Michael Derrer Fuchs

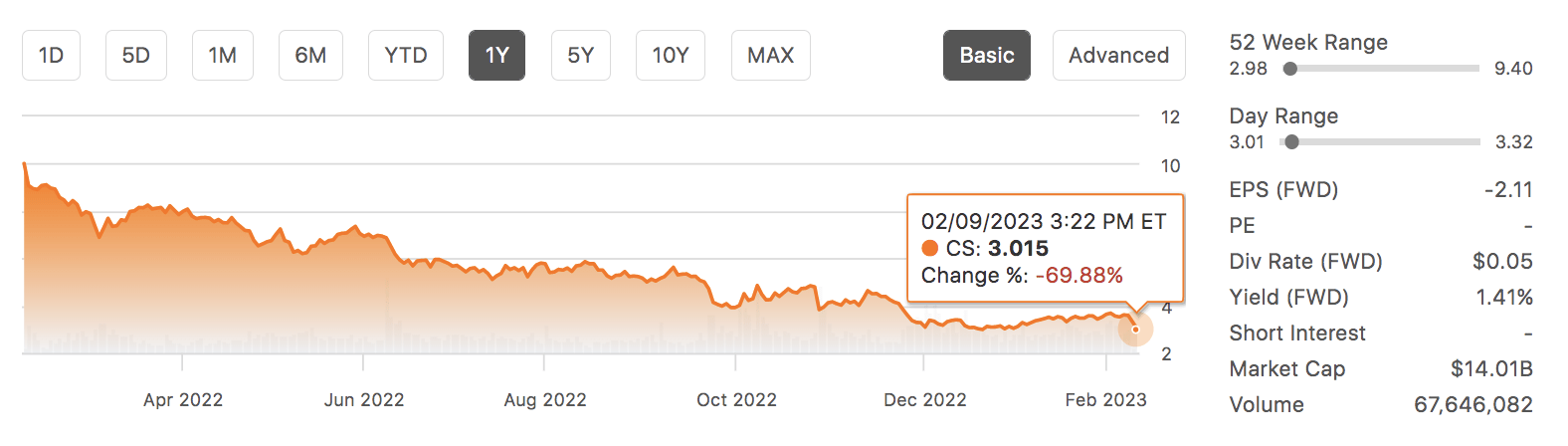

And there we have it, folks; Credit Suisse Group AG’s (NYSE:CS) stock is essentially a distressed asset. After a nearly 70% year-over-year drawdown, Credit Suisse is in the midst of a seemingly endless spiral.

Today’s article isn’t as much about price discovery as it is to update the firm’s investors on the ins and outs of the firm’s restructuring process and what they mean for Credit Suisse’s investors.

Without further ado, let’s get into it.

CS Stock Price (Seeking Alpha)

