Morsa Images/DigitalVision via Getty Images

Investment Thesis

ContextLogic (NASDAQ:WISH) has made the airwaves after Citron’s recent tweet. Given the strength of Citron’s following, I believe that I have to now upgrade my rating on WISH to a hold.

Author’s rating on WISH

Previously, I had a sell rating on the stock. But now, with the stock at $1 at the time of writing, I believe it could make sense to revisit this analysis, at this much lower price point.

And what you’ll find now is that from this entry point, the risk-reward is more compelling, but I’m still not entirely sold on this opportunity.

I believe that WISH has approximately 2 years left of cash on its balance sheet. Put another way, I suspect that a capital raise will be on the cards. Imminently.

ContextLogic is Not Pinduoduo

Pinduoduo (PDD) is the Chinese e-commerce giant. Citron makes the assertion that Pinduoduo and ContextLogic have similar opportunities. Personally, I disagree.

I know Pinduoduo quite well having been bullish on the company for a long time.

Author’s rating on PDD

The goal of ContextLogic’s approach is to provide consumers with an accessible and enjoyable online shopping experience. ContextLogic is said to be able to use its data insights to propel a consumer’s discovery-based buying experience.

However, beyond this narrative, I’ve not found the facts echo that point of view.

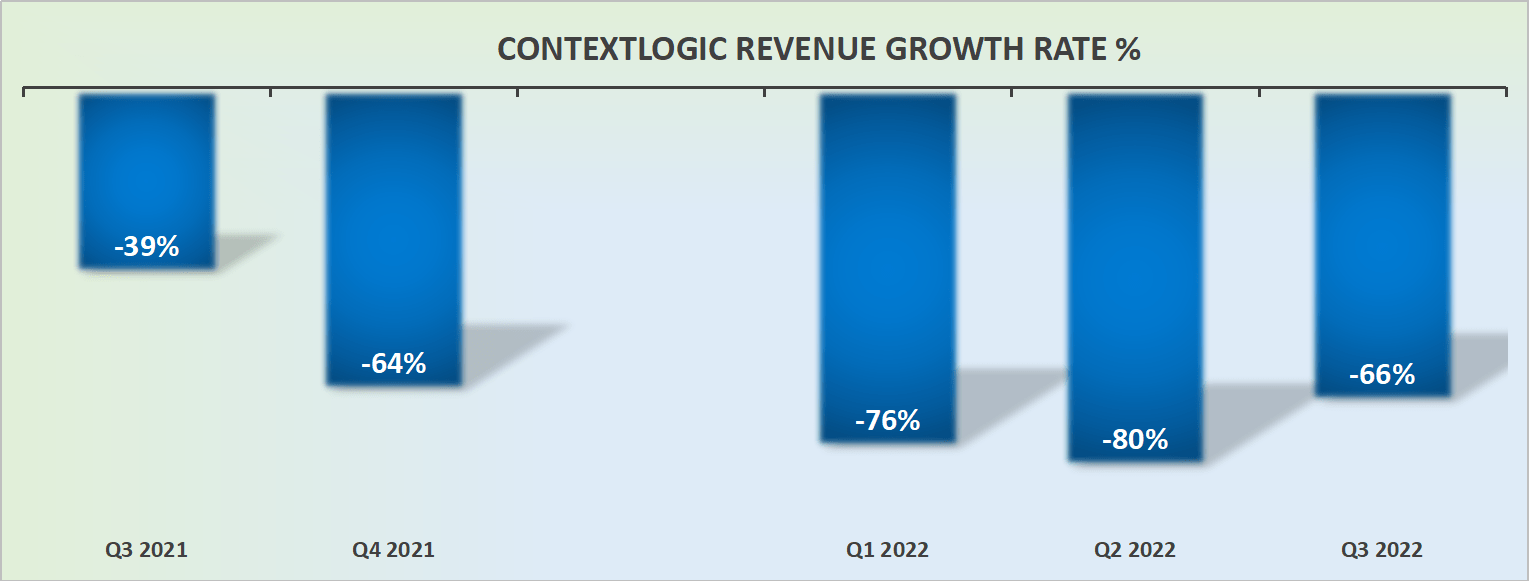

Revenue Growth Rates Don’t Inspire Much Hope

WISH revenue growth rates

As you can see from the graphic above, WISH’s revenue growth rates appear to be moving in the wrong direction. As an investor, I find it difficult to back companies that are shrinking with time.

The business could survive, but in this case, time appears to be working against the investor, not with the investor.

But to be clear, it’s not all bad.

Balance Sheet is the Crown Jewel

WISH’s balance sheet holds approximately $800 million of cash and equivalents. What’s more, the business operates debt free.

Indeed, perhaps a better way to think about this investment is that it trades for less than the cash on its balance sheet.

On yet the other hand, WISH is burning through a fair amount of free cash flow each quarter. As a point of reference, Q3 2022 saw WISH burn through $100 million of cash.

WISH Stock Valuation – Cheap Can Always Get Cheaper

The only way one can make the claim that WISH is cheap is to only focus on its balance sheet. Assuming the business was to wrap up its operations right now and return the capital to shareholders.

However, that’s not a likely scenario. A more realistic scenario is that WISH will attempt to stem its cash burn and stabilize its business.

In fact, by my estimates, WISH has approximately another 2 years’ worth of cash on its balance sheet. Regardless, it’s unlikely that WISH will wait until the very last moment to raise capital.

Consequently, on the back of this run-up on its share price, I would not be surprised to see WISH diluting shareholders in the very near term. I don’t believe that WISH will be able to dilute shareholders prior to its Q4 results. But if the lessons from Bed Bath & Beyond (BBBY) are to provide any help, it is not to wait around too long. WISH should consider diluting shareholders quickly, into a raising share price, to provide the least overhang to the share price.

The Bottom Line

Shareholders will undoubtedly welcome Citron putting a spotlight on how cheap WISH is. However, I struggle to see how in this most challenging macro environment WISH will be able to stabilize its operations.

Indeed, what we’ve seen from companies’ guidance for the present period is that even its strongest e-commerce peers are struggling to gain traction. How will WISH manage where others are failing?

Particularly given that even when the economy was stronger and market conditions more favorable, WISH was already back then struggling to grow its operations.

One thing we can be clear about, WISH’s interim CEO Joe Yan will have his work cut out on the company’s upcoming earnings call next week.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment