VanderWolf-Images/iStock Editorial via Getty Images

At the time I’m starting to write this report, Delta’s (NYSE:DAL) Q4 earnings call is still ongoing. But despite results being strong the guidance for Q1 came in below expectations and the stock is trading down 4% to 5%. I will have a look at the results and the guidance.

Delta Air Lines: A Strong Buy But The Stock Tanks

Seeking Alpha

On Jan. 6, I published a report explaining why I reversed my view on Delta Air Lines from a Strong Sell to a Strong Buy over the course of 2022. With the stock down 4% at the time of writing you can wonder whether that was the right call. Realistically, in a week since publication you cannot assess whether a call was good or bed. You can only assess whether things headed in the right direction and I would say it did as shares are up 4.3% even after the 4% drop and shares of Delta Air Lines are still outperforming the market.

In fact, I was actually too conservative. I saw the possibility that Delta’s results for the fourth quarter could disappoint due to flight service disruptions around Christmas. However, Delta managed to beat its EPS forecast of $1.35-$1.40 per share by eight cents measures from the high end of the range. The reason was that what Delta lost during the winter storm, it made up for it and then some in markets where it competes directly with Southwest Airlines (LUV). So, really strong quarter where the company benefited from the problems at Southwest Airlines. Revenues also beat expectations by $720 million, which also showed strength of the operations and environment during the quarter.

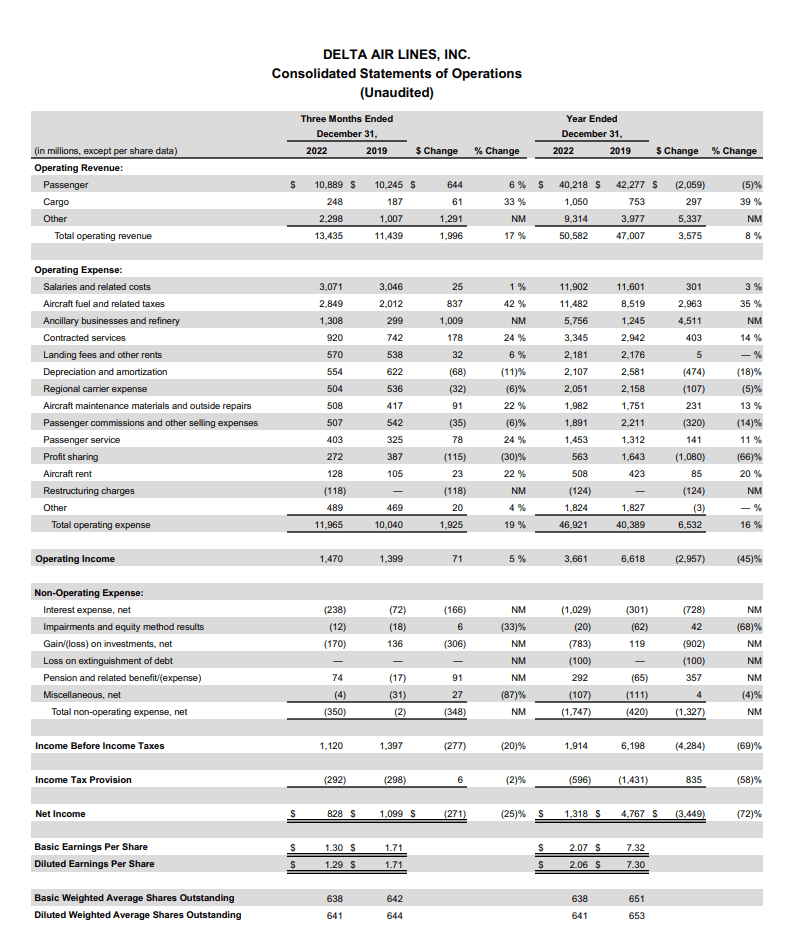

A Deeper Dive In The Results

Delta Air Lines results (Delta Air Lines )

I’d say that investors took the Q4 performance for granted, but it’s still useful to look at where the company is compared to pre-pandemic levels. So, revenues were up 6% compared to pre-pandemic levels and cargo revenues were up 33% driven by higher capacity and unit revenue leading to 17% top-line growth and that is on 91% capacity deployed with unit revenues up 17%. Interesting to note is that capacity on Domestic and Latin America is still down 8% to 9%, while Asia Pacific is down 50% providing upside and Atlantic operations were up 8%.

