deliormanli/E+ via Getty Images

Overwhelming fear in the equity markets has created compelling opportunities for value investors looking to pick up high-quality stocks at a deep discount.

Within the homebuilder group of stocks, D.R. Horton, Inc. (NYSE:DHI) is our favorite deep-value pick for a medium-to-long-term investment horizon. For more diversification, investors may consider adding exposure to homebuilders more broadly through the iShares U.S Home Construction ETF (ITB) or the SPDR Homebuilders ETF (XHB).

In this article, we present the favorable macroeconomic forces that could boost earnings for homebuilders. We then focus more specifically on the reasons why we think D.R. Horton is well-positioned to outperform its peers.

At the time of writing, Seeking Alpha’s Quant Rating has a ‘Buy’ rating on all three of the tickers mentioned above (DHI, ITB, XHB).

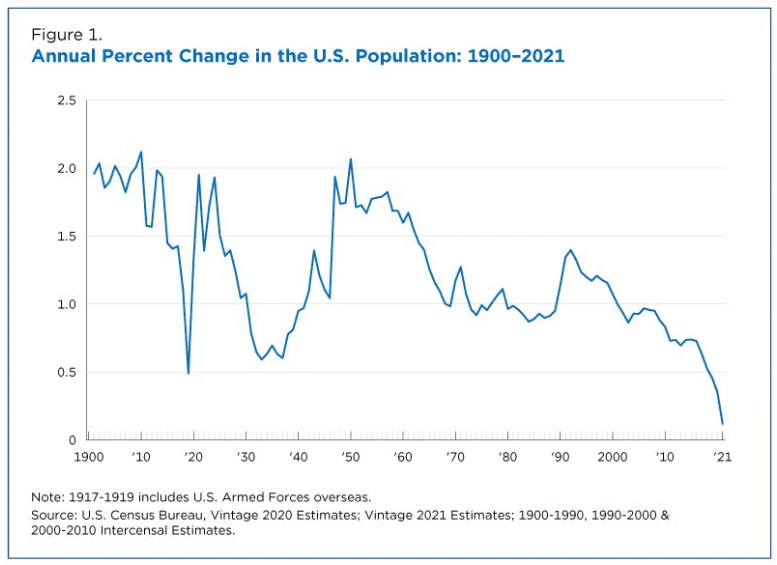

U.S. Immigration Rebound To Boost Demographics

A declining birth rate and stringent immigration controls imposed by the former Trump administration (2017-2020) have contributed to driving U.S population growth to a new historic low. According to a recent report published by the U.S Census Bureau, the country’s population grew by only 0.1% in 2021.

US Census Bureau

However, we believe that the U.S is undergoing a major demographic shift and that this decline in population growth will reverse in the next few years. We see encouraging evidence that a healthy rebound in immigration will soon become a key driver of this improvement in U.S demographics.