Noteworthy News Update

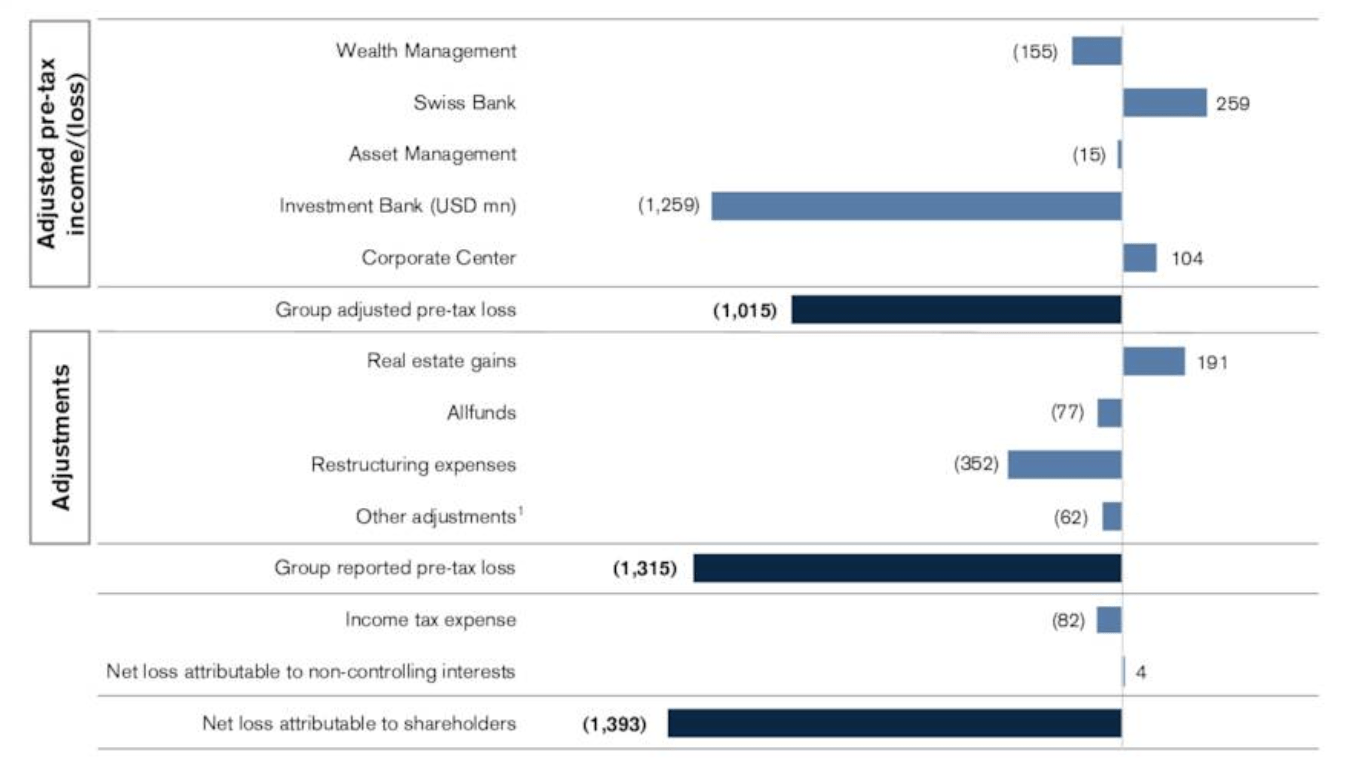

Adding to the plethora of recent bad news, Credit Suisse released its Q4 earnings report on Thursday, revealing a $1.5 billion staggering miss on bottom-line earnings. The firm’s Q4 earnings miss is its worst since the 2007/08 housing crisis, sending investors into a tizzy.

According to Credit Suisse’s management, the bank experienced significant obstacles pertaining to restructuring. For example, the company’s asset management division rendered outflows of more than $1.1 billion, and its general restructuring charges continued to mount.

However, an analysis beyond headline news is required to determine Credit Suisse’s fate.

Operational Review

Let’s start by looking at a few developments in the bank’s restructuring process and how they have and could affect the organization’s income statement.

As mentioned on numerous occasions by the bank’s management, it wants to pivot into a lean model, emphasizing its Swiss banking segment’s lending position and wealth management capabilities.

During the past quarter, the bank incurred $352 million in restructuring expenses as it unwound approximately $35 billion in securitized products and deleveraged a significant portion of its risk-weighted assets. Credit Suisse also completed the acquisition of M. Klein & Company for $175 million to strengthen the appeal of its CS First Boston investment advisory business.

For those unaware, Credit Suisse plans to carve out the advisory part of its investment banking unit and fund it with external capital. As such, the Klein acquisition has tremendous appeal as it adds deal flow and intellectual capital.

Now back to the topic of restructuring costs. From a minority investor’s vantage point, it will depend on your horizon whether you consider the costs core or non-core. Usually, restructuring charges will be considered non-core and phased back into earnings. However, the Credit Suisse restructuring program is expected to be lengthy; meaning charges could be recurring for a prolonged period.

On the other side of the pendulum, we think the $191 million in gains from real estate can be phased out of core earnings as a non-recurring item.

Credit Suisse

Let’s move on to our outlook on the firm’s profit and loss statement.

