naphtalina/iStock via Getty Images

Investment Summary

From the Portfolio Manager’s desk

Many equity strategies were hammered in FY22′ as the market finally laid weight to true fundamentals and unwound the high-beta/growth trade. Losses were most pronounced in long/short and directional managers, except those tilted to a value bias, who claimed outsized return. As such, low-beta and quality strategies agreed most with investors across the bulk of the year. This meant that balanced portfolios with broad exposure to commodities and alternatives retained strategic alpha, whereas active management were the winners on the tactical side.

Retail liquidity has been swept up across many pockets of the market, leaving allocators plenty of safety margin to work with. The benchmark’s heavy weighting to tech/growth was trumped by more traditional sectors that benefit from the inflation-rates cycle, in particular, energy, utilities and resources. As a result of this structural rotation, cash-rich, fundamentally sound companies with quality factors were rewarded, with the trend continuing into the new year.

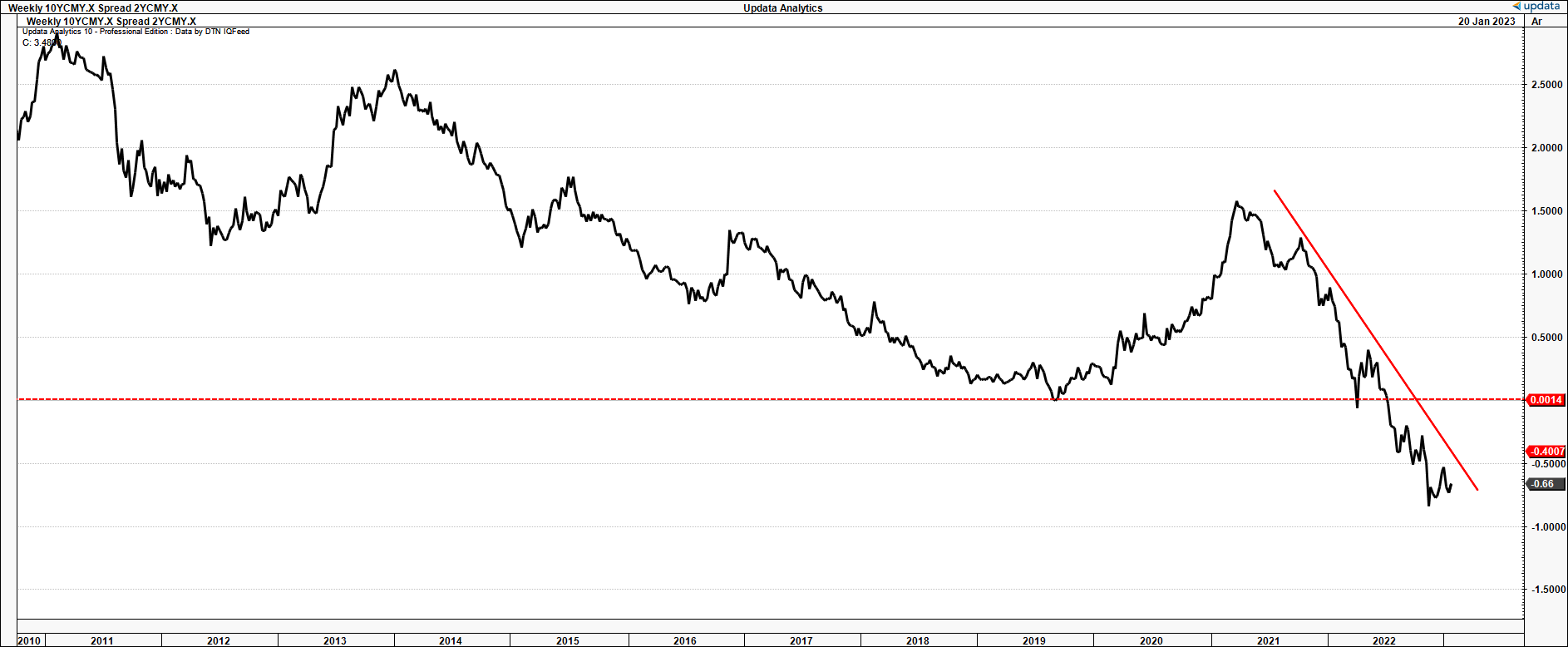

Meantime, the aggressiveness of central bank tightening policies continues to dominate the headlines, with the bond market pricing in a potential recession with the steep inversion of the 2/10yr treasury yield spread, if not that, then a potential deflationary period to come. UST yields have pulled back somewhat with the 10-year retracing off its 4.25% highs last year at a YTM of 3.5% at the time of writing. The long-end remains above 3%, with the 20yr still offering the best starting yields in terms of duration with a 3.77% YTM.

