S has a much higher P/E ratio, price to revenues and price to tangible net worth than all of its peers. The only one somewhat close is Hibbett (HIBB) which has been growing faster. DICK’S due to its size, growth and profitability does deserve a premium, but not to this degree. What appears to be happening is a flight to the bluest chip. But all are equally exposed to unsustainable margins, pulled forward demand, and discretionary merchandise.

9. Little Growth

The high P/E ratio to peak sales and peers may be justified if DICK’S was growing its store base but that’s not the case. Total stores were 868 on October 29, 2022, up only by 2 from one year earlier. It is getting online growth, but that is still only 20% of the total so not moving the needle much yet. Also, DICK’S relies on its store base for online sales as 70% of sales are fulfilled in the stores. Revenues for the first 9 months of fiscal 2022 declined 2.1%. However, that decline is closer to 8-10% after inflation.

Positives

DICK’S does have a number of strengths and these are listed below.

1. As mentioned earlier, the balance sheet is strong and liquid even with the increased inventory.

2. DICK’S is the largest pure play player in the industry.

3. Apparel and footwear are a little more difficult for online disruption as people like to try them on. That is less important with most sports equipment though.

4. DICK’S remained profitable in the 2007-2009 recession with profit margins running around 3%. However, 3% is a long way down from the current levels.

5. During the pandemic, DICK’S changed its business model to fulfill most of its online sales from its stores. However, many other retailers now do this too with little apparent financial impact.

6. DICK’S has repurchased 4,362,000 shares during the first 9 months of fiscal 2022. However, this was more than offset by notes that converted to stock and employee stock compensation. Total shares outstanding increased from 52.0 million on January 29, 2022, to 57.0 million on October 29, 2022 after 7.8 million of shares issued in the conversions. Most notes are now converted.

7. The short ratio is currently 5.6 days with 28.1% of the float sold short. This could be a catalyst if short sellers are forced to liquidate in the face of a rising stock price.

Takeaway

I have a sell recommendation on DICK’S. Even without a recession, they are facing a reversion to the mean on sales and profit margins and the after effect of pulled forward demand. DICK’S is more exposed to a recession than most retailers due to its merchandise being mostly discretionary.

There is a real risk that the stock price can drop to pre-pandemic (2019) levels. The stock traded between $30 and $50 over the 10 years prior to the pandemic. The store base is not much different than 5 years ago. The stock price did drop from a high of $129 in August 2021 to $75 in June 2022, in anticipation of the reversion to the mean. However, operating results remained strong and they have since rallied back to $129 after a third quarter earnings upside surprise. But the market has been fooled by the good times lasting longer than in some other industries. There are too many headwinds for that to continue much longer. DICK’S is not a growth company. It is a strong but slower growing company that is just overpriced. While I am not going to try to predict which quarter things start to slow, I do expect that within a year. There is little upside here with margins and likely soon revenues falling. My one year price target is $60.

Be the first to comment