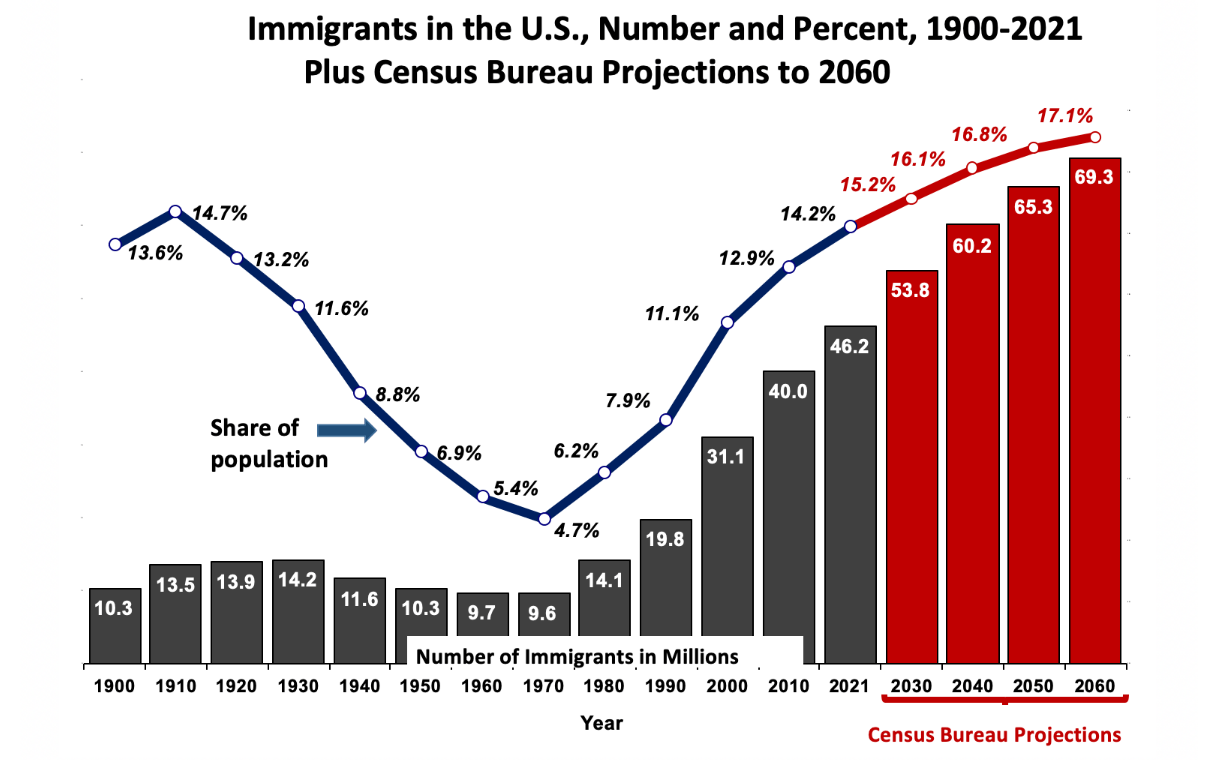

The Biden administration has been working to overhaul the U.S. immigration system and to fast-track approvals for a backlog of immigration applications. As of Q3 2022, this backlog stands at more than 8.0 million applications, according to data from the Department of Homeland Security’s U.S Citizenship and Immigration Services (DHS-USCIS). The Biden administration is also targeting skilled migrants and has relaxed rules for migrants with advanced degrees in STEM fields to access temporary visas and employment-based green cards.

Unlocking this source of migrant workers is crucial, as the U.S. economy is struggling to fill job vacancies in a tight labor market, while wage-price increases threaten to exacerbate mounting inflationary pressures.

The U.S. Census Bureau expects the share of immigrants as a proportion of the U.S. population to increase steadily, from an estimated 14.2% in 2022 to 17.1% by 2060.

US Census Bureau

This increase in migrant workers supported by the Biden administration’s efforts to relax immigration controls, and the resulting boost to U.S demographics, present favorable conditions for U.S. residential real estate in the coming years.

To be more precise, the particularly well-defined and highly predictable age-income profile of this wave of new migrants, suggests that multi-family and low to mid-end single-family real estate should benefit disproportionately from this demographic shift.