Exhibit 1. UST 2/10yr inversion its greatest in years, spelling potential economic and earnings recession

Data: Updata

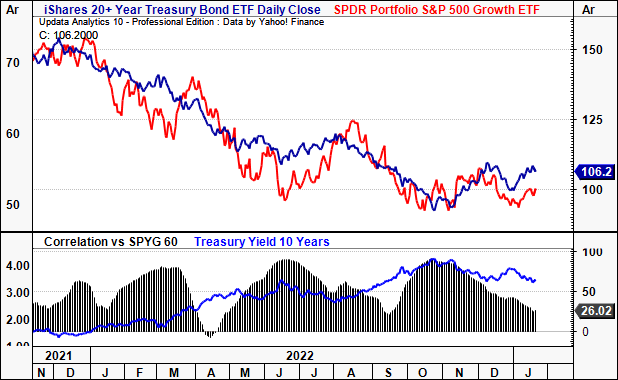

In spite of this, investors can lock in a 4.8% starting yield in buying the UST 6 month note, with most US Treasury notes from 1 month–2 year duration offering >400bps return at the time of writing. What this says for equities? A lot. Whilst the yield curve is inverted, the distribution of potential outcomes for the U.S. [and global] economy increasingly includes recession, and this means a recession to earnings as well. In regimes of the past, this has resulted in volatility and unpredictability of future cash flows, reducing the scope for valuation upside in many corners of the market. Presuming a similar outcome in the present day, long-duration growth equities are still unfavourable in our estimation, despite the stock-bond correlation rolling back below FY21′ levels [Exhibit 2], all while growth equities continue trending sideways.

Exhibit 2. Stock-bond correlation rolling over, yet growth equities continue tracking sideways

Data: Updata

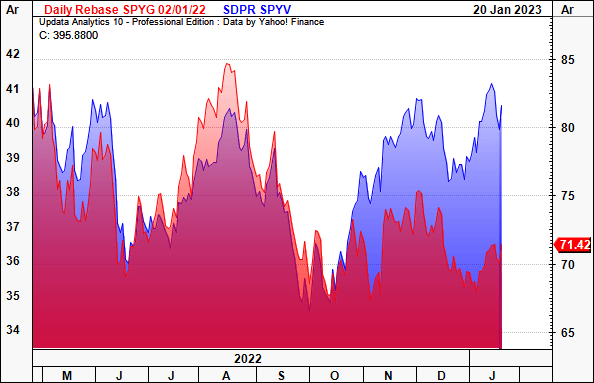

It’s no surprise, therefore, to see the growth/value axis diverge to its widest mark in over 2 years [Exhibit 3]. It’s important to consider this in weighting schemes when constructing equity portfolios in FY23′, to gauge where the allocation of capital will flow, and what this offers for individual names within the growth and value portions of the broad market.

Exhibit 3. Growth/value axis diverging to widest portion, implications for capital allocation into the new year.

Data: Updata

We factored all of these points in our appraisal of DICE Therapeutics, Inc. (NASDAQ:DICE), after the stock rallied hard at the back end of FY22′ before consolidating to the downside. We wanted to see how the market was playing DICE, and what to potentially expect in the name this year. Here we took a deep technical approach to achieve this, eyeing where and how investors are positioning in the name. Net-net, we see risks to DICE re-rating to the upside, and rate the stock a hold for now.

Momentum around DC-806 compound

DICE recently completed its Phase 1 clinical trial studies for its investigational compound, DC-806. The compound is administered orally and is targeting interleukin-17 (“IL-17”). If you didn’t already know, IL-17 is a pro-inflammatory cytokine that is critical in regulating the human immune response. This ranges in the form of various infectious disease, and, in particular, the development of autoimmune conditions. It is primarily produced by a subset of CD4+ T-helper cells, known as T helper 17 (“Th17”) cells, which is important for the DC-086 hypothesis.

IL-17 has been established as one of the key mediators in the pathogenesis of psoriasis, a chronic autoimmune disorder identified by an abnormal keratinocyte proliferation and inflammation of the skin. Numerous studies have demonstrated an increased frequency and activation of Th17 cells in the peripheral blood and lesional skin of psoriasis patients, both of which are responsible for the overproduction of IL-17.

