Torsten Asmus/iStock via Getty Images

In my last macro article, I wrote about how the analysts were way too high with their S&P 500 earnings forecasts and their S&P 500 target price. The market continues to move lower and the consensus analyst target price for the S&P 500 is still just over 5,000. This continues to be a ridiculous number and shows just how far the analyst community is behind the curve.

I spent several years as an independent research analyst, and it was usually more common than not to watch many of the analysts at the really big Wall Street firms downgrade stocks after they had already gone down over 50% or upgrade stocks after they just went up 50%. They’re even more lethargic with their market target prices.

During my 23 years as a professional money manager, I witnessed the year 2000-2002 eighty percent “dot.com” bubble sell-off in the Nasdaq and the 50% S&P 500 sell-off in 2008-2009 during the Financial Crisis. If you think that Wall Street analysts are going to get you out of the market before the major damage is done, think again.

At the end of the day, each individual investor is ultimately responsible for his or her own portfolio(s). I disagree with both perma-bulls and perma-bears. The economy does not always expand, and markets do not always go up.

You cannot miss out on the great 13-year run that the market had from 2009 to 2022, but you cannot have your offense on the field 100% of the time unless you are rather young and have the time to make up for big losses.

After the Nasdaq hit about 5,300 in March of 2000, it went down almost 80% over the next 18-24 months. It took the Nasdaq more than 12 years to get back to 5,000 once again. Most retirees were heavily weighted in the tech sector at that time and their portfolios never came back.

Having a defense can come in handy at certain times, but most investors do not have one. Most only know how to sell everything and go to cash, when in reality alpha can be easier to create on the downside than the upside.

During 2020, the COVID year, alpha was there to be had as the so-called “spec-tech” and “work from home” stocks roared. Our Ultra-Growth portfolio was up 66.9% that year while the S&P 500 was up just 16.3%. Our large-cap, Premier Growth portfolio was up 38.2% against the 16.3% return of the S&P 500. These are two of the six portfolios that are in our Best Stocks Now Premium service.

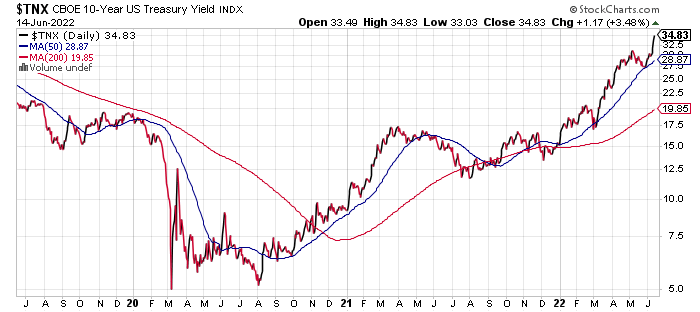

Last year 2021 was a transition year as the 12-year long bull started to wind down as the interest rates started to finally head up. Interest rates on the 10-year U.S. treasury actually bottomed in July of 2020 at 0.53%. They came down from a high of 15.84% in September of 1981. A 40-year cycle of falling interest rates was finally over.

In January of this year, I wrote about the impact that rising interest rates would have on stocks (especially ones with high PE ratios) and bonds. The longer duration the stock or bond, the bigger the hit it would take.

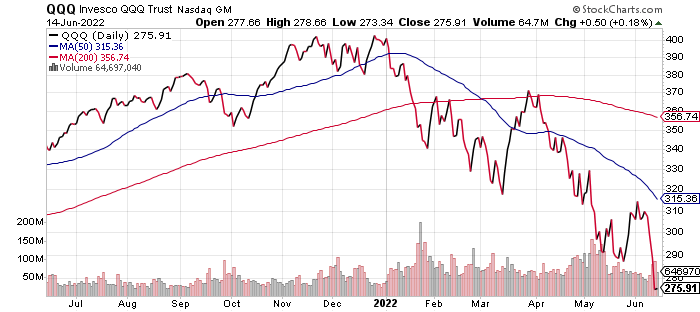

The DJIA is now down 17.1% from its Jan. 4 of this year all-time high. The S&P 500 is now down 22.2% from its high, while the Nasdaq is down 32.7%. Notice how the Nasdaq is down the most. That’s because it generally is made up of higher PE and longer-duration stocks than the DJIA. We will talk about the Inverse ETFs, PSQ, QID, and SQQQ later on in this article.

Now for the real carnage: Cathie Wood’s ARKK ETF is now down 77% from its February 2021 all-time high of $159.70! It closed at $36.99 on Tuesday of this week. The downfall of the ARK family of funds began when interest rates began to break out in February of 2021. That was the warning sign to flee stocks like Teladoc (TDOC), Upwork (UPWK), Roku (ROKU), Zoom (ZM), Peloton (PTON), etc., etc., etc.

Stockcharts.com

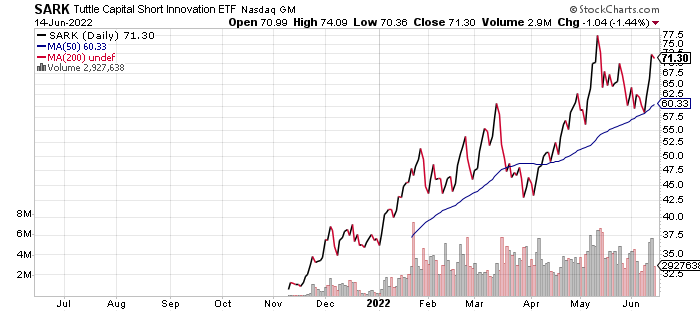

In our Jan. 11, 2022 article, “The Real Reason That ARKK Continues To Sink” we outlined the relationship between interest rates and multiples (PE ratios) and long-duration stocks vs. short-duration stocks. Then we followed up three days later on the Inverse ARKK ETF, SARK. SARK has soared since then while ARKK as continued to get pummeled.

