imaginima

We see mixed signals in the European chemical industry. BASF (OTCQX:BFFAF) reaffirmed its 2022 guidance, Solvay increased its 2022 forecast, whereas Covestro (OTCPK:CVVTF, OTCPK:COVTY) significantly lowered its profit forecasts for the year after gas prices are continuing to rise and there is an ongoing uncertain about the supply situation with regard to Russian NatGas development. We suggest having a look also at our recent publications of Uniper and Engie.

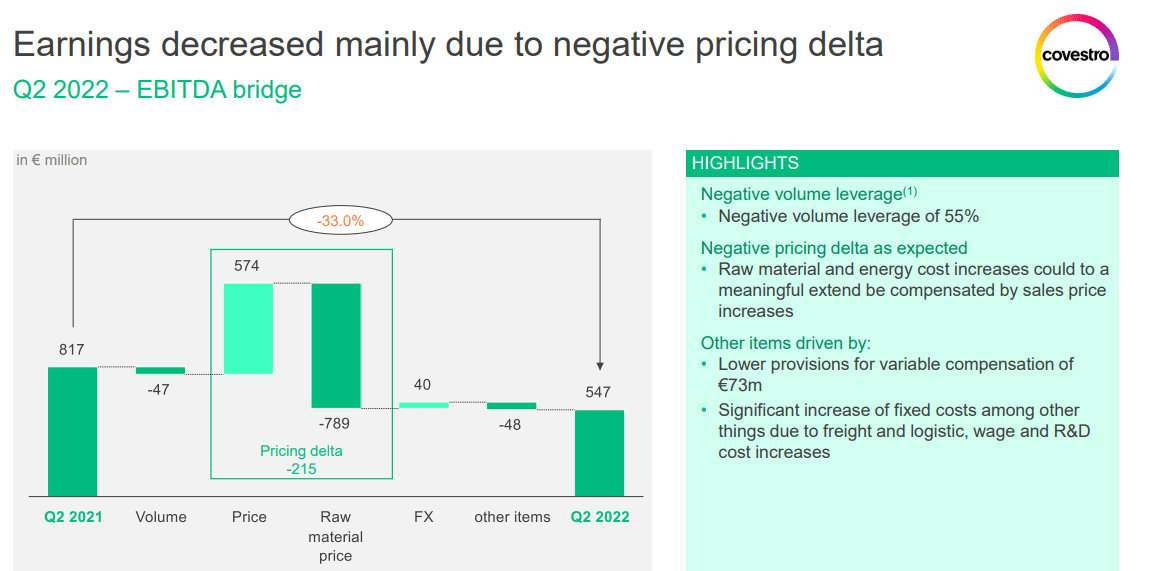

Two days ago, the Leverkusen-based group presented the three-month numbers. With a turnover of more than €4.7 billion, the company delivered an 18.88% increase compared to the same quarter last year, in which €3.96 billion had been achieved. The increase in top-line sales is only attributed to an increase in sales prices, i.e., volumes were 2% down in a year-on-year comparison (Chinese lockdown negatively contributed to the Q2 volume performance). Nevertheless, rising gas prices due to the Ukraine-Russia crisis are leading to margin deteriorations. The company was not able to fully pass through higher energy costs. Thus, there was a negative pricing delta as we can see in the snap below.

Covestro EBITDA evolution (Covestro Q2 results)

As a result, the group’s net income halved to almost €199 million in the second quarter. The company management justifies the decline with high burdens in the supply chains and high energy costs. Natural gas is also a key element as a raw material input.

Looking at the divisional level, we see that margins in the Specialty and Solutions segment were more resilient than in the Performance Materials division. From a volume perspective, we are forecasting a rebound in sales in China post lockdowns.

Gas emergency plan

Despite the fact that the company managed to beat analysts’ consensus estimates in sales and EPS, there is an increasing concern about gas rationing. Thus, Covestro presented a crisis plan with an outlook for the following quarter.

- If the gas supply situation continues to deteriorate, the company would have to close individual production sites;

- The company is converting steam generation to oil where possible. However, as already mentioned, natural gas is a much more remarkable input for production;

- A quarter of Covestro’s production is located in its home country, and Germany is facing the worst gas disruption across the EU. Other production sites are safer.

- As the company stated: “based on a scenario with ~25% reduction of gas supply to the German plants would have an estimated low to mid-double-digit € million EBITDA impact per month“.

Conclusion and valuation

The company lowered its 2022 EBITDA guidance and now expects a range between €1.7 to €2.2 billion. Our previous target price was derived based on a €2.5 billion EBITDA and a 5.5x EV/EBITDA multiple. Looking at the net debt evolution (that increased for working capital requirements and seasonality due to the dividend payment), we reduce our expectation of Covestro’s EBITDA to €2 billion. Applying the same multiple, we derive a price target of €40 per share. The German chemical player is currently trading at a discount if compared to its closest peers and its historical average by 40% and 27%, respectively. Covestro is very cheap, and there is no credit on its return to mid-cycle earnings.

Asset replacement cost analysis, a juicy dividend yield, and an ongoing buyback are also our margins of safety. We lower and confirm our buy rating.

Covestro guidance (Covestro Q2 results)

Be the first to comment