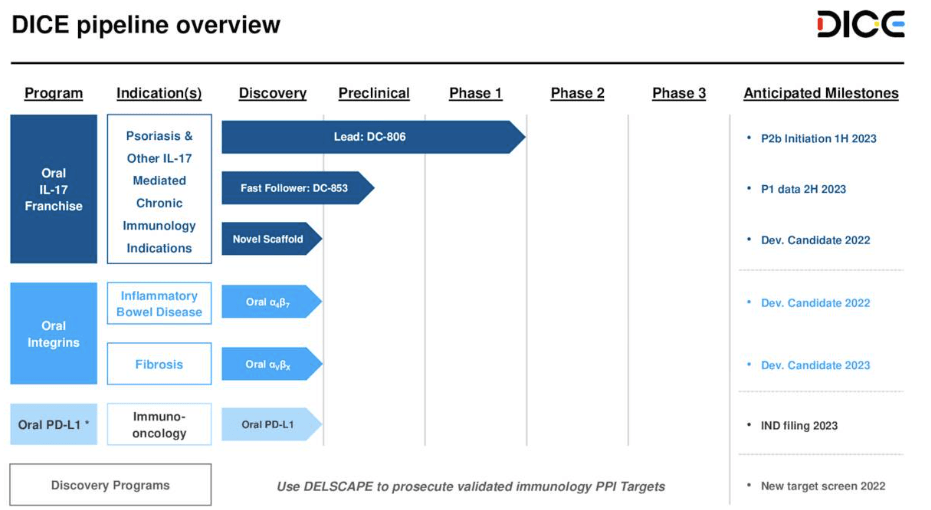

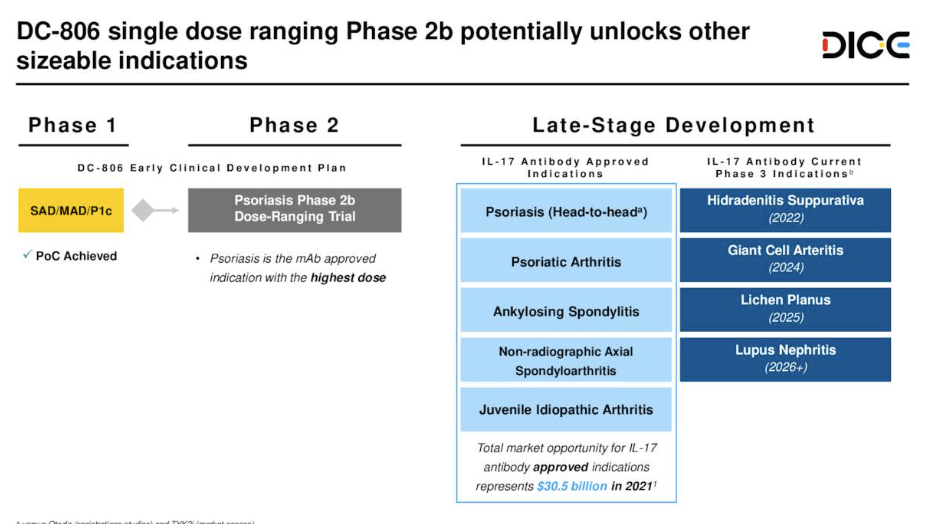

It is at this point where DICE’s hypothesis in DC-806 comes into play. The company’s phase 1 pipeline for DC-086, broken into parts a., b., and c., delivered positive top-line data in October last year.

DICE clinical pipeline

Data: DICE Investor Presentation

The Phase 1c portion, enrolled a high-dose group [n=8] at 800mg bi-daily, a low-dose group at 200mg [n=13], and 11 patients in the placebo group. It measured the mean percentage reduction in Psoriasis Area and Severity Index (“PASI”) from baseline after 4 weeks of treatment as its primary endpoint. Results showed that the mean percentage reduction in PASI from baseline was 43.7% in the high-dose group compared to 13.3% in the placebo group [p=0.0008]. As such, we expect DICE to continue with the 800mg regime looking forward. The trial also included an exploratory biomarker analysis, which demonstrated dose-dependent IL-17 target engagement, rapid onset of action, with direct inhibition of IL-17 signalling. Safety data also held up well across all groups.

