simonkr

Thesis

Desktop Metal (NYSE:DM) is taking a stab at a high-volume approach to additive manufacturing, by acquiring various related manufacturing companies. Of these companies, ExOne, was acquired for $575 Million in 2021. DM, along with its other acquisitions, now trades at around a $580 Million Market Cap. Investors now have the opportunity to buy DM and its other acquisitions for the price paid of a single, innovative, and well-sought-after company in ExOne. Furthermore, DM exhibits high growth, yet similar valuation, compared to other additive manufacturing companies who have flatlined in growth. For this reason, I believe now is the best time to take advantage of this opportunity for those bullish in the additive manufacturing industry.

What is Metalcasting?

Before explaining why ExOne will be paramount for the future of manufacturing, let’s review the 5000-year-old Industry in Metalcasting. A good definition comes from the American Foundry Society:

Metal casting Process (American Foundry Society)

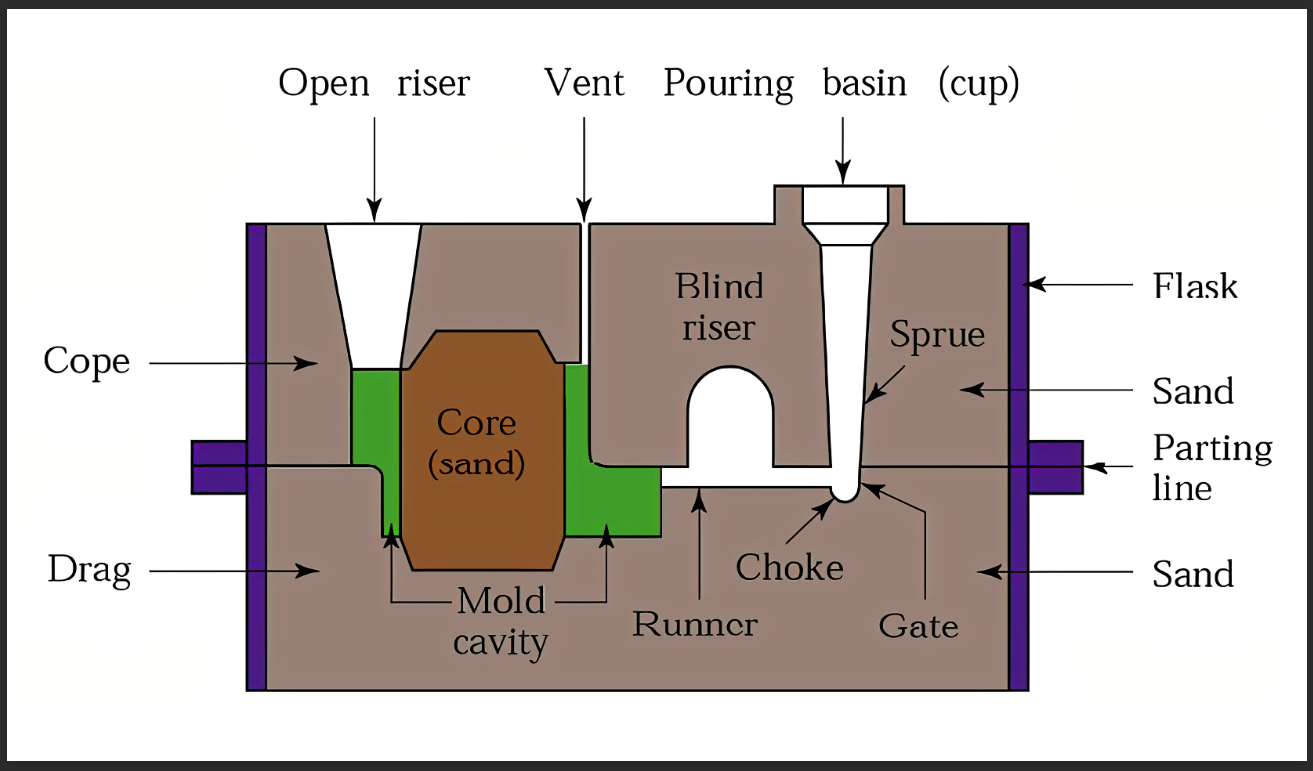

Of this definition, we will focus on “sand”, more specifically, sand cores. For reference, sand cores make the internal geometry of a casting.