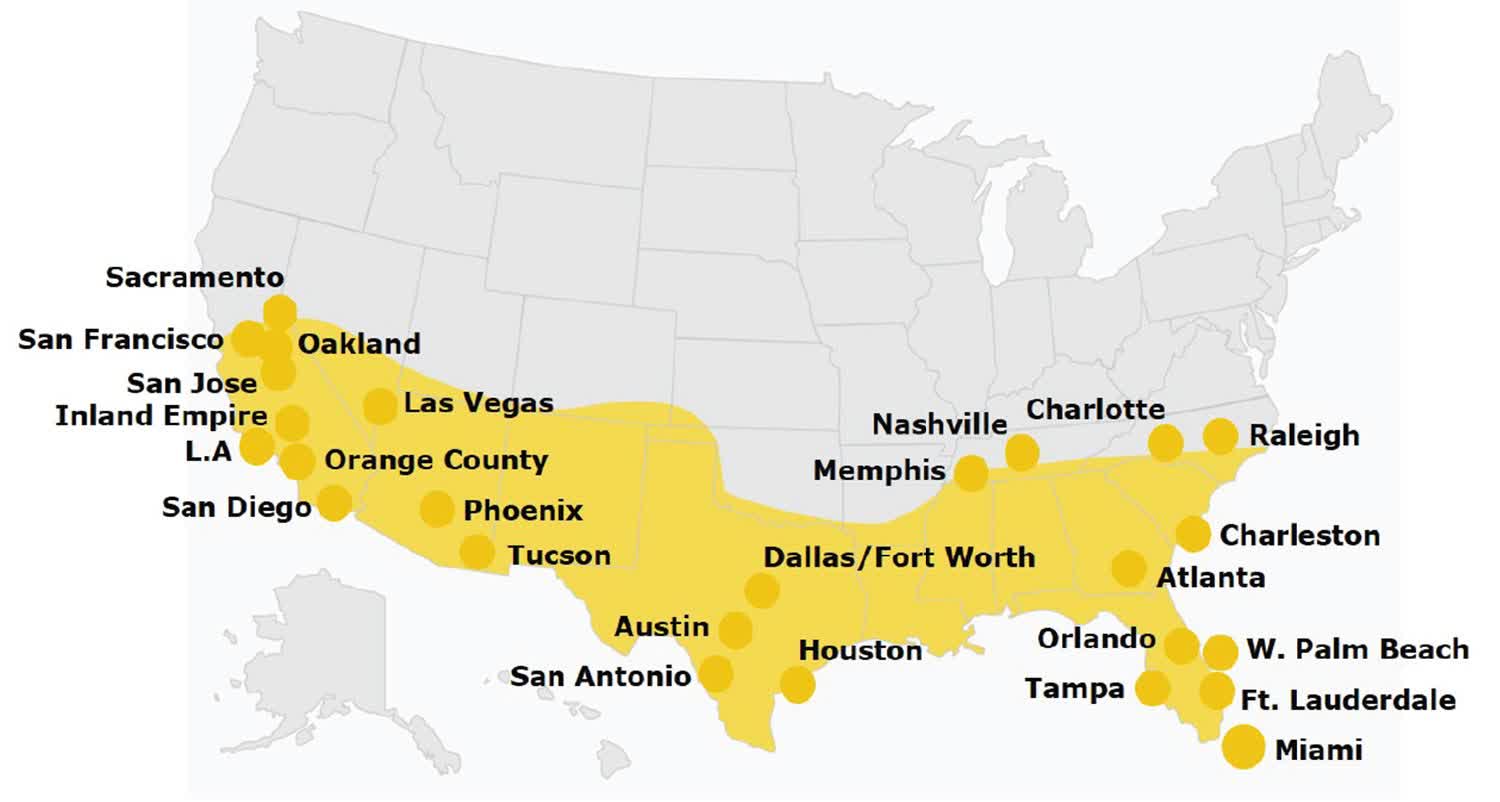

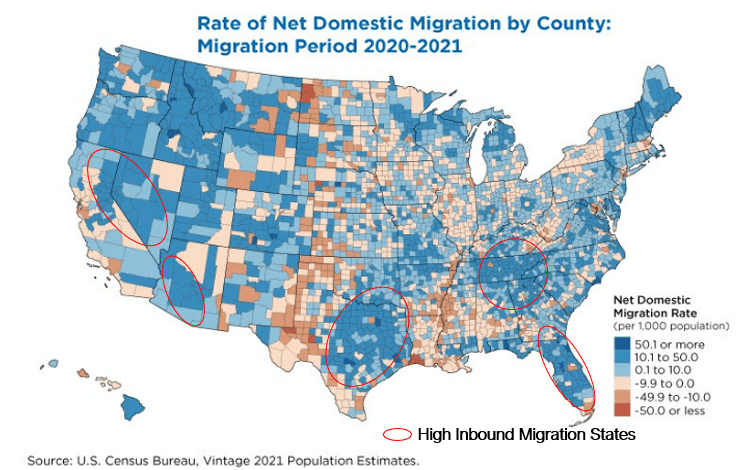

Domestic Migration Trends Favor Sun Belt States

Besides favorable international migration trends that could provide a boost to U.S demographics as a whole, domestic/interstate migration (U.S citizens moving between states) trends further suggest that Sun Belt states are likely to absorb the lion’s share of migrants. Over the years, domestic migration trends have persistently favored the Sun Belt states, which stretch across the Southeast to Southwest regions of the country (see map).

Moody’s Analytics, Clarion Partners

U.S Census Bureau

The reasons Sun Belt states are popular for international and domestic migrants include warmer climate conditions, lower taxes, and better job opportunities. California attracts many technology companies and high-skilled migrants, while Texas is a leading aerospace hub with industries that support local military institutions.

Robust fundamentals supported by healthy working-class population growth will help to boost demand for residential real estate, giving Sun Belt states a clear advantage over other regions. However, housing supply in these areas has failed to keep up with demand.

Housing Supply Gap Could Take Years To Close

Anecdotal evidence from some of the largest home builders in the U.S suggests that the persistent housing shortage in the U.S. is mainly caused by a lack of construction workers and supply-side disruptions that have led to raw material and equipment shortages.