Net revenues slipped broadly. However, astonishingly, the bank’s asset management division’s revenue slipped by 28% year-over-year, coupled with a 10% slump in segment outflows. Although the financial markets have acted unfavorably of late, this clearly signals structural issues. The firm’s asset management division could continue to struggle unless it slashes its entry fee rates significantly, which is highly dangerous in today’s market, which is overshadowed by low volumes.

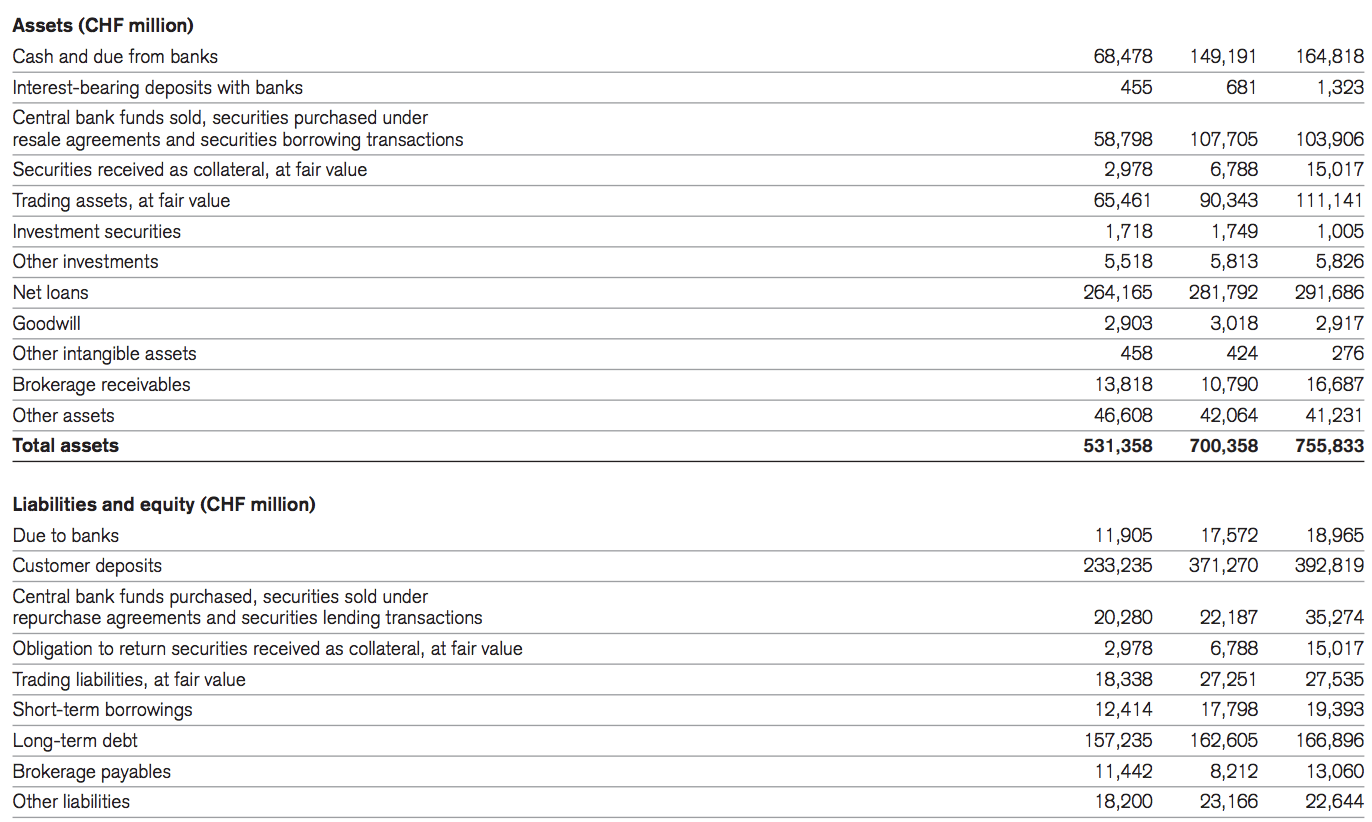

Furthermore, Credit Suisse’s total year-over-year net interest income slid by 8%, which is quite shocking as most banks benefitted from elevated interest rates during the past quarter. Prospectively, we can’t see Credit Suisse making up ground here as it possesses significant maturity mismatches after an $88 billion firm-wide outflow in deposits. Managing fixed-income assets and liability term structures will be difficult because Credit Suisse lacks an adequate capital hierarchy.