Stockcharts.com

Can you start to see the opportunity for some extreme alpha in a down market? Obviously, picking on some of the most vulnerable areas of the market can be quite profitable during a downtrend in an individual stock, sector, or index. When ARKK goes down 50% and SARK goes up 50%, how much alpha is created?

Now the malaise in the market that began in February of 2021 has slowly worked its way throughout the entire market. It has been buoyed by excessive valuations, extreme inflation, a hawkish Fed, and technical breakdowns of charts throughout almost every neighborhood of the market.

As I wrote in my February 2022 article, rising interest rates are the kiss of death for long-duration high PE ratio, high price to sales ratio, or no PE or no price to sales stocks. Multiples contract viciously in a rising interest rate environment. Consider that forward PE ratios of the S&P 500 has contracted from 23X to almost 16X so far this year.

Earnings expectations have budged very little during this heavy sell-off, the multiple has gone on an extreme diet and lost several inches off its waistline, however. Long-duration bonds have also been whacked real good during this rise in rates. There’s a good time to own bond funds and a bad time to own bond funds. This is a horrible time to own bond funds!

There also are good times to own equities and bad times to own equities. Except for fertilizer and energy stocks, this is also a bad time to own almost all equities. With stocks and bonds off the current menu, what’s left?

I was lucky enough to learn about inverse funds back in 2002 when a wholesaler from Profunds visited my RIA office. I started using them in managing variable annuities at first, then began expanding them to my fee-based money management practice.

There also has been a great expansion in the choices that I have today as a professional money manager vs. what was available back then. They have also grown in size and become much more liquid.

I currently own 12 different inverse ETFs amongst the six different portfolios that I manage. I continue to pick on the most vulnerable areas of a market that has almost zero catalysts to look forward to.

These ETFs should continue to do well in a down market that has the Fed on the warpath, out-of-control inflation, and earnings that have now peaked after a 12-year growth cycle.

In addition to this, rapidly rising interest rates are now bringing the red-hot real estate market to a screeching halt. Consider that a 30-year fixed mortgage is now pegged at 6.26%.

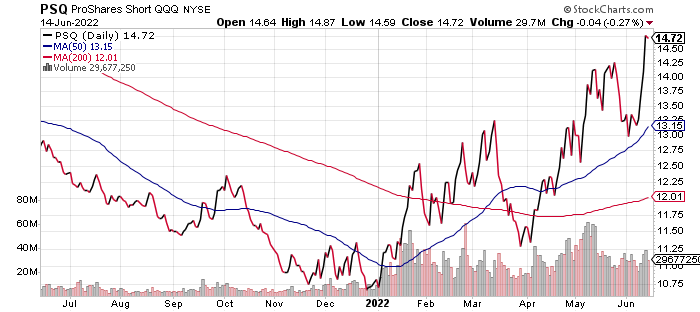

The inverse funds on the Nasdaq should continue to do well. PSQ is the 1X inverse version, QID is the 2X model, and SQQQ is the 3X version. The chart of PSQ looks a whole lot better than the chart of the Nasdaq right now.

Stockcharts.com Stockcharts.com

PSQ is one of the ETFs that we own right now.

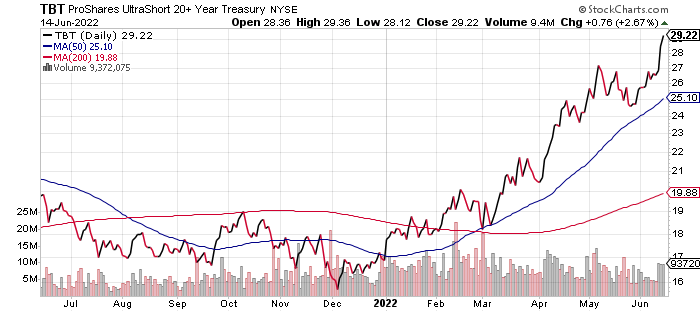

It would seem to me that interest rates are all set to go a lot higher. Maybe we will see 5% on the 10-year sometime next year. The inverse long bond ETF TBT should also continue to do well.

Stockcharts.com

TBT is also one of the inverse ETFs that we currently hold.

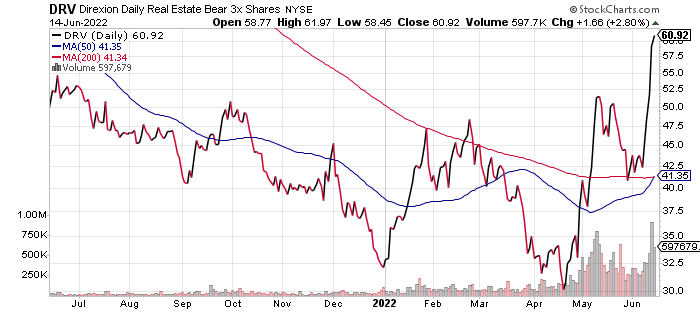

My last example of an area to pick on (there are many more) would be real estate. The perma-bulls on REITs are wrong again. The REIT index RWR went down over 70% during the 2008-2009 financial crisis and recession. REITs do not always go up. I think that the ETF DRV will continue to do well in this nasty environment that we are now in.

Stockcharts.com

If nothing else, you can use it as a hedge against a REIT portfolio.

As you can see there is another asset class out there. It’s called inverse ETFs. They can create some very good alpha for those seeking it. In fact, more alpha can be created in a down market than in an up market.

Obviously, this current run in inverse ETFs will not last forever, but I believe it still has a long way to go. It now appears that we are in a global recession after a thirteen-year bull market.

Perma-bull anyone?

Be the first to comment