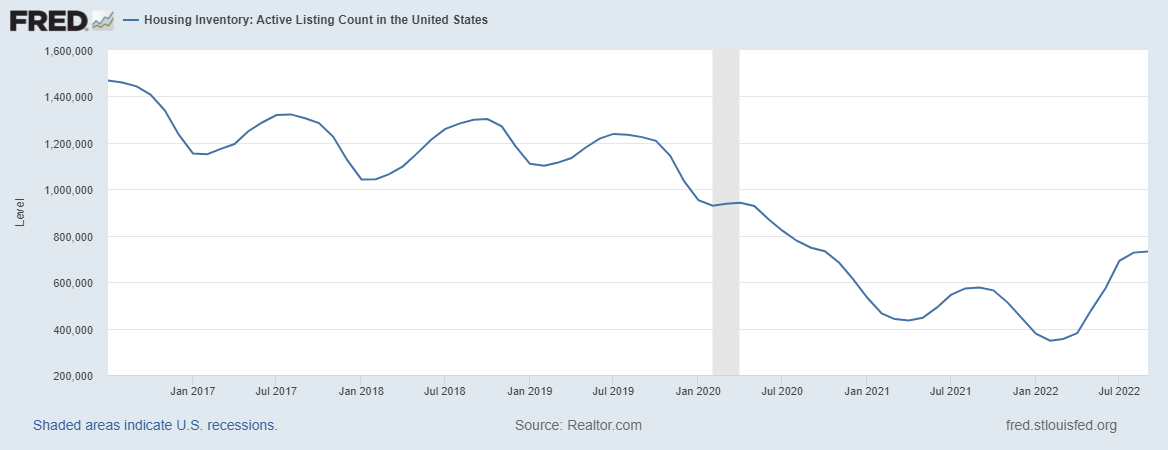

As the chart below shows, active online listings of houses for sale (widely referred to as a proxy for existing housing inventory) have drifted lower over the decade. Although sharp increases in real estate prices in 2021 and higher mortgage rates in recent months have led to a temporary increase in listings, we believe that the U.S housing supply shortage may require several years to return to equilibrium.

Realtor.com, FRED

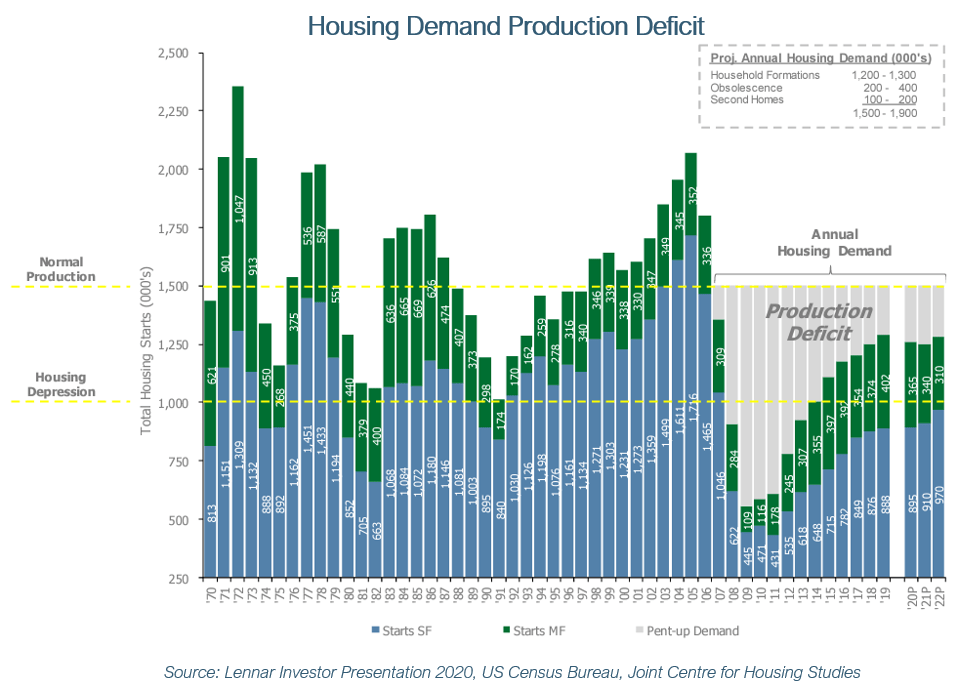

The current shortfall of new housing was created by a protracted period of under-building in the years following the subprime mortgage crisis and the collapse of the housing bubble in 2008. During this period, new household formation and the usual obsolescence of older housing stock combined were persistently higher than new housing starts for both single-family and multi-family housing. This production deficit meant that housing inventories were steadily drawn down as prices climbed.

Lennar Corporation Investor Presentation

Given our view that demand for housing will likely increase further on the back of improving demographics in the U.S, housing construction will need to pick up substantially to close the demand-supply gap. Even if we are wrong on housing demand, the real estate market will still require a substantial increase in new housing construction to restore inventories back to normal levels.

This severe dislocation of demand and supply presents a compelling risk-to-reward opportunity for homebuilder stocks: there is further upside potential for earnings as builders work through supply-side bottlenecks to increase production while home prices remain well supported by low inventory levels.