Casting Diagram (Blog Spot Mechanical Inventions)

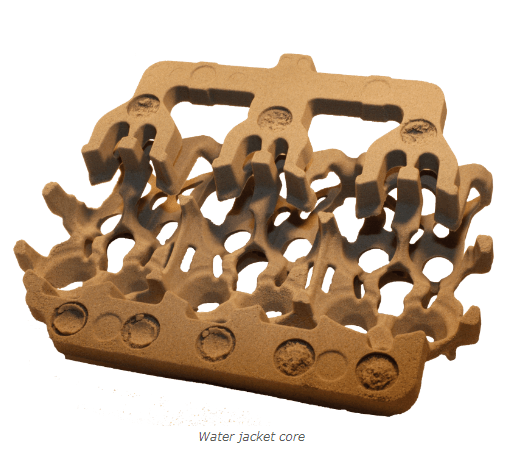

Water Jacket Core (Flow 3D)

To make these cores, separate tooling is required, called core boxes. These are typically made out of aluminum or hardened polyurethane resins. Sand and binder is typically rammed or blasted in these boxes and hardened to make the completed core. Depending on part complexity, this tooling can be extremely expensive to manufacture. There are also constraints with this manufacturing process, regarding design. First, in order to correctly draw the casting, the core should be made to have draft or slanted features to avoid sticking. Second, negative features must be accommodated by loose pieces or adding more cores to the mix. Simply put, the more complex a casting becomes, the more time and energy is needed to properly cast it. This severely limits design possibilities and overall progression in manufacturing.

Urethane Core Box (Le Sueur)

There are other issues that can arise if a design needs to be modified during production. This requires either manufacturing a new core box or reworking another to accommodate the design. Again, this limits design capabilities. However, ExOne offers a solution that is currently being used in industry with success.

The ExOne Solution

ExOne’s solution to this problem is their binder jet system, specifically the S-max series. This system uses binder jetting to 3D print sand cores and is currently being used in American pattern shops such as Hoosier Pattern and Humtown with great success. Foundries are coming to the conclusion that the current state of 3D printing sand casting is useful for two scenarios:

- Prototyping a new design.

- Mass producing complex parts.

However, 3D printing sand cores is not cost advantageous when mass producing simple parts yet. I use the word “yet” here on purpose.

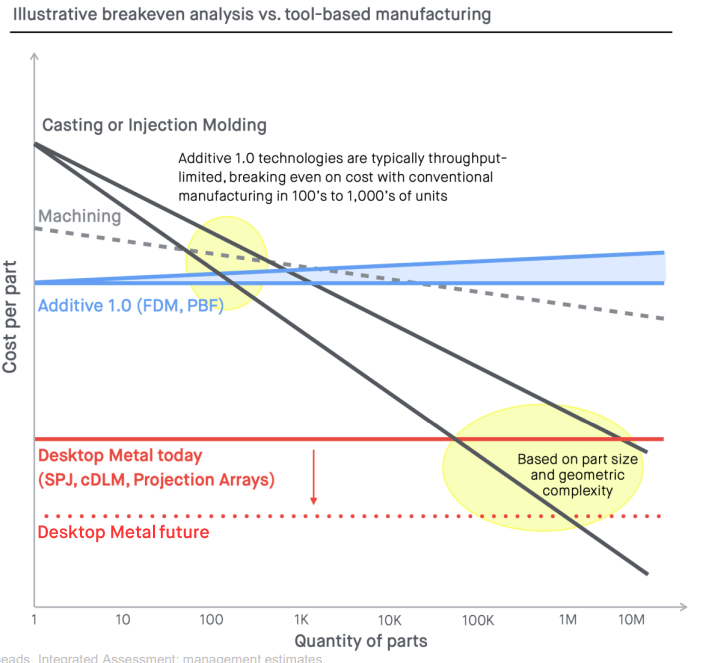

This is also referred to as break-even analysis and explained in DM investor relations presentation. Essentially, there is a point where 3D printing parts are no longer efficient versus just using traditional manufacturing practices.

