MoMo Productions/DigitalVision via Getty Images

Introduction

Cosmos Health Inc.(NASDAQ:COSM) is at first glance a pharmaceutical distribution company that also owns some pharmacies and has interests in various other health related businesses.

Looking deeper, the primary financial driver of Cosmos is “nutraceuticals”, which as the name implies, are products somewhere between medicine and nutrition and herbal remedies. You can see examples from their SPL brand.

While these types of products are becoming more popular, they are not exactly the same as science backed, proprietary, unique medications that real pharma companies like Amgen and Pfizer sell.

Cosmos has been expanding the sale of these products both online and at retail in the US and Canadian markets.

Despite this, Cosmos is still in a stage in its lifecycle where it is producing very little revenue, is unprofitable, and has been issuing large amounts of equity and debt to finance its operations and acquisitions.

Recent Results

In Q3 2022, revenue came to $12 million vs $13.5m in Q3 2021. Operating income and gross profit both fell as well. The company contributes the decline solely to currency movements, with revenue actually growing 7.5% in local currencies.

So even though the economies that the company operates in are starting to weaken, this level of growth is a disappointing in my book for a company that is supposed to be and needs to be rapidly growing.

Q3 2022 release

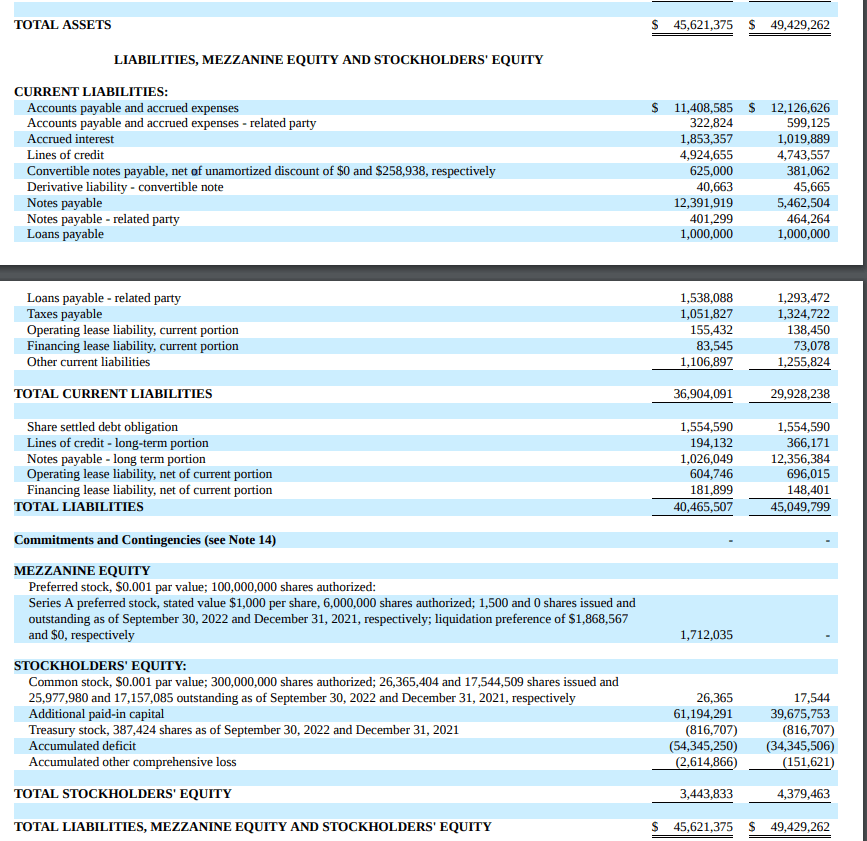

The balance sheet is also weak. The company has large current liabilities it has to meet and will continue to need more financing to do so. The accumulated deficit of $55+ million shows that the company has had many an unprofitable quarter as every net loss eventually ends up accumulating there.

This is why the company needs stronger growth than it is currently producing. Financing is much easier when you have a compelling story to tell and the results to back it up.

The company also has half their assets, ~$25 million, in receivables. With payables of around ~$12 million, they could improve their collection speed greatly.

2021 Annual Report

Red Flags and Concerns

Diving into Cosmos’s filings, there are a lot of things that give me pause and that I do not like to see. Firstly, the company has material weaknesses in their internal controls over financial reporting.

While this may sound like accounting jargon, and it somewhat is, it is a serious red flag when it is present.

Specifically, Cosmos has a lack of separation of duties and a lack of review and oversight across multiple levels.

2021 Annual Report

An example of segregation of duties at the most basic level might be the fact that someone who makes a journal entry to update the general ledger, the accounting system of record, is also the one reviewing and approving it. Or there is no review or approval at all.

These two duties are supposed to be separate people both for internal controls and well as to make sure junk is not being posted that needs to be fixed or reversed later.

Other disclosures include a “going concern” disclosure. This is present when the rules dictate that the company meets certain thresholds that they might be at risk of not meeting their obligations in the next year. In simpler terms, Cosmo needs to raise more debt and equity in the next year.

Moving on, the company also has a number of concerning related party transactions. The company’s CEO, Grigorios Siokas, has personally loaned the company millions and also personally guaranteed other loans that were from third parties.

Other weird stuff includes a very small 40,000 euro loan to a former director of which they have only paid off 5000 euro so far. That just seems pointless in relation to the size of the company, even though its micro-cap.

In general, the company’s capital structure is very complex and a mess, frankly. They have warrants, derivative liabilities, all sorts of debt with various structures, convertible debt, and just immediately makes me want to steer clear. What this capital structure tells me is that the company has had to get very creative to finance its operations and acquisitions, that is not a good thing.

Capital Raises and Other Events

Cosmos has raised equity 2-3 times this year and also performed a 1 for 25 reverse stock split to remain in compliance with Nasdaq minimum price rules. Even with their dire financial condition shown above, the company continues to make acquisitions. This year they acquired a telemedicine company, ZipDoctor, and vertically integrated with Cana Labs, among other smaller acquisitions.

The rationality for these moves is that Cosmos is attempting to become a globally diverse health company, or something like that. Unfortunately, I just don’t think that is a smart idea or that Cosmos has the runway or resources to make it anywhere close to that grandiose vision.

Conclusion

As an outside, minority investor with no power or control, you want a company that is simple to understand, has a focused and proven business model, manages their capital well, and has consistent and growing profitability.

Cosmos has none of those things. My view is that the company is an unfocused, deeply indebted, mess of a holding company that might have one or two core businesses that are decent but cannot carry the company toward its vision.

I believe Cosmos needs to refocus and streamline its ambitions. Even so, its current actual operating business is one I am not a big fan of as it appears to be bordering on snake oil and has little competitive advantages in terms of patents, branding, or anything else. Their greatest asset is some exclusive distribution of some products in Greece and other places but that is about it.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment