ArtistGNDphotography/E+ via Getty Images

Investment Thesis: While Despegar.com has been seeing a significant rebound in revenue, low growth in cash and earnings levels make the stock too risky at this point in time.

In a previous article, I made the argument that Despegar.com (NYSE:DESP) could be in a good position to see upside on the basis of a rebound in growth across the Brazilian market – with this market having accounted for 33% of transaction volume in Q4 2021.

With that being said, earnings came in below expectations in the last quarter, which has made investors largely shy away from the stock.

investing.com

As an emerging markets stock in what remains a volatile time for the travel industry – Despegar.com is by no means without risk. While revenue growth has been rebounding – the purpose of this article is to investigate whether this would be sufficient for the stock to rebound longer-term.

Performance

As mentioned, earnings recently came in below expectations for Q1 2022, with GAAP EPS of -$0.45 missing expectations by $0.29. However, revenue of $112.4M still beat expectations by $7.55M.

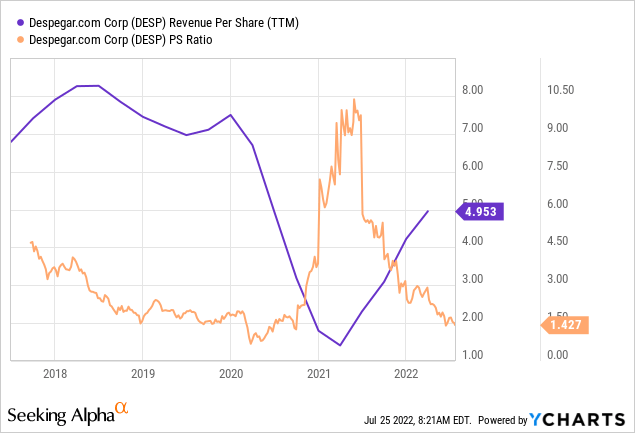

Particularly, when we look at the price to sales ratio – we can see that the stock is trading near a 10-year low on this basis while revenue per share has been showing a significant rebound:

YCharts

In this regard, while earnings have yet to rebound into positive territory – revenue growth is moving in the right direction.

In addition, Q1 2022 saw gross bookings of $803.9 million – which was up by 118% year-on-year and accounted for 69% of levels seen in Q1 2019.

Moreover, Despegar.com has limited exposure to currency risk given that the company holds its cash reserves in U.S. dollars in the United States and the United Kingdom.

However, when we compare the company’s cash position for Q1 2019 and Q1 2022 – we can see that the company’s cash to current liabilities ratio has decreased quite considerably:

| March 2019 | March 2022 | |

| Cash and cash equivalents | 311657 | 235175 |

| Current liabilities | 345862 | 479910 |

| Cash to current liabilities ratio | 90.11% | 49.00% |

Source: Figures sourced from Q1 2019 and Q1 2022 Despegar.com Earnings Releases. Cash to current liabilities ratio calculated by author.

From this standpoint, while the company has been seeing a rebound in revenue – Despegar.com has less cash available than previously to be able to meet its short-term debt obligations.

Looking Forward

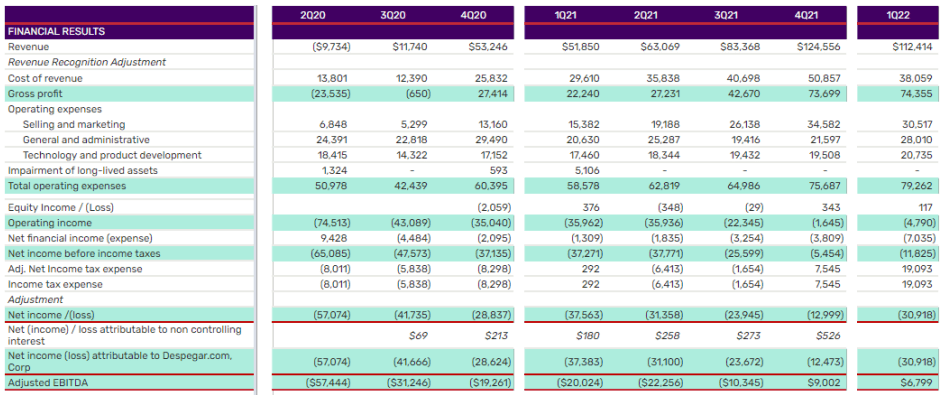

The main issue with Despegar.com at the current time is that operating expenses are simply outpacing that of revenue growth. We can see that total operating expenses in Q1 2022 are up by 55% from Q2 2020.

Despegar.com Q1 2022 Financial Results

In this regard, it is not clear as to whether Despegar.com can continue to grow revenue sufficiently so as to outpace operating expenses – even if we are seeing revenue start to approach pre-COVID levels.

Moreover, a geographical breakdown shows that the Brazilian market showed the most growth in transactions and gross bookings outside of Latin America.

Despegar.com Q1 2022 Financial Results

Recently, with the announcement that Despegar.com is to acquire 100% of online travel agency ViajaNet, we can expect that transaction volume across Brazil will come to account for a larger portion of overall revenue going forward.

With that being said, inflation of 12.1% in May across Brazil could significantly hamper travel demand as the country starts to head into its summer season. From this standpoint, while Despegar.com gains greater exposure to the Brazilian online travel market – adverse macroeconomic conditions could significantly harm revenue growth.

Conclusion

To conclude, Despegar.com has seen a significant rebound in revenue. However, the lack of cash growth is concerning – and this company will ultimately have to show that it can translate revenue growth into bottom-line earnings before we start to see upside. In this regard, while Despegar.com has potential for a longer-term rebound – I take the view that the stock is too risky at this point in time.

Be the first to comment