Halina Pinchuk/iStock via Getty Images

Barrick Gold (NYSE:GOLD) is the second largest gold miner in the world and has a diverse portfolio of mines, including six Tier One gold mines which are considered to be some of the highest quality in the industry. In the past year, Barrick’s free cash flow has been impacted by higher capital expenditures due to expansions and special maintenance, but these expenses are not expected to occur every year. Barrick’s all-in sustaining costs for gold and copper have increased in recent years due to inflation and the company’s financial performance is closely tied to the price of these commodities. The company has provided a guidance for its financial performance over the next five years, which is based on the price of gold and copper.

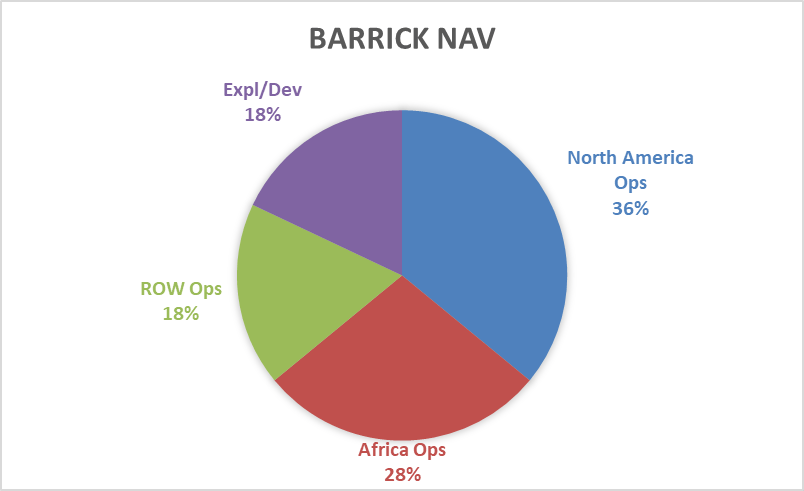

The Importance of Barrick’s North American Operation Cannot be Understated

The future performance of Barrick shares is joined at the hip with the performance of its producing North American assets. The reasoning behind this thesis is simple. Approximately 33% of Barrick’s Net Asset Value [NAV] is derived from its North American operations and represents its largest geographical exposure. Over the next five years, Barrick expects to grow its production within North America while also lowering the overall cost as economies of scale factor in. Outside of North America, roughly 25% of its NAV is derived from its African operations with 16% coming from its LATAM and PNG operations. The remaining ~16% asset base consists of exploration and development stage assets.

Author estimate

Because of the importance of North America to Barrick, it is important to understand these operations as well as Barrick’s strategy for them. As it relates to the North American operations, Barrick Gold has outlined several key priorities for the company, including a focus on safety and the progression towards zero harm. The company aims to continue building a strong, engaged workforce and to develop its people in order to create a pipeline of future leaders.