DM Breakeven Analysis (DM Investor Relations Presentation)

However, this is just based on standard FDM machines. ExOne’s binder jet system selectively deposits resin into a bed of sand, and hardens to form the desired geometry. This process produces 3D printed sand cores 100x faster than traditional FDM, and the best part is – it’s only getting more efficient.

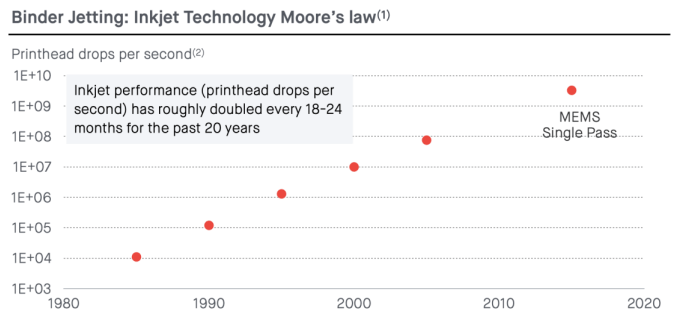

Moore’s Law

In 1965, Gordon Moore observed that roughly every two years, the number of transistors on microchips will double. If you are even remotely familiar with the semiconductor industry, this observation is the lifeblood of progress. This same progress can be observed in binder jetting printhead drops per second, explained in the same slide of DM investor presentation.

Moore’s Law DM investor Presentation (DM investor Presentation)

This is why I use the word “yet” when describing progress earlier. Binder jetting is already incredibly useful in industry, and since its still in its infancy, there is so much room for growth.

Valuation

I will value DM through three ways:

- Comparing growth and Price/sales multiples across industry.

- Revenue multiple analysis based on expectations.

- Discussion on DM acquisitions.

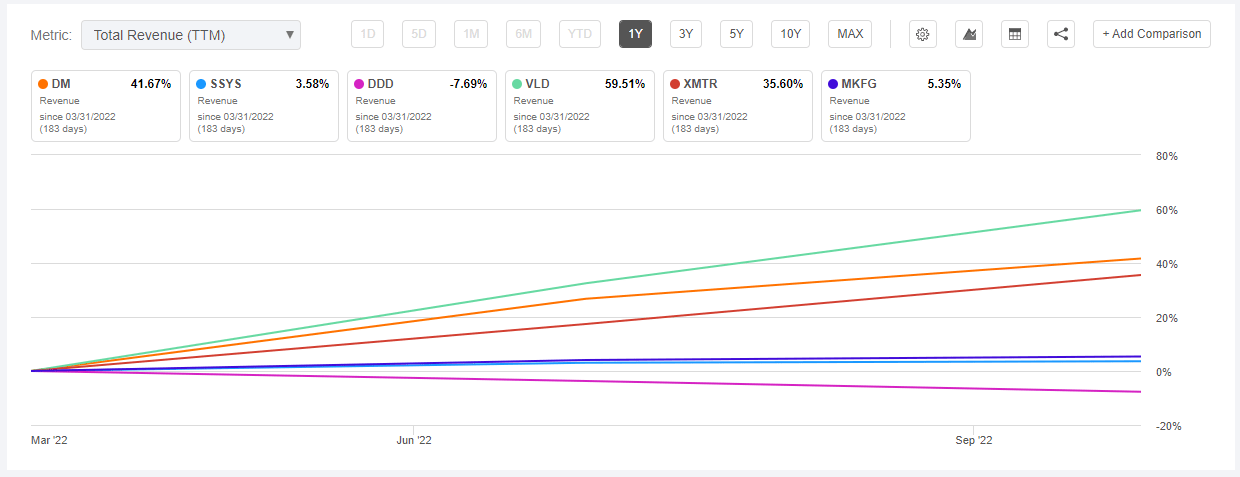

For the industry comparison approach, we can look at revenue growth compared to competitors. Out of primary additive manufacturing tickers, Xometry (XMTR) and Desktop Metal DM and (VLD) are the only ones showing significant growth over the last year. XMTR is also primarily an outsource service/software company with DM more closely related to the other manufacturing companies. VLD is showing 20% more growth than DM but is also more than double the current Price to Sales ratio.