Analysts at this point are obviously looking whether they see any signs of softening demand, but this was not the case revenue per available seat mile grew by 1% sequentially. Ex-fuel unit costs or CASM-X grew by 6%. There’s some impact in there from the winter storm that drove up unit costs.

Overall, results were good we see operating income was 5% ahead of pre-pandemic levels with a 10.9% margin which was in line with the 11% that was guided for. I don’t want to go over every cost element in detail but overall we see that Delta exceeded expectations driven by topline growth exceeding expectations. For the full year, revenue is up but profitability is down. However, this is not an extremely useful thing to look at as those numbers incorporate the improvement during the year instead whereas somewhat of an annualized measure of the current performance would provide a better view on where the company is now in terms of revenues and profits.

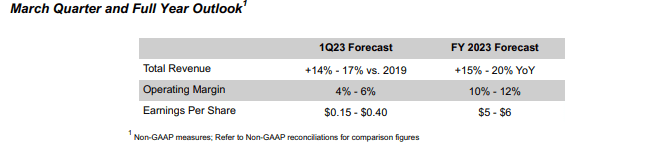

Why Delta Stock Trade Down?

Delta Air Lines guidance (Delta Air Lines)

The reason why Delta shares traded down was the Q1 guidance which came in extremely light in the $0.15-$0.40 whereas analysts were expecting $0.64 per share and we see margins half of the 10%, we’d like to see. There are two reasons for that. The first is maintenance activity in preparation for network restoration and the summer season which will frontload some costs and even out over the entire year and labour costs are going up. However, importance to keep in mind is that its full-year forecast remains in place with earnings per share of $5 to $6.

The Opportunities For Delta

I can certainly understand the concern on higher labor cost because when unit revenues will slide, labor costs will not and those unit cost put a three-point damper on CASM improvement. However, overall we see that Delta is going to restore its capacity this year and they carry some costs for that in the first quarter as well. Furthermore, by increasing domestic stage length and expanding international capacity, unit costs will come down. So, yes if you are worried about softening unit revenues then the higher labor costs are not a nice thing but there also are opportunities for Delta.

In the Pacific region, there are opportunities to increase revenues in Japan, South Korea and Australia. For Asia, China is a big question mark as the pace of the recovery there is going to be dictated by demand and likely with a layer of politics as well, but overall internationally while significantly recovered there is room for a lot more while also domestic operations should start running more efficiently as well and even then by year-end it is not expected that asset utilization is fully recovered providing even more room for efficiency to improve. The company used the pandemic to increase market share in coastal hubs and it will now focus on improving its position at core hubs, which provide for lower cost capacity expansion. So, we see a strong operational plan and from financial point of view we also see that Delta Air Lines wants to retire high interest debt. So, we see that the company wants to recover, create value for customers which translates into value for Delta Air Lines which it will then use to deleverage. That is something that makes so much sense that it is silly to actually write it down, but too few companies actually take this approach.

Conclusion: Buy The Delta Dip

Today’s share price movement of 4% in the negative direction in my view is somewhat of a knee-jerk reaction. It’s solely based on the Q1 guidance which incorporates higher labor and maintenance costs as Delta recovers virtually all of its capacity. I can understand at this point that there’s not much attention for the extremely strong beat for Q4 2022, but there is a danger in weighing the negatives heavier than the positives. Because Q1 2023 might be disappointing, but Q4 2022 was good and overall Delta sticks with its full year guidance for 2023 so I would say investors are too much focused on the Q1 forecast. That might be because while a guidance for the entire year has provided, there are uncertainties on demand strength and economic health for the entire year even though Delta expects supercycle or maybe better worded anti-parallel demand with demand moving up while economic indicators could be moving in the opposite direction.

Nevertheless, even with the uncertainties I do believe that the stock price reaction is somewhat overdone as Delta Air Lines has been improving the fuel efficiency of its fleet and its now recovering capacity with a more efficient fleet with pre-pandemic plans such as a restructuring of the Asia operations, upgauging and higher focus on maintenance coming to fruition which the company can ultimately use to deleverage and return value to shareholders.

Be the first to comment