piranka

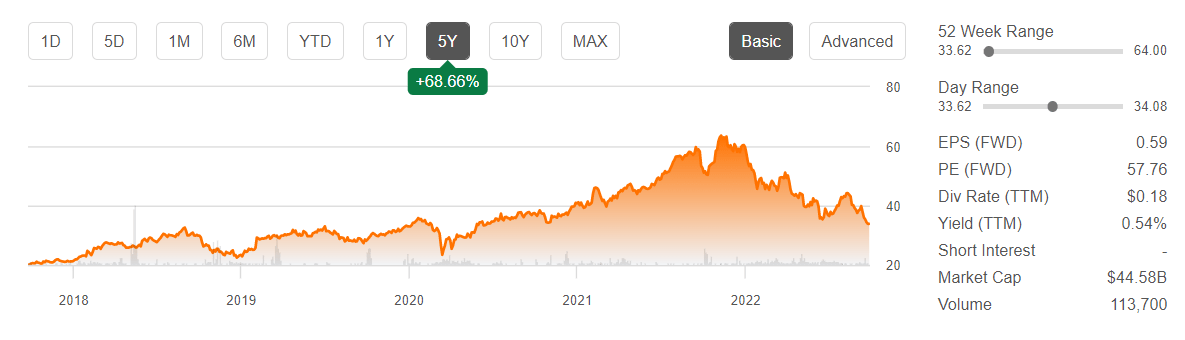

Enterprise tech, much like the rest of tech, has been a money-loser. Dassault Systemes (OTCPK:DASTY)(OTCPK:DASTF) used to lie above the rest. Its PE was consistently high, and the shareholder value creation has been very consistent and very substantial for many years. But it appears the market is offering it no quarter, as the price has declined almost 50% from its peak last year. We believe the market is right, and that Dassault Systemes should be avoided for the time being as uncertainties are still too substantial.

Dassault Systemes Price (Seeking Alpha)

