benedek

The Toronto-Dominion Bank (NYSE:TD) is acquiring Cowen Inc. (NASDAQ:COWN) for $39 in cash per share. Cowen trades at $38.59. This is a practical example of picking up pennies in front of the proverbial steamroller, but sometimes that’s something I like to do. TD is a $118 billion market cap Canadian juggernaut of a bank. Cowen is a specialized U.S. investment bank with a market cap of around $1 billion.

The deal spread indicates there is a 1.06% upside to the deal close. First announced on August 2, 2022, the deal is supposed to close in Q1 2023. The options chains for Cowen show almost no outstanding open interest post-January. That means the market puts a high likelihood of the deal being closed well ahead of February’s expiry. The company pays a quarterly $0.12 dividend. Last year, the record date was in early March. If the merger drags on, that will mitigate some of the pain as the upside increases to 1.37% (assuming no tax).

There is a theme to some of the mergers I’m writing up lately. Because the market has been recovering off its lows, their downsides do not appear as menacing as they once were. Many deals that are currently ongoing were struck at relatively advantageous prices. At least based on recent history, I’m not sure 2023 will be so great. One example is the Microsoft (MSFT) and Activision Blizzard (ATVI) deal.

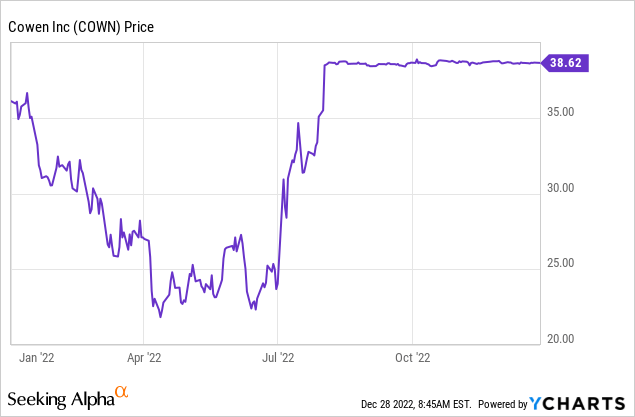

It is hard to say what the exact downside would be with the Cowen deal. Looking at the chart, you get the impression that rumors about a deal spread in July, and the market (rightfully) bought into it.

It may be too dark to put the downside in the $20 – $25 range, but that looks more like an unaffected price level than the ~$35 it traded at once the deal was officially announced.

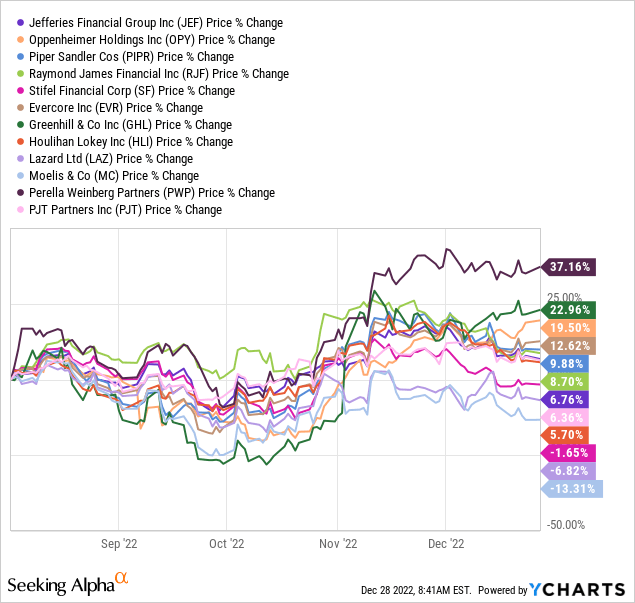

I pulled up the price developments for the peer group from the merger documents, and this paints a highly favorable picture:

The average price appreciation comes to ~8.8%. Cowen appreciated by 0.42% over the same time frame. This leads me to believe the downside is more likely to be at least in the $22 – $27 range, which may still be too dark. All bets are off as the market resumes a selloff, however. This translates into a downside risk range of -30.03% to -42.9%.

There is a high likelihood this deal closes, as Cowen is a tiny U.S. institution and TD Bank Group is a huge Canadian player. It seems likely to me that the deal has closed before the end of February but possibly before the end of January. The upside of around 1% isn’t that juicy. But I view this as a “lower risk” deal that’s highly likely to close as planned. In addition, the shareholder vote has passed, and sometimes mergers close soon after that. If it closes in the first weeks of January (which is not impossible), the annualized return is great.

Be the first to comment