Signs of a Real Estate Bubble? Evidence Suggests Otherwise

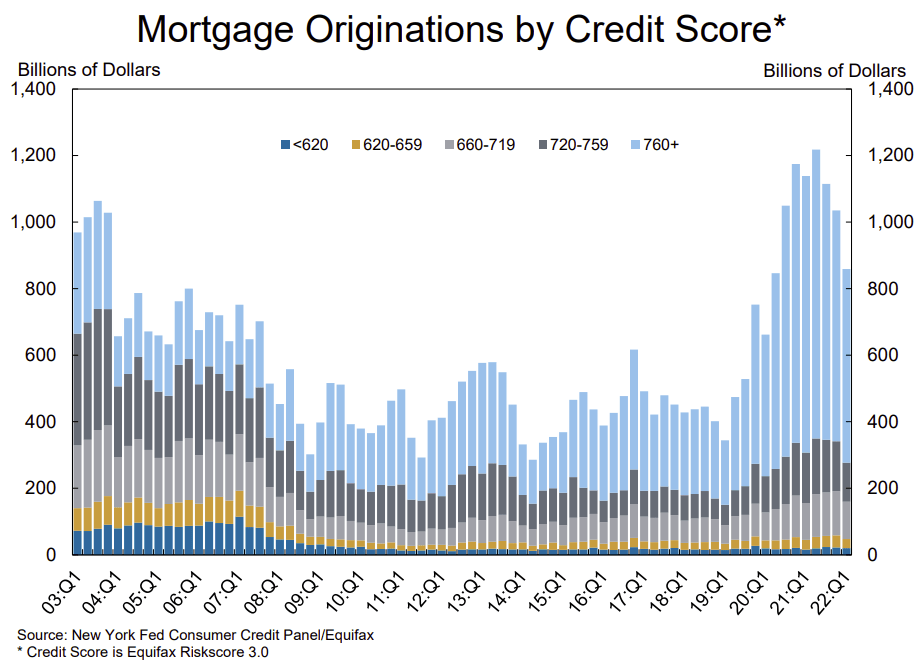

Understandably, memories of the aftermath of the subprime crisis remain fresh in the minds of investors. However, increased regulatory oversight on mortgage loans and strengthened risk management measures imposed on lenders have substantially reduced the vulnerabilities of the real estate market today. Recent data published by the Federal Reserve Bank of New York also show a substantial improvement in the credit quality of mortgage originations.

New York Fed

At the very least, evidence suggests that higher U.S. residential real estate prices are largely driven by robust economic fundamentals (strong household formation, supply shortage) rather than speculative investment activity.

D.R. Horton Shines Among Peers

Looking at the three largest homebuilders in the U.S by TTM Revenues, D.R. Horton, Inc. and Lennar Corporation (LEN) are evenly matched at US$31.1billion while PulteGroup Inc. (PHM) is significantly smaller at US$14.6 billion.

While all three homebuilders appear to be deeply undervalued at just 4.5x TTM P/E and 4.0x FWD P/E, both D.R. Horton and PulteGroup have a much higher TTM ROE of 34.9% and 30.3% respectively, versus Lennar at 20.3%. 5Y Avg ROEs reflect a similar trend.

| TTM Rev |

TTM P/E |

FWD P/E |

TTM ROE |

5Y Avg ROE | |

| DHI | US$31.1 bn | 4.42 | 4.04 | 34.9% | 21.9% |

| PHM | US$14.6 bn | 4.20 | 3.35 | 30.3% | 21.2% |

| LEN | US$31.1 bn | 4.87 | 4.52 | 20.3% | 14.8% |

The values below are extracted from Seeking Alpha.

Based on financial metrics alone, D.R. Horton appears to be the best candidate to outperform in terms of scale, valuations, as well as profitability. Next, we focus more specifically on D.R Horton’s business and highlight several advantages that further enhance the attractiveness of the company as a long-term investment.

Having The Right Target Mix

Firstly, we believe that demand for new housing will be driven by an increase in inward migration of skilled workers and new household formation among the millennial cohort (age 25-35). Thus, multi-family and low to mid-end single-family real estate are likely to see the most demand given the low-to-middle income profile of these demographic groups.