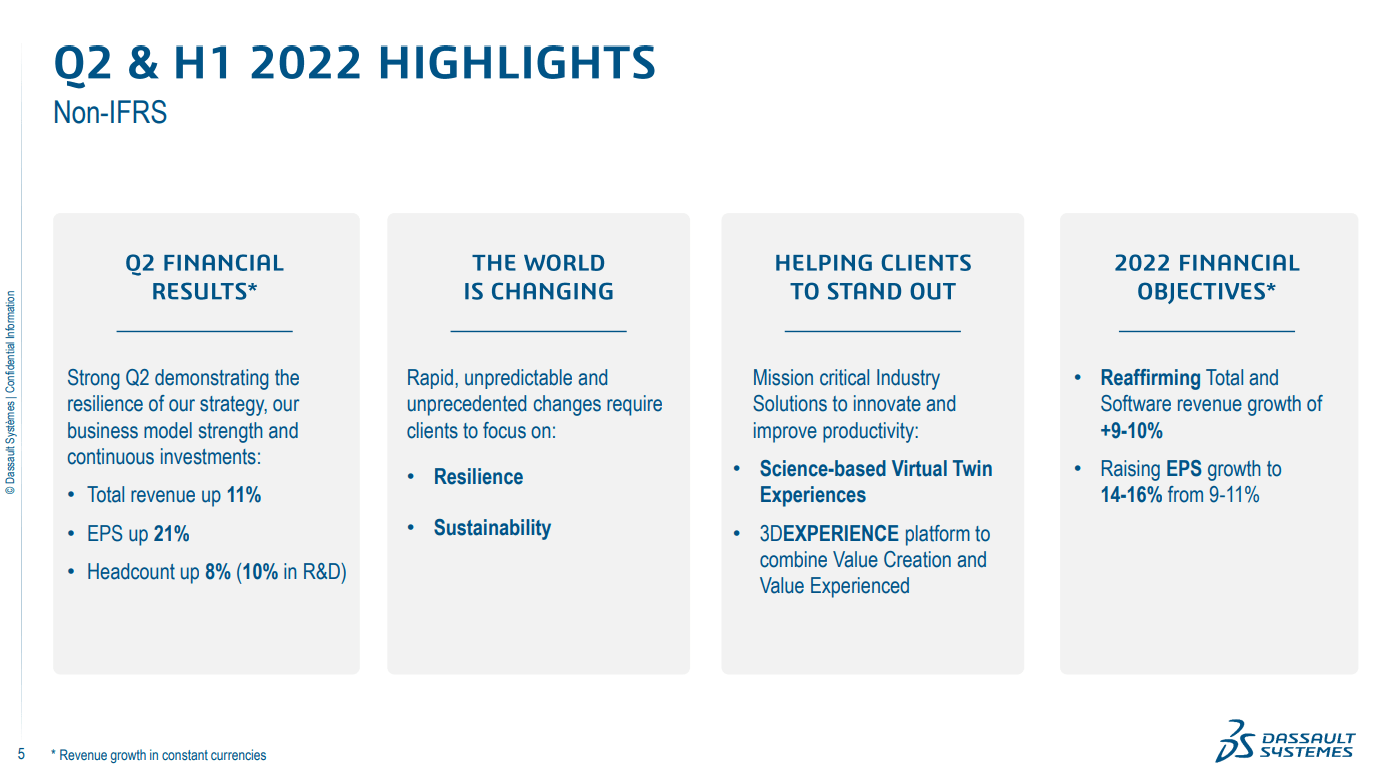

Quick Q2 Note

The Q2 results show what other enterprise tech showed, which was continuing growth despite some waves of rate hikes across the globe already having taken place. Dassault makes about 50% of its revenue in the US, so certainly the environment created by the Fed there is an appropriate analogue for its overall results.

Highlights (Q2 2022 Pres)

Revenue growth continued to be stable and relatively unimpeachable, and this was consistent with the last earnings season in big tech, and the bifurcations we saw between consumer and enterprise spending, where consumer confidence had dropped while corporate confidence had not.

EPS growth also looked strong, but the reality is that the major US exposure and an unhedged long position in the dollar was the primary contributor to EPS growth. Headline figures were around 20%, while the constant currency figures were around 10%. While growth is still respectable, we are seeing some gross margin pressure on the service revenue front baked into contracts as a result of labor inflation, consistent with the situation seen in other enterprise tech companies, although to a more limited degree due to the more meaningful software revenue exposures with Dassault.