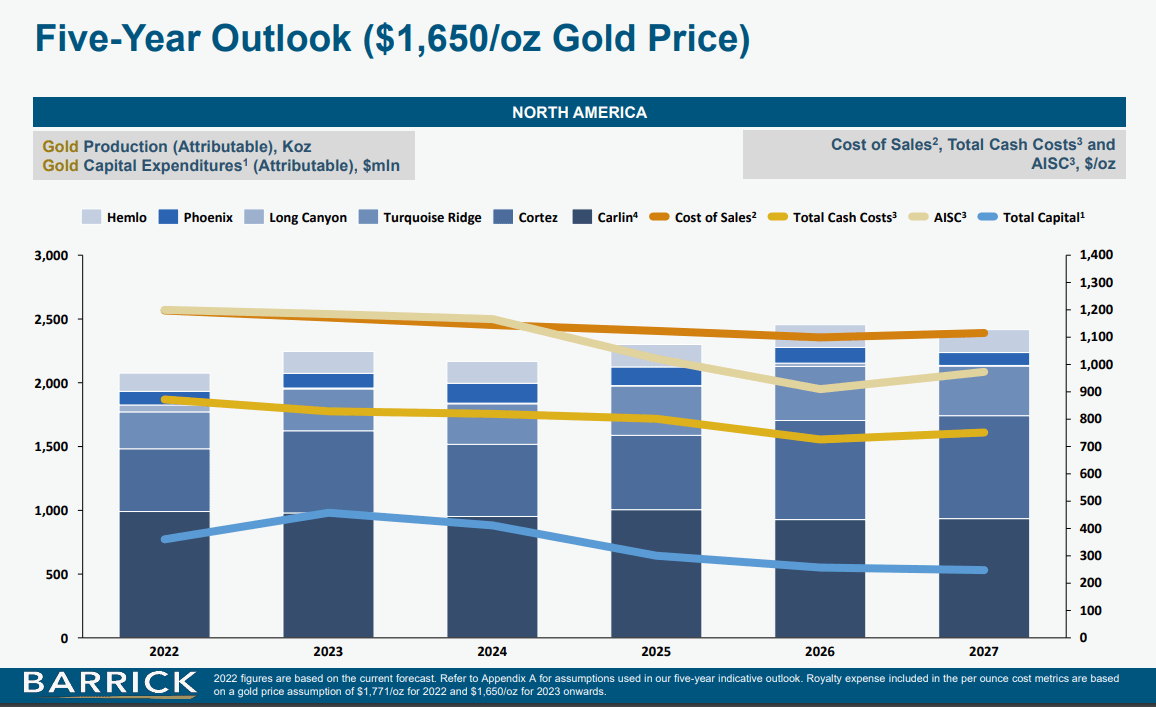

Barrick plans to increase production and reduce costs in North America

Barrick Gold remains on track to meet its 2022 production guidance, although per ounce costs are expected to be higher than initially forecast due to higher energy prices. In the long term, Barrick has a robust production profile with significant growth initiatives planned in order to sustain production over the next 10-15 years.

Barrick Gold

Barrick’s North American production is expected to rise from ~2M oz to ~2.4M oz by 2026. Total CAPEX is expected to peak in 2023 at ~$450M and then steadily decline as the growth initiatives translate to higher production run-rate. Additionally, costs are expected to decline by over 20% as higher production offsets the fixed costs associated with the production centers.

The devil is always in the details

Nevada Gold Operations: Barrick Gold is on track to meet its 2022 production guidance, although per ounce costs are expected to be higher than initially forecast due to higher energy prices, which have a direct and indirect impact on the company’s cost structure and supply chain. The company has completed mining at the Long Canyon Phase 1 project and is currently conducting a review to optimize the potential mine life extension. Barrick has a significant level of flexibility to balance ongoing production and development at the complex. The company also has a robust 10-year production profile with several growth initiatives planned in order to sustain production over the next 11-15 years. These initiatives include the development of the North Leeville and REN projects, the extension of high-grade material at the Turquoise Ridge project, the development of the Robertson project, and the implementation of new mine access at the Upper Rita K project to deliver high-grade underground tonnage and efficiencies. The Nevada Gold operations are the crown jewel of Barrick’s North American portfolio. I believe that Barrick is positioned to deliver on its plans in Nevada. Barrick has a long and successful history with these projects and the key personnel have a track record of delivering within project constraints.

Barrick Gold

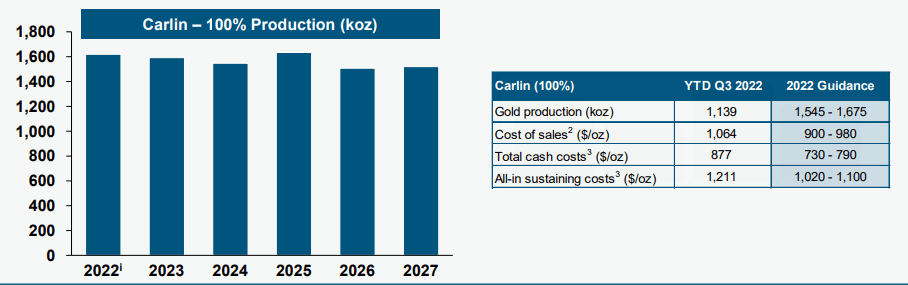

Carlin Gold Operations: Barrick Gold has made investments in processing improvements at the Gold Quarry roaster and Goldstrike autoclave in order to increase throughput capacity and convert from RIL to CIL. The company has also extended the life of the Gold Quarry oxide mill/concentrator until H1 2023 and is exploring opportunities to recover additional oxide ounces from the continuation of open pits. In addition, Barrick has brought forward the West Barrel layback at the Goldstrike open pit to support the Ren infrastructure and open new exploration areas. The company is also implementing new portals to improve mining productivity efficiencies at Pete Bajo and Rita K. In the future, Barrick is looking at growth opportunities at the North Leeville, Upper Rita K, REN, and Horsham projects. The Carlin gold operations are rather complex and involve immense logistics. Typically, when companies are treading water in terms of production, costs tend to disappoint. In the case of Barrick’s Carlin Gold ops, the company expects to maintain status quo over the next five years from a production standpoint. I would not be surprised if the costs disappoint to the upside.