Desktop Metal Revenue Growth (Seeking Alpha)

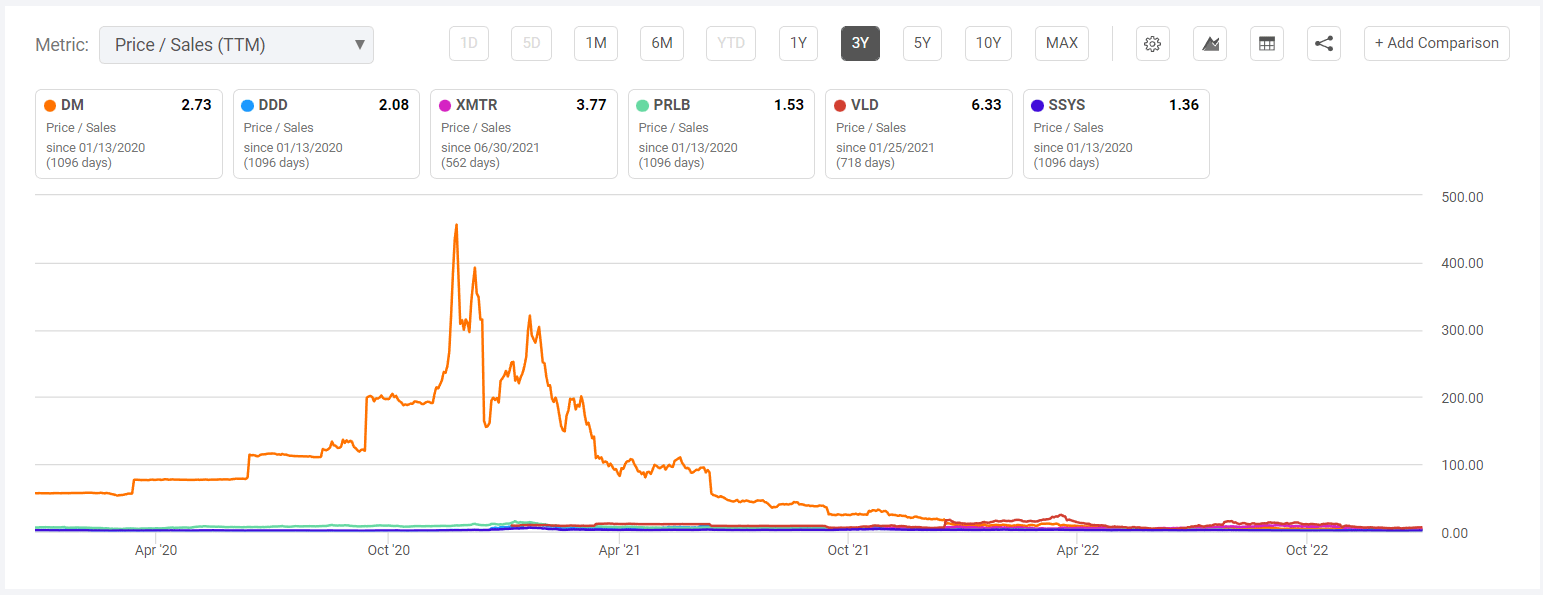

DM is at reasonable Price/Sales ratio now, compared to the industry. In other words, the investor now has an opportunity to pay the same price for growth, when compared to other additive manufacturing companies.