Remarks

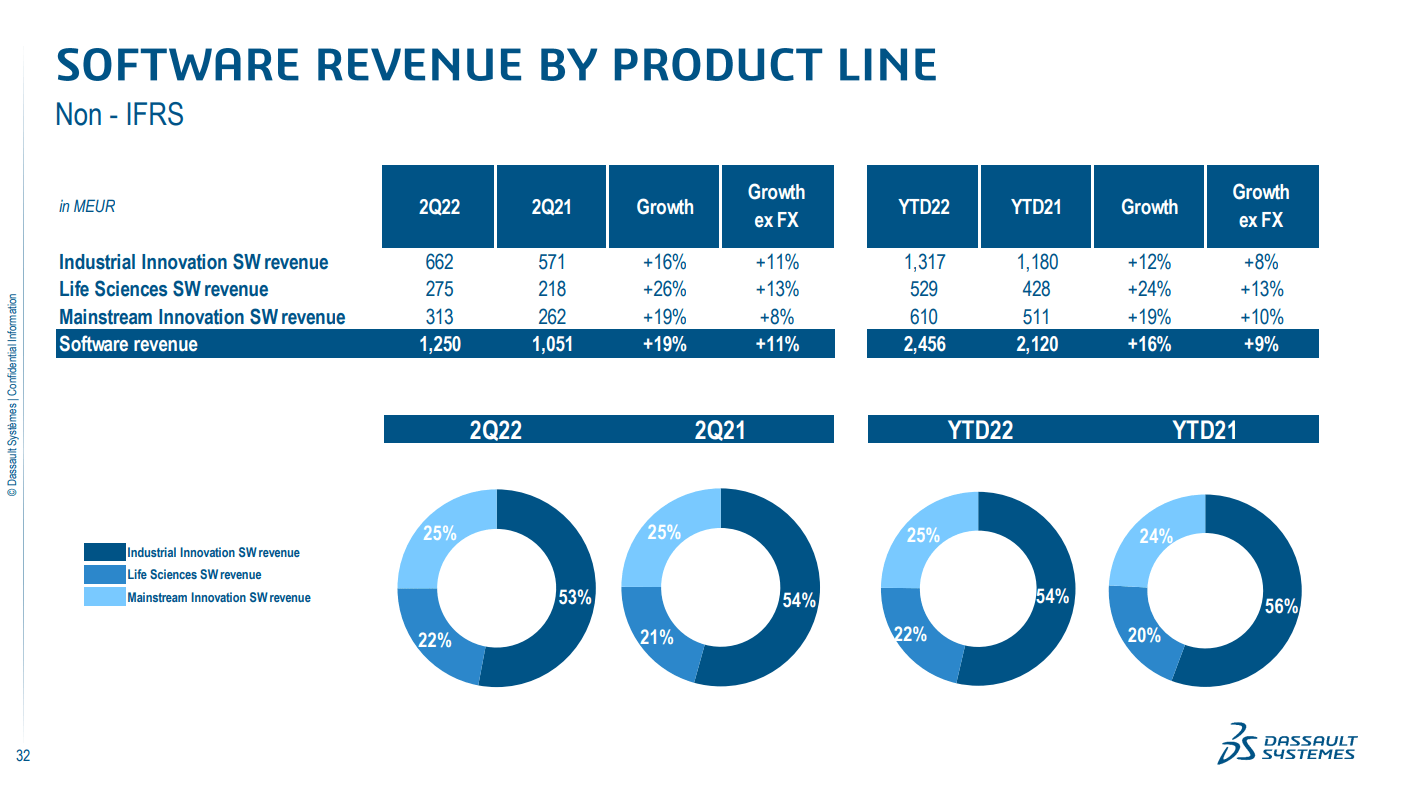

The majority of Dassault’s revenue can be considered software revenue, so the following end-market mix is a very direct representation of the company’s exposures and likely fortunes.

End-market Split (Q2 2022 Pres)

In our opinion, besides the life sciences business, there are end-market risks here. There is meaningful automotive risk and risk associated with other manufacturing businesses that deal in consumer durables that are the first to fall in a downturn. This is just for the industrial and innovation segment. On the mainstream innovation segment you start getting into the electronic and semiconductor territory, where inventories have gone from scarce to bloated, signaling another glut like in 2018. Life sciences are totally resilient accounting for about 20% of the revenue split.

What could this realistically mean for Dassault Systemes? As the macroeconomy becomes more of a concern, we are not arguing that Dassault is posed for any kind of collapse. In fact, its business model remains excellent, and recurring revenues can be relied upon, and most of the income here is recurring at around 80%. Customers are major and are unlikely to dial back on this cost area for the company. The problem is the growth trajectory. The company trades at around a 35x forward PE if you annualise current EPS. If 75% of your growth markets slow down entirely, where major discretionary spends on product development and R&D are paused, the expectations that support a still very high 35x PE will not be met. With the added fact that some revenue could be lost if new licenses aren’t sold, since not all the revenue is on a subscription basis, growth could in theory turn negative when a recession finally hits, and that recession is likely to be protracted, perhaps a full 2-year bear market cycle.

Overall, we see other cheaper enterprise tech ideas in the market like TeamViewer (OTCPK:TMVWF). We’d never take Dassault over them at their current relative multiples, but we wouldn’t take TeamViewer now either since sentiment is so decidedly against enterprise tech, and a latent hit could deflate expectations even further once consumer declines pass through or unemployment begins. It’s a pass.

If you thought our angle on this company was interesting, you may want to check out our idea room, The Value Lab. We focus on long-only value ideas of interest to us, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, our gang could help broaden your horizons and give some inspiration. Give our no-strings-attached free trial a try to see if it’s for you.

Be the first to comment