SimonSkafar

The Investment Plan

Cross Timbers Royalty Trust (NYSE:CRT) was created back in 1991 as a means of investing into properties where they receive a royalty of the net interests. They collect and distribute monthly net profits to the unitholders. They essentially own oil producing properties in Texas and Oklahoma. They have very favorable agreements where they are able to collect 90% of the net profits from XTO Energy which operates on these properties. On top of this they hold investment in drilling projects where they can collect a 75% net interest.

If you believe that oil prices will remain high and that we are far from adopting renewable energy completely, then I think Cross Timbers offers a good place to store money right now. They will most likely continue seeing higher net interests which directly benefit shareholders. I think the trust is a buy right now, and any drop in share price is just another opportunity to add more in my view.

Latest Earnings Report Highlights

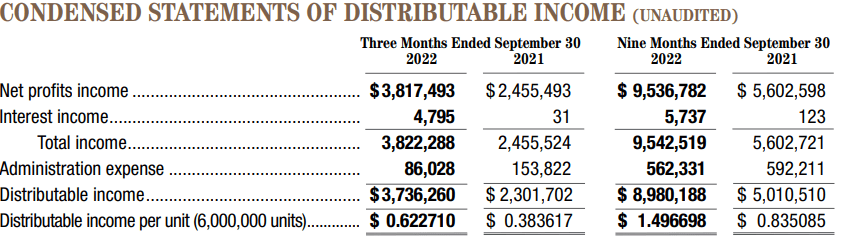

In the latest earnings report for Q3 Cross Timbers managed to impress inventors and grew revenues by 55%. The net interest income was at $3.8 million, compared to last year’s performance of $2.4 million. Since the company gets a cut of all the profits that companies regenerate on their sites, the large increase in net interest income can be attributed to higher commodity prices. Since oil prices have seen rallies and drops during 2022, there has been a lot of volatility.

Net Income Statement (Q3 Earnings Report)

Looking at the bottom line, the EPS came in at $0.62, an increase of 63% YoY. As the company has barely any operating expenses, except for administration expenses, an investment into the company is getting you directly in touch with the profits of the properties.

As the company operates as a trust for investors, they did not provide any comments on the future performance. But if you are a believer in that commodity prices will continue to increase for years to come, then net interest incomes should continue increasing. I think it will take time until we see a clear down trend in the use of oil all over the world. Until then, CRT will most likely continue seeing improvements in my opinion.

Sector Outlook

The interests that Cross Timbers generate comes directly from the current commodity prices of oil. Therefore some volatility should be expected as demand and supply obviously shifts back and forth. In 2022 they saw record numbers as oil prices spiked because of the ongoing war in Ukraine. But the prices remained elevated throughout most of the year. Looking ahead, the short-term will most likely also bring volatility. But with good timing and management they should be able to take advantage of this and end up on top.

Market Outlook (Deloitte)

In the long-term renewable energy will be the clear winner. But I think that is many years out. This has been misinterpreted and caused a lot of oil companies to have their valuations suppressed. But as people realize oil is still going to be with us for a long time, the multiples should start moving upwards. In the meantime investors will be able to collect healthy dividends as these companies generate impressive cash flows. During the drops in oil prices in 2020, a lot of companies took advantage of this and focused on keeping costs down and with the boom in 2022 a lot of debts could be paid off. This primed the sector for somewhat smooth sailing ahead.

Competition

Seeing as Cross Timbers operates as a trust where they collect the interests and profits from their facilities, the only real competitors would be if they are looking to expand. Otherwise they are subject to commodity prices for revenues, just like all their competitors. But some notable options that investors might be looking at instead would be VOC Energy Trust (VOC), Battalion Oil Corporation (BATL) and Epsilon Energy Ltd. (EPSN).

Looking at the way these companies are growing, I think EPSN has them beat with the highest revenue growth of them all. Looking at the dividend these companies are offering, I think that investors would definitely go with Cross Timbers, I know I would. Offering an 8% dividend they are in a healthy position to offer value to shareholders. As the competitors all look for expansion, Cross Timbers can sit steady and collect their royalty. In the long-term I think this will prove much more stable. If the competitors make a misstep and invest too much and oil prices plummet, then that could cut deeply into the bottom line, creating rich and dangerous valuations.