Additive Manufacturing Price/Sales (Seeking Alpha)

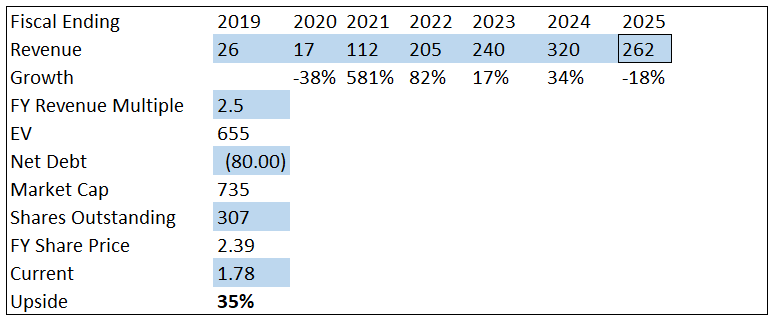

The second way we can value DM is by using revenue expectations from Seeking Alpha. At a current revenue multiple of 2.5x, we can see a 35% upside based on the lowest analysts estimate in 2025.

Desktop Metal Revenue Multiple (Author and Seeking Alpha)

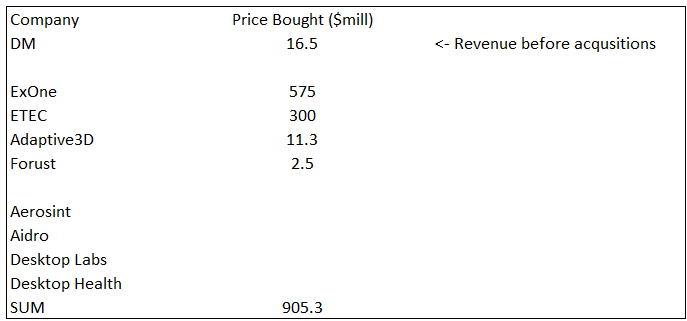

The third way we can value DM is by discussion of their acquisitions. DM currently trades at the price paid of ExOne. Since we are bullish on ExOne, we can value DM as if it will be the only revenue producer of this mini conglomerate of binder jetting solutions. This is highly unlikely but builds a factor of safety. If that were the case, DM acquired ExOne at roughly 8x Price to Sales and thus we can value DM at 8x Price to Sales as whole. This is large but not completely far off from VLD current valuation.

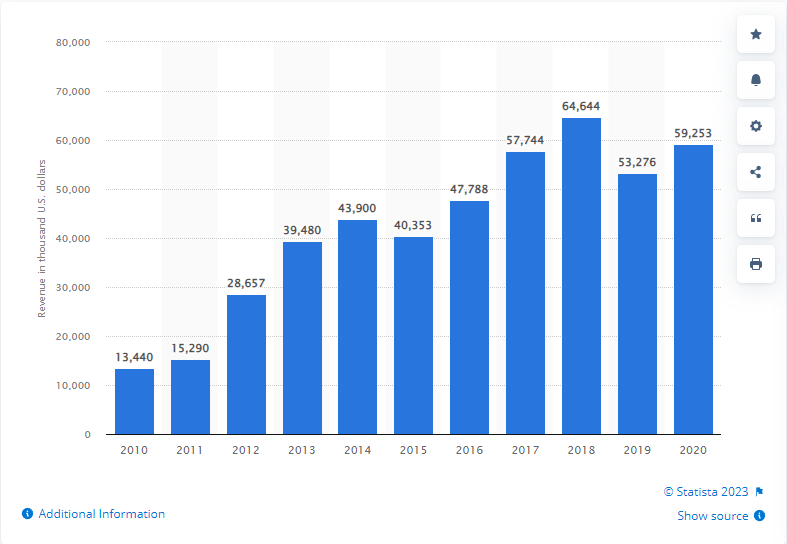

Desktop Metal Acquisitions (Author Research) ExOne Revenue Growth (Statista)

Conclusion

Overall, I’m valuing DM as if ExOne is the only useful company it has acquired recently, which is highly unlikely. Even in this case, DM seems very close to fair valued, with upside. ExOne is currently used in industry today as a 3D printing solution and growth is expected to follow. Since I am excited about this industry as whole, and is now at relatively close valuations, I will be dedicating small percentage of the portfolio to DM.

Be the first to comment