Therapeutic strategies targeting IL-17 have already been developed as treatment options for psoriasis, such as Secukinumab [by Novartis] and Ixekizumab [Eli Lilly], each targeting the IL-17 pathway, and each already being approved for the treatment of psoriasis. Hence, if successfully approved and commercialized, the DICE will be coming up against these names in the marketplace.

DICE’s next steps for DC-806

Data: DICE Investor Presentation

Nevertheless, it is the momentum around its DC-086 label that had investors jumping behind DICE in FY22′. Whilst only in its phase 1 stage, any news around the compound looks to be key to the investment debate looking ahead. In that regard, whilst difficult to forecast a launch curve and future cash flows right now, we needed more insights into market positioning in the stock to guide our potential strategy and execution looking ahead, and, to see if DICE is a buy right now or not.

DICE advanced technical analysis

It’s imperative we have a good understanding of how the market is playing DICE in order to guide price visibility looking ahead. Make no mistake, the market is a constant auction house, with demand and supply key to understand in the absence of revenues or earnings.

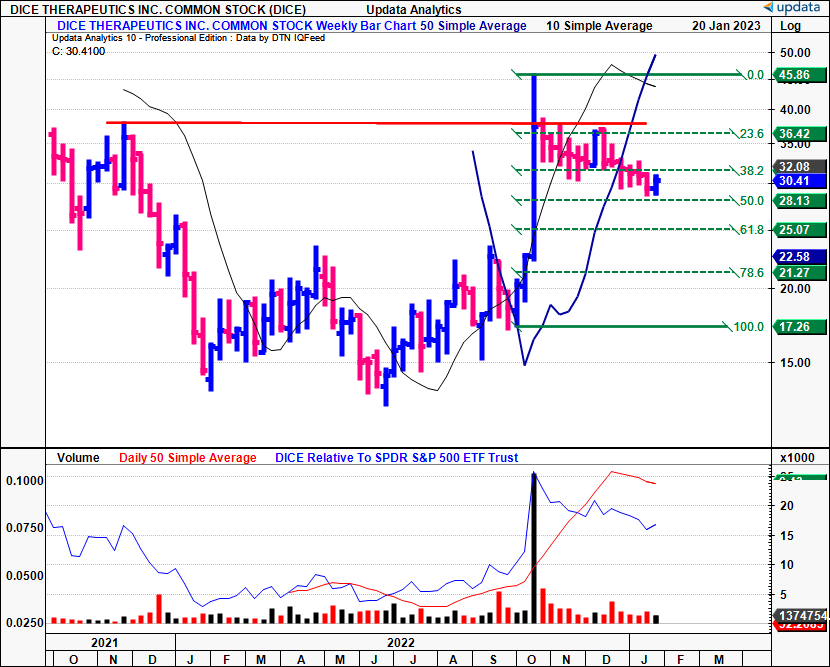

You’ll see that, in October last year, DICE ran up the page after its DC-086 update. As a reminder, the company listed on the NASDAQ in September 2021. The reward was short-lived, however, and the stock has pulled to the downside for the last 14 weeks.

Tracing the fibs up from the September lows to the October high, it appears the next targets are set to be $28 and then $25, should it continue at the current trajectory. It managed to hold the line over the past 2 weeks, however, volume was equally as low in both instances.

Exhibit 4. DICE pullback off October FY22′ highs, next targets to $28 then $25 [note: weekly bars, log scale]

Data: Updata

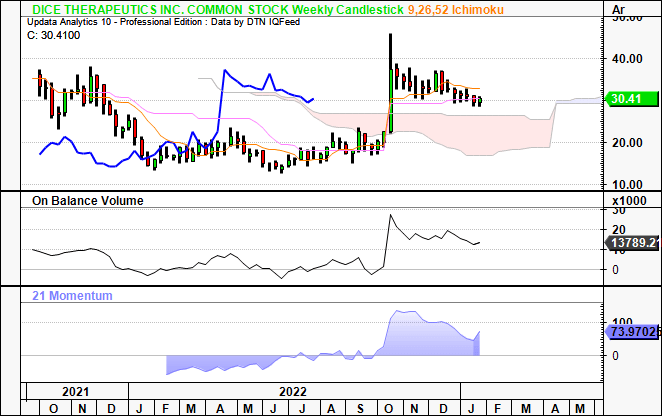

Looking at a longer-term horizon, the trend appears it could be bullish – but only by a margin [Exhibit 5]. Shares are still trading above cloud support, but the lagging line is testing the cloud top after riding the level for the last 4-5 weeks. A break below the cloud would see us adopt a bearish stance. Momentum has also fallen back, but not to the point where the rate of price change has stalled. After widening, the cloud has crossed to the upside, whilst longer term volume has flatlined. Immediately, $30 looks to be a key level of support that must be held into the coming 2-3 months, based on the current market price, but there is additional scope to see it rate to ~$17 at the lower bound of the cloud.

This tells us that the prevailing trend might still be bullish, and that demand still might be present at the current levels. This is a key question we now seek to answer.

Exhibit 5. Weekly trend remains bullish, with lagging line testing the cloud top

Data: Updata

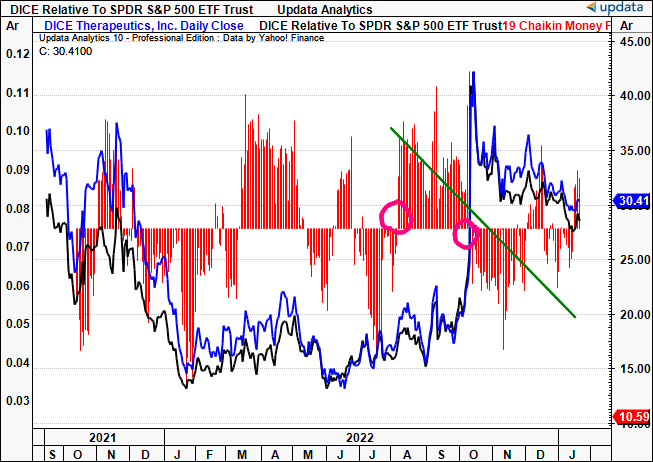

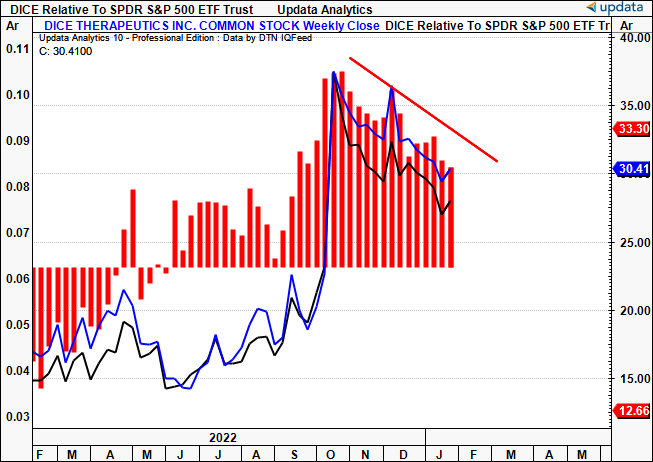

We get objective information on demand and supply levels [buyers, sellers respectively] by observing the money flows into DICE equity in the charts below [Exhibit 6, Exhibit 7]. As shown, investors [likely ‘smart-money’] were early onto the move early back in October, with inflows starting as early as August on a daily basis [left hand circle]. They were equally as fast out of the upside as well, exiting positions rapidly after the stock ran up the page to the c.$41 mark [right hand circle]. As such, the stock now attracts 15.5% short interest, which could be interesting if price action reverts back up, causing a wave of short covering at the current marks.

Exhibit 6. Daily money flows into/out of DICE equity – investors were early on the mark with each direction of the move

Data: Updata

On a weekly basis, the money outflows are less pronounced, demonstrating that investors are still net buyers of DICE on a weekly basis. The key question is exactly what kind of demand is present.

Exhibit 7. Weekly inflows/outflows into DICE equity

Data: Updata

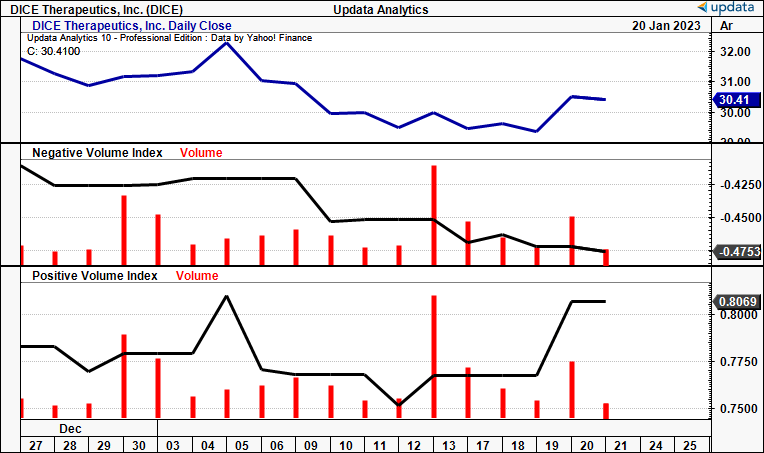

We can observe the spread between institutional and retail order flows by looking at the negative and positive volume indices, respectively (“NVI”; “PVI”) [Exhibit 8]. We’re looking to see the NVI spike up with up-moves in the DICE share price, as evidence of institutional buying momentum. As seen below, the opposite has occurred, in fact, it’s been all retail inflows across the month of January. This is important as it tells us that the ticket sizes tied to each respective order may be small, and the overall positions taken in the stock may be too small to see a reversal back to the upside.

Exhibit 8. Absence of institutional momentum on the back of recent price action in DICE

Data: Updata

That’s not to say that it can’t happen, however. Enough demand from any portion of the market can be substantial enough to drive equity prices, especially when considering leverage and derivatives exposure – something that isn’t shown via the NVI and PVI.

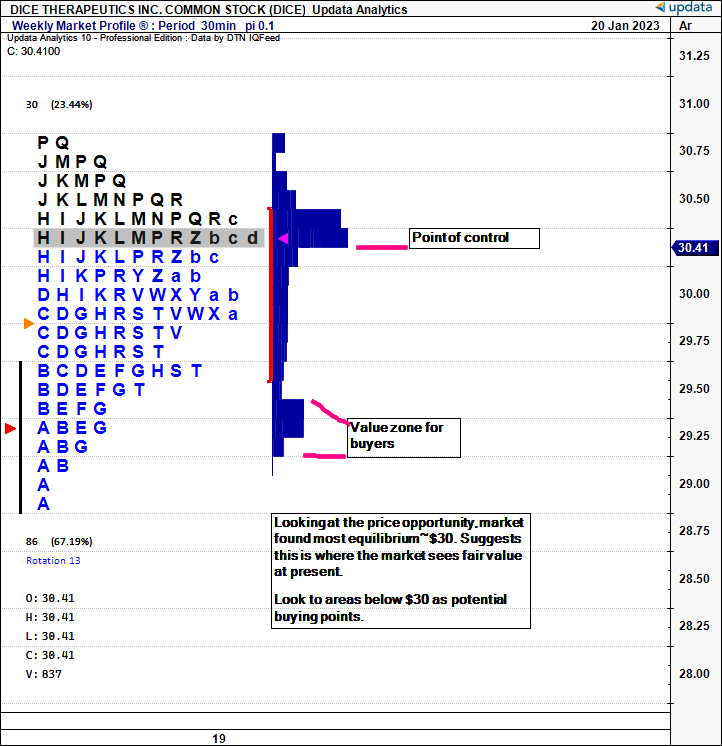

As such, we turned to the market profile for January to see where the DICE share price has achieved most equilibrium across the last few weeks [Exhibit 9]. Market profile charts illustrate at what points a stock price has traded, and in particular, how long [in time] it has spent there. This is different to a conventional chart, where time is a constant, no matter what price. In the chart below, each letter corresponds to 1 hour. The volume histogram is plotted vertically next to the corresponding price action.

You can see in the chart the stock has spent the majority of the new year at the $30 level [grey highlight]. This is known as the point of control, and demonstrates where the market has assigned fair value for DICE over these past few weeks. The red bracket is where 70% of the trading price range occurred. What you need to know is that all prices/letters below the point of control represented a good buying opportunity for investors over the past 2 weeks, in other words, the value zone for buyers. Those who bought here in January haven’t incurred a loss [just yet, anyway]. You can also see there’s been a reasonable amount of buying volume at these marks. This is where we’d define the ‘smart money’ as buyers.

As such, the question now immediately turns to whether these zones will continue to represent as a value zone for buyers looking ahead.