Balance Sheet Displaying Maturity Mismatch (Credit Suisse)

A P&L final feature to outline is the bank’s investment banking unit. It’s difficult to place judgment on the bank’s investment banking division. Sure, the firm’s investment banking segment experienced a 73% year-over-year slump in Q4. However, the IBD market was unfavorable to most companies, and as mentioned before, Credit Suisse is in a rampant transitional period with its investment banking advisory unit. Therefore, we’ll stay neutral here.

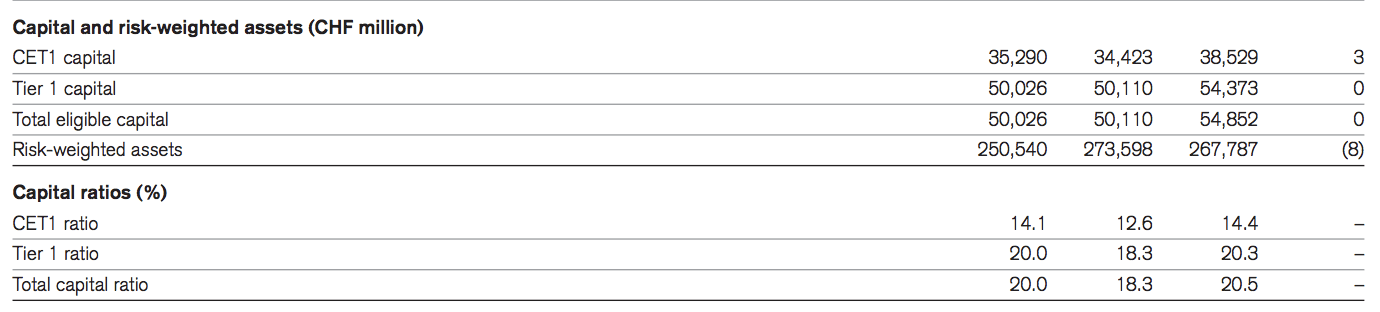

Lastly, a look at risk suggests that Credit Suisse is still in safe territory regarding risk-weighted capital with a CET1 ratio of 14.1%, a significant improvement from last quarter’s 12.6%. However, one has to wonder whether the bank can organically sustain its capital adequacy with the high volume of capital outflows it is experiencing.

RWA (Credit Suisse)

Valuation and Dividends

Credit Suisse has a tangible book value per share of 10.60, which is approximately 3.50 times higher than its current stock price. However, with continued restructurings and diminishing liquid capital, the bank could raise various rounds of equity and debt capital, subsequently diluting its shareholders.

Furthermore, Credit Suisse’s earnings per share is in negative territory at -0.46, indicating that receding residual value is en route.

Credit Suisse

The company’s management is awaiting board approval for its dividend proposal. In any case, Credit Suisse has a lumpy history of dividend payments. Therefore we don’t want to speculate on the bank’s future dividend distributions.

Final Word

Although the urge is there to speculate on a Credit Suisse recovery, it simply won’t be morally correct placing a buy rating on an asset without a valid premise.

Credit Suisse’s restructuring will likely result in sustained non-core costs, continued negative EPS numbers, and depleted book value. Moreover, it is near impossible to speculate on its investment banking unit’s outcome due to the velocity of the variables involved.

The entity’s asset management and interest-bearing activities are worrisome amid an evident lack of client satisfaction and a balance sheet maturity mismatch.

Although positives exist, the situation is still too opaque to provide a definitive outlook on Credit Suisse Group AG and its stock. As such, we are placing the security on our hold list.

Be the first to comment