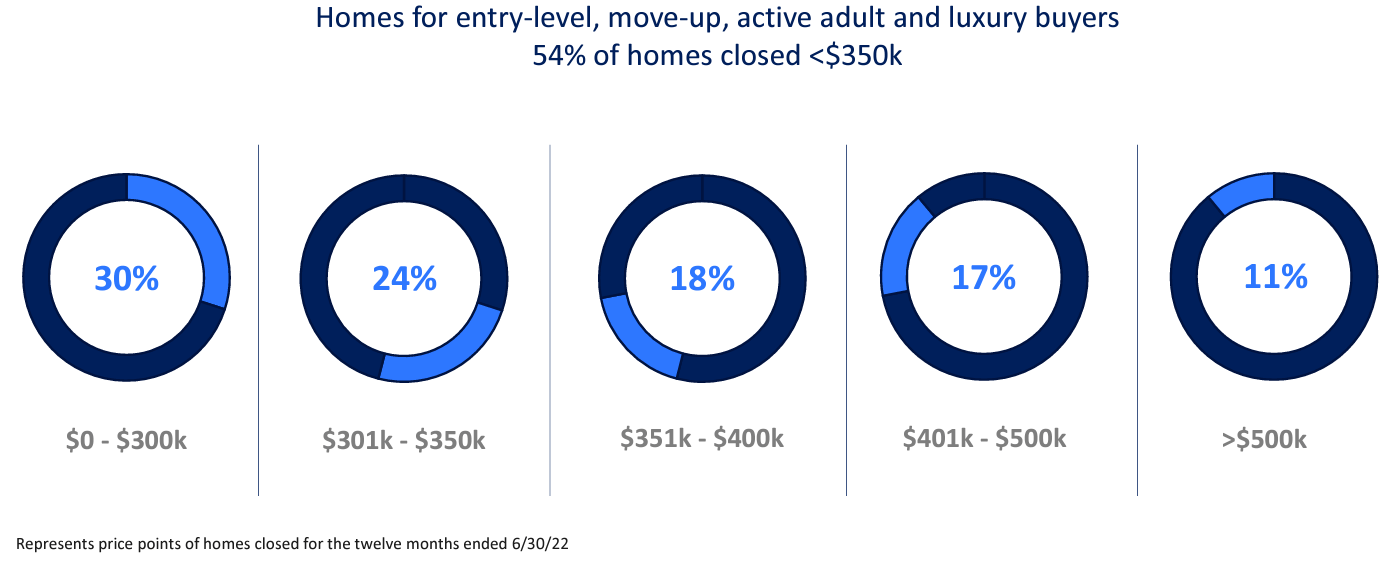

D.R Horton’s target market is ideal for capturing this group of entry-level home buyers. According to the company’s latest Q3 2022 investor presentation, 30% of the homes closed under its brands in the last 12 months were priced under US$300K and 72% were priced under US$400k.

D.R. Horton Inc

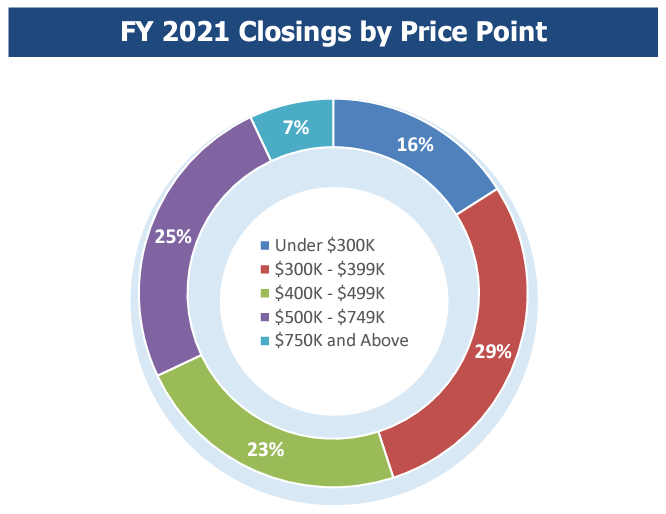

For comparison, PulteGroup’s Q2 2022 investor presentation showed that the company had a significantly larger concentration of homes closed in the higher-end and luxury segments in 2021. Only 16% were priced under 300K and 45% were priced under US$400K.

PulteGroup Inc

Although we do not think that PulteGroup’s higher concentration of sales in the higher-end and luxury segments of the housing market is necessarily a deal breaker, we view D.R. Horton as having a much better fit with our macro thesis.

In The Right Place At The Right Time

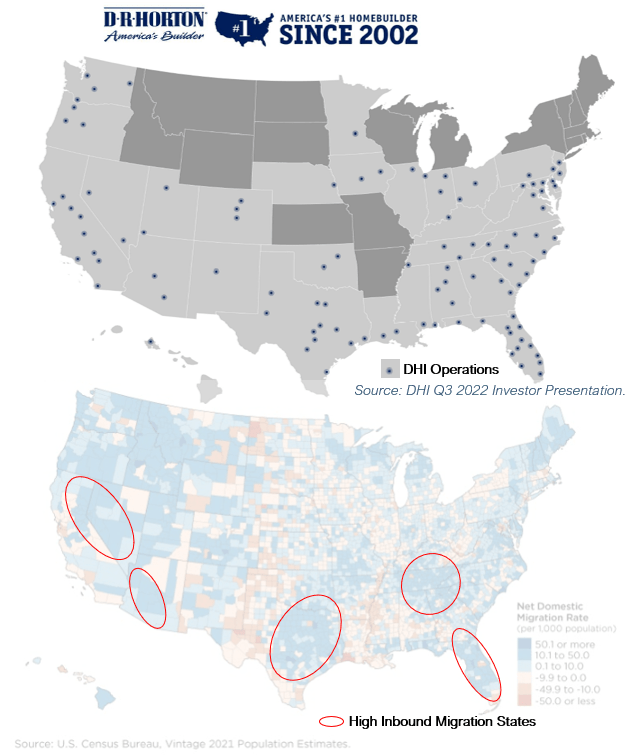

Below, we have reproduced a map highlighting the concentration of net domestic migration in Sun Belt states which we shared earlier in the article, and placed it alongside a map showing D.R. Horton’s area of operations across the U.S.

D.R. Horton Inc, U.S Census Bureau

Here, we can see that D.R. Horton’s operations are strategically concentrated in US states that enjoy healthy demand for new housing, in particular the Sun Belt states which we have previously identified as having a clear advantage over other regions.

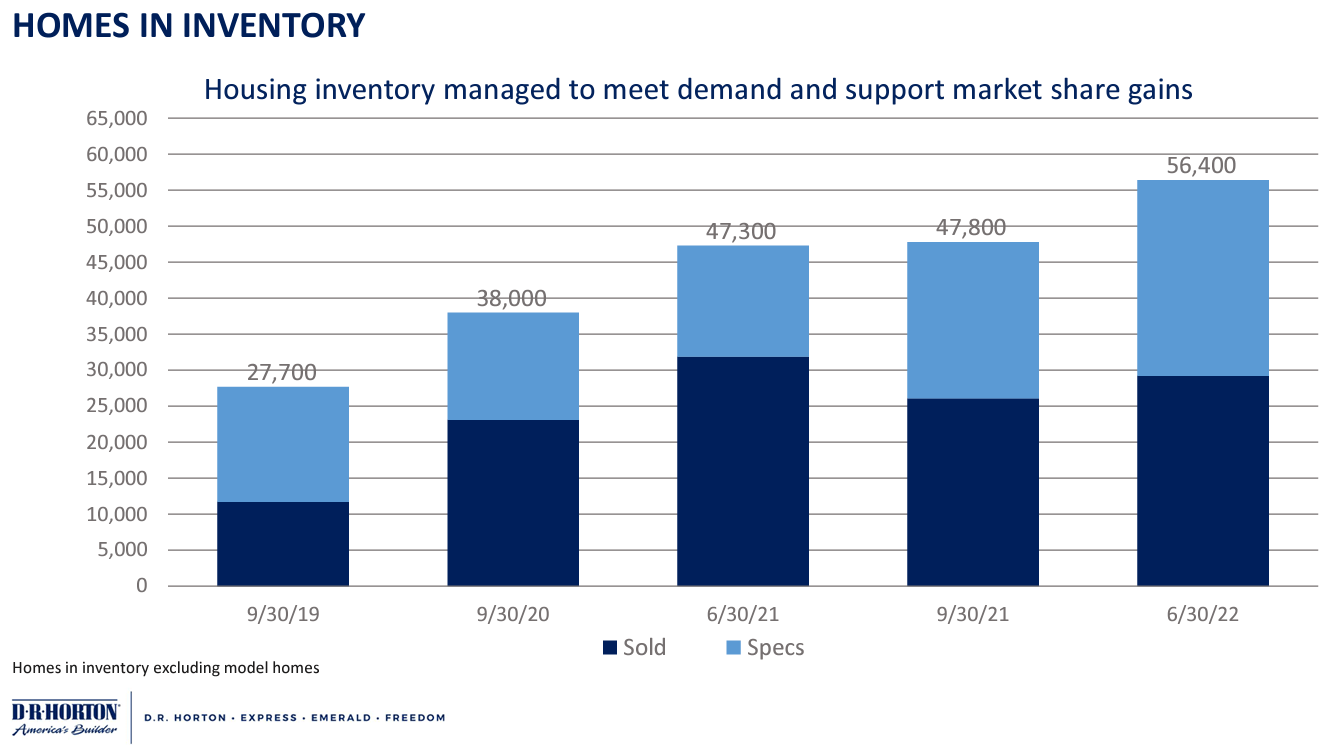

Healthy Inventory Of Unsold Homes A Strategic Advantage For DHI

D.R. Horton Inc

Another advantage that D.R. Horton has over PulteGroup lies in the former’s strategy of maintaining a healthy stock of unsold housing inventory, also commonly referred to as “spec” homes. These are newly constructed and move-in-ready homes that are built before a buyer commits to a purchase.

In contrast, PulteGroup pursues an asset-light strategy whereby the construction of new homes usually starts after a purchase has been finalized. This would rely on purchasing an option to build on a plot, which tends to be more costly but allows for greater customization of the design of the home. According to PulteGroup’s Q2 2022 investor presentation, the company has a unit backlog of 19,176 homes, with a long-term target of having 65% to 70% of new lots for construction to be held via options.