Exhibit 9. Market profile of DICE share price illustrating majority of price traded at $29.50–$30

Data: Updata

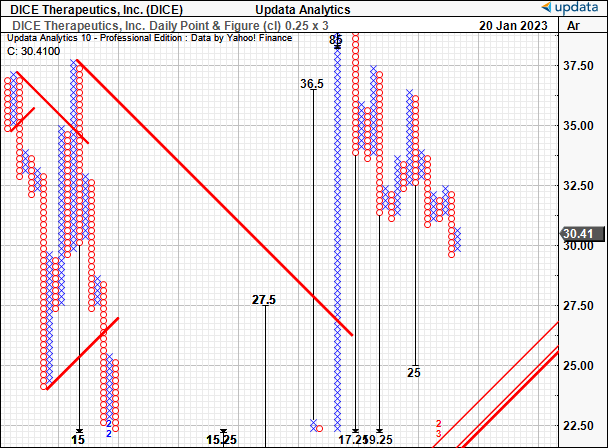

To answer this question, point and figure charting is the solution. We are huge advocates of this method of charting as it presents a cleaner view of price action that can be used to derive price targets with reasonable accuracy. As seen below, the next target we have is a downside number to $25, after the $29.25 target was taken out earlier this month. Note, there’s also another target as low as $17, which tells us that going long at this point in time could lead to downside risks on the chart. Those who bought at the ranges shown in Exhibit 9 are potentially stuck, and may sell to clip losses early, creating further downside momentum.

Exhibit 10. Downside targets to $25, then $17, supported on Fibonacci ranges listed earlier

Data: Updata

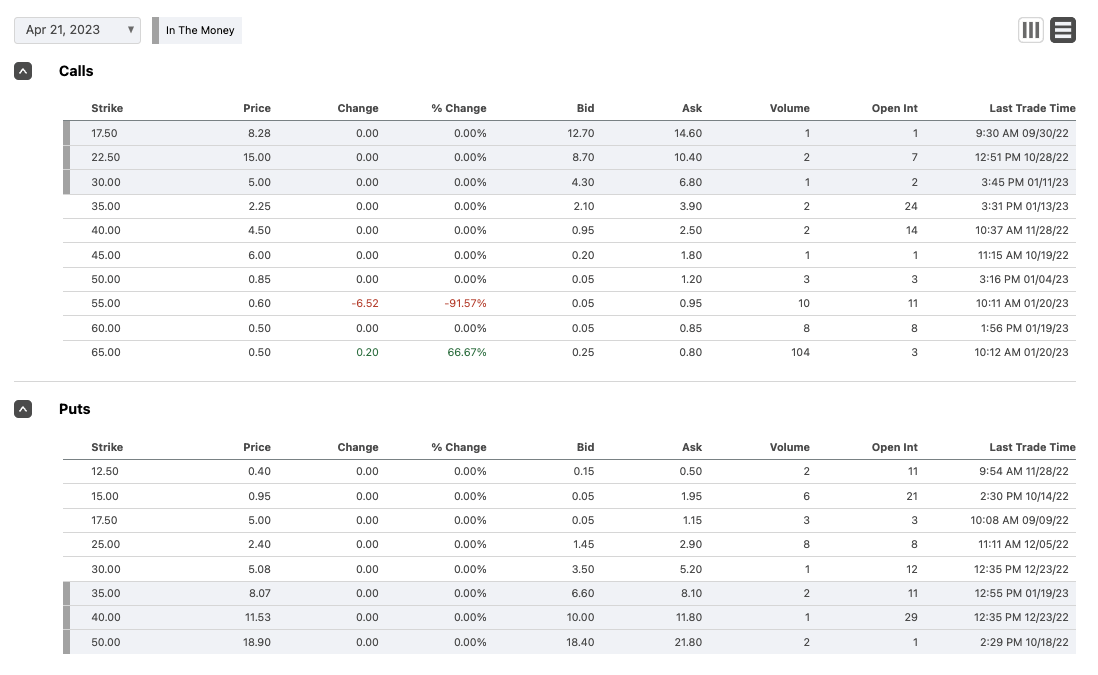

This is also reflected in the options chain for DICE into April FY23′, with put/call numbers peaking at $21.80 and $14.60, respectively.

Exhibit 11. DICE options chain, April FY23′

Data: Seeking Alpha, DICE, see: “Options”

In short

Dice has come off a large high and has consolidated to the downside. Investors have repositioned in the stock and the issue we have found via the various technical studies presented here is that demand has crumbled from larger buyers, reducing the propensity for DICE to re-rate to the upside in our opinion. In this vein, we rate DICE a hold and await more comprehensive data to suggest enough demand is present to spark another rally. For now, it appears as if there is downside risk, and we look to the next target of $25, then $17.

Be the first to comment