Barrick Gold

Cortez Operations: Barrick Gold is transitioning from the Pipeline Open Pit to the Crossroads Open Pit and expects to deliver high-grade oxide ore in Q4 2022. The company has also mined the first ore at the Goldrush project in Q1 2021 as part of ongoing exploration and development activities, with a Record of Decision expected in H1 2023. Barrick has also brought forward production from the Cortez Pits and is conducting feasibility and permitting work for the Robertson Open Pit. The company is also continuing to buttress the Cortez Hills Open Pit. In the future, Barrick is looking at growth opportunities at the Fourmile, Robertson, and Hanson target projects. Cortez is expected to bring impressive growth to Barrick’s North American portfolio. Given the number of moving pieces that have to fall in, slippages on cost and timelines are possible. However, Barrick tends to be a conservative operator so these slippages are likely to be mild.

Barrick Gold

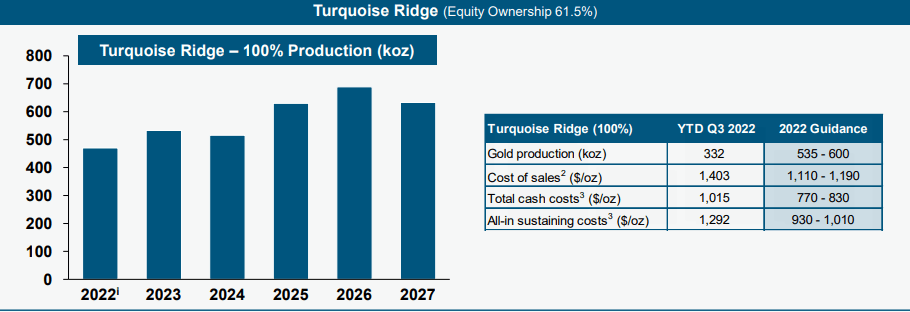

Turquoise Ridge: While this operation disappointed in 2022, Barrick Gold expects underground production to improve due to an increase in long-hole stope mining and the use of larger underground equipment. The company is also commissioning a Third Shaft, which will provide increased hoisting capacity, additional ventilation, and shorter underground haulage distances. Barrick is investing in process infrastructure, maintenance, and training at the Sage autoclave in order to improve throughput, reliability, and recoveries. The company has also extended the production timeline for the Vista Underground project to 2024, with the potential for further extension. In the future, Barrick is looking at growth opportunities at the Turquoise Ridge Underground Southern Extension, the Getchell Expansion, and the Turquoise Ridge to Twin Creeks Corridor.

Barrick Gold

Donlin is not expected to be greenlit any time soon. Barrick Gold is working on improving its geological understanding of the Donlin Gold project through the creation of large geological and mineral resource models. The company is also focused on advancing permitting, regulatory engagement, and trade-off studies for the project. Despite being satisfied with its ownership stake in Donlin, the company has noted that the project currently does not meet its investment hurdle rates. Given its optionality to higher gold prices, Barrick has no plans to divest from Donlin in the foreseeable future.

At Phoenix, Barrick Gold is focusing on flexibility in mine sequencing in order to maximize value from tri-metals production. The company has also produced and shipped the first batch of sulfide flotation concentrate to the Carlin roaster. Pit slope optimization and increased recoveries are being implemented to drive the addition of reserves and resources. Barrick is also working to re-establish Hemlo as a core contributor by improving underground efficiencies and addressing legacy infrastructure constraints to enable improved and consistent operational delivery. The company is also using updated geological modeling to refine drill targeting for growth areas and is conducting studies on a potential larger open pit with first production as early as 2027.

Barrick Gold’s ability to execute on its North American operations will be crucial in delivering on its five-year outlook. Most of Barrick’s growth is expected to come from its North American operations and Porgera in Papua New Guinea. Therefore, the success of these operations is of utmost importance. While I believe the NGM operations will deliver as planned, we can expect modest slippages on cost and timelines from Carlin gold operations and Cortez. Phoenix and Hemlo are not large enough to be pivotal to Barrick’s fortunes in North America.

Barrick Valuations

Bloomberg

Barrick trades at a premium to virtually all of its peers. The premium is somewhat deserved given its scale and liquidity. However, historically, Barrick’s shares have enjoyed their share of volatility. For this reason, patience can be rewarded for those willing to let the market come to them.

At present, Barrick’s valuation is on the higher end of its 10-year EV/EBIDA range. However, this could be conservative if gold prices remain strong. As a potential entry point, it may be wise to consider buying Barrick around 7x EBITDA, or around $16.50 per share.

Bloomberg

Barrick Gold is an excellent for generalist investors seeking exposure to a highly liquid gold producer with a diversified asset base. As gold prices rise, it may be wise for investors to closely examine premier gold producers like Barrick. In a future article, I will cover Barrick’s African asset base and the company’s plans for it.

Be the first to comment