The Balance Sheet

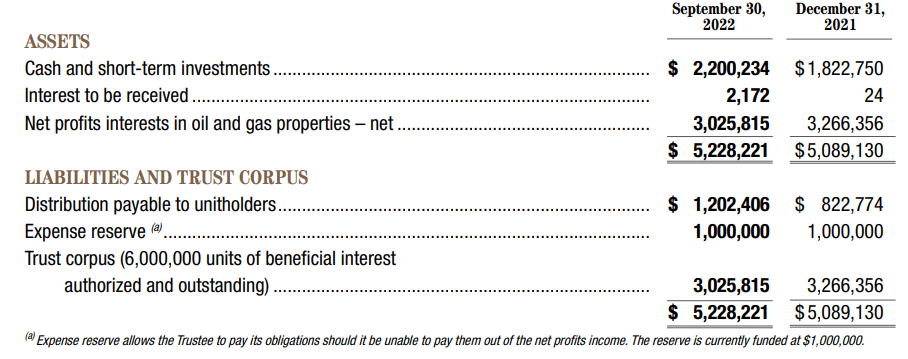

In terms of looking at a trust and their balance sheet there’s not much information, instead much of the research is about the properties they hold and the potential for them.

Cross Timbers Balance Sheet (Q3 Earnings Report)

But with Cross Timber I am still seeing them increase their assets YoY as they become increasingly more valuable and profitable. Right now the company holds $2.2 million in cash, an improvement of 22% YoY. This is great as when the profits might not meet expectations, they are still able to deliver a healthy dividend to shareholders.

The liabilities are staying the same as the shareholders essentially are a liability too for the company on the balance sheet. They account for the distributions payable to shareholders as a liability, and the same with their expense reserves.

Outstanding Shares (Seeking Alpha)

Share dilution will probably not be a thing as the trust is not here to raise capital and further their expansion. Instead, an investment into it is directly benefiting from the profits that the facilities are generating. A bet on oil companies continuing to print money.

Valuing The Company

It’s hard putting a price tag on the share price for a trust. These are mostly places where people place money to be stored away for a very long time. But I do think that there is merit to having at least an idea of what the possible value could be for the company.

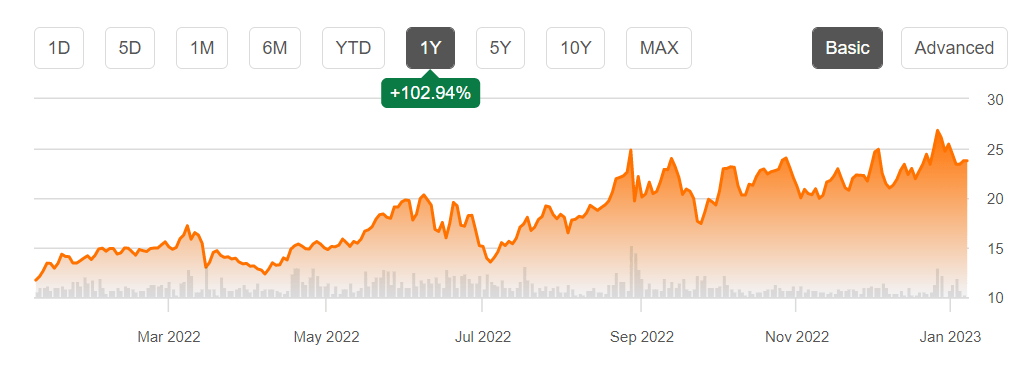

Price Chart (Seeking Alpha)

In the case of Cross Timbers they have seen a share price increase of over 100% in the last 12 months. Seeing some profit taking wouldn’t be too surprising in my opinion. They offer an 8% dividend yield right now which is one of the main attractions for me. But the value will come from whether or not commodity prices for oil will remain high and provide investors with plenty of profits.

I think that in the short-term there might be some volatility which could make for unpredictable returns. But if you are an investor at these prices I think just holding on to your shares and collecting the dividend should pay off very well. Like I said, seeing lower prices as investors take profits isn’t unreasonable and that could provide a very good opportunity to add some more to a long-term hold. If I see prices below a p/e of 10 I would be very interested in adding more. That would mean a share price of around $17-18.

Conclusion

In the last few years Cross Timbers has seen a large increase in their net interests as oil prices have spiked and also remained high. This directly benefits the shareholders as the trusts collect 90% of the profits from some of the facilities.

The oil and natural gas industry will continue seeing demand in my opinion as the shift to renewables is slow and costly. In the meantime there will be a lot of money available for these companies to make.

I think that investing into Cross Timbers at these levels is worth it for a long-term hold. The dividend is great and the valuation isn’t too rich either in my view.

Be the first to comment