In an environment of rising real estate prices, D.R. Horton enjoys the advantage of reaping immediate gains arising from any price appreciation over the construction phase of the project. Maintaining a healthy stock of move-in ready homes also provides the benefit of being able to quickly draw on inventories when prices are favorable. This strategy of holding unsold housing inventory works very well with economies of scale. As such, we believe that D.R. Horton is in a better position to increase sales and boost earnings as conditions in the housing market begin to improve.

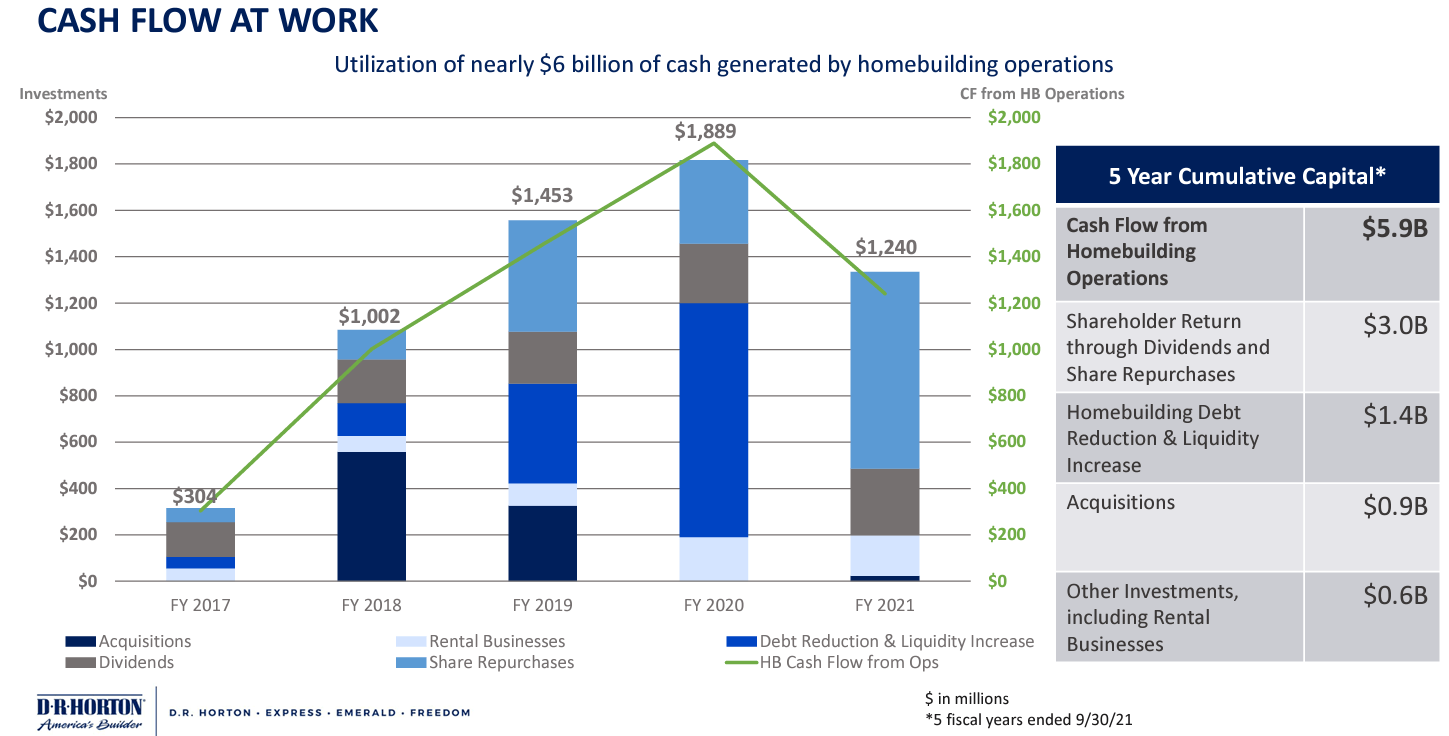

Scope For Expansion Of Share Repurchases

Finally, we see scope for D.R. Horton to further expand its share repurchase program given that the stock price is trading at compelling valuations while cash flows have remained resilient on the back of strong sales (Net Sales Orders and Homes Closed increased 8% and 18% year-on-year, respectively in Q3 FY22).

D.R. Horton

D.R. Horton has substantially expanded its share repurchase program in recent years to take advantage of the company’s undervalued share price. These share repurchases have a direct positive impact by increasing the company’s ROE. But more importantly, share repurchases signal confidence by management to reinvest in the company when shares are deeply undervalued. Thus, at current valuations, further expansion of the company’s share repurchase program should be celebrated by shareholders. D.R. Horton is a “Strong Buy.”

Be the first to comment