courtneyk/E+ via Getty Images

The sharp rally we’ve seen in January so far has told us one thing: investors are tired of being bearish, especially over the same news. The pace of interest rate increases seems to be slowing this year, and even though we are staring down a recession, most indicators suggest it will be shallower and shorter than we might have feared.

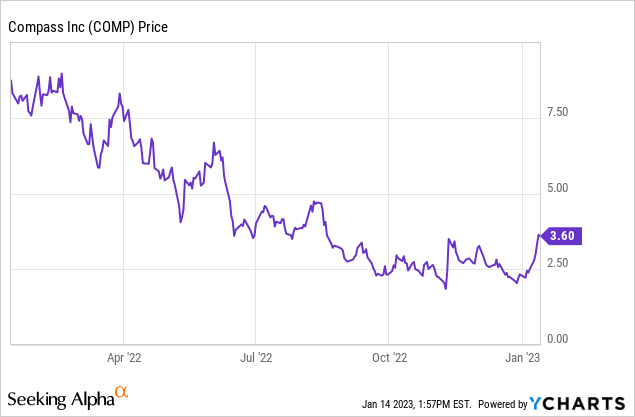

Compass (NYSE:COMP), the national real estate agency known for its presence in affluent coastal markets, has been the beneficiary of the recent rebound. The stock has rallied ~50% after touching all-time lows below $2 in November. Still, Compass is down nearly 60% over the trailing twelve months; and relative to its IPO at $14 per share, the company has lost a giant chunk of its market value. It’s a good time, in my view, for investors to survey the damage.

I’ve held on loyally to my Compass holdings (the bulk of which I entered at $4 per share), and even though the losses have been painful to watch, I remain incredibly bullish on this name. Of course we can’t ignore the perfect storm of macro headwinds pulling down the real estate sector, but we have always known that the real estate industry is cyclical and we shouldn’t blame Compass for that. In my view, the company is well-positioned to survive through the current downturn and rebound much more broadly.

The bull case for Compass; and its diminutive valuation

For investors who are newer to Compass, here is a rundown of my full bull thesis for the company:

- Within a few years, Compass has become a dominant brokerage – Compass’ market share of U.S. real estate transactions is growing rapidly to ~5%. Already deeply embedded into major coastal markets, Compass is more recently pushing into new office opportunities in the Midwest. There’s still room for further expansion. Even after the new market activity this year, Compass is still penetrated into less than half of the U.S. population.

- Tertiary revenue opportunities – Recently, Compass has been opening the door to new monetization opportunities, including starting its own title company. This positioning helps Compass derive more wallet share from real estate transactions as a whole. Compass has commented that attach rates on these tertiary services are rising. Compass estimates its U.S. TAM is $240 billion, of which only $95 billion and the rest is coming from adjacent services.

- Strong branding – Compass built a brand around being a full-service, high-quality real estate brokerage, very similar in style and profile to competitors like Berkshire Hathaway Home Services or Sotheby’s. This gives the company a very strong distinguisher against other tech-first rivals like Redfin.

- Scalable platform – Compass’ primary costs lie in the R&D spend to deliver its technology platform for Compass agents, as well as the sales and marketing costs of advertising its brand to homebuyers/sellers and potential new agents. These costs are scalable: as Compass’ scale grows, and as agent productivity grows (the average Compass agent generates 19% more sales in the second year), Compass will be able to improve its profitability margins, which we have already seen in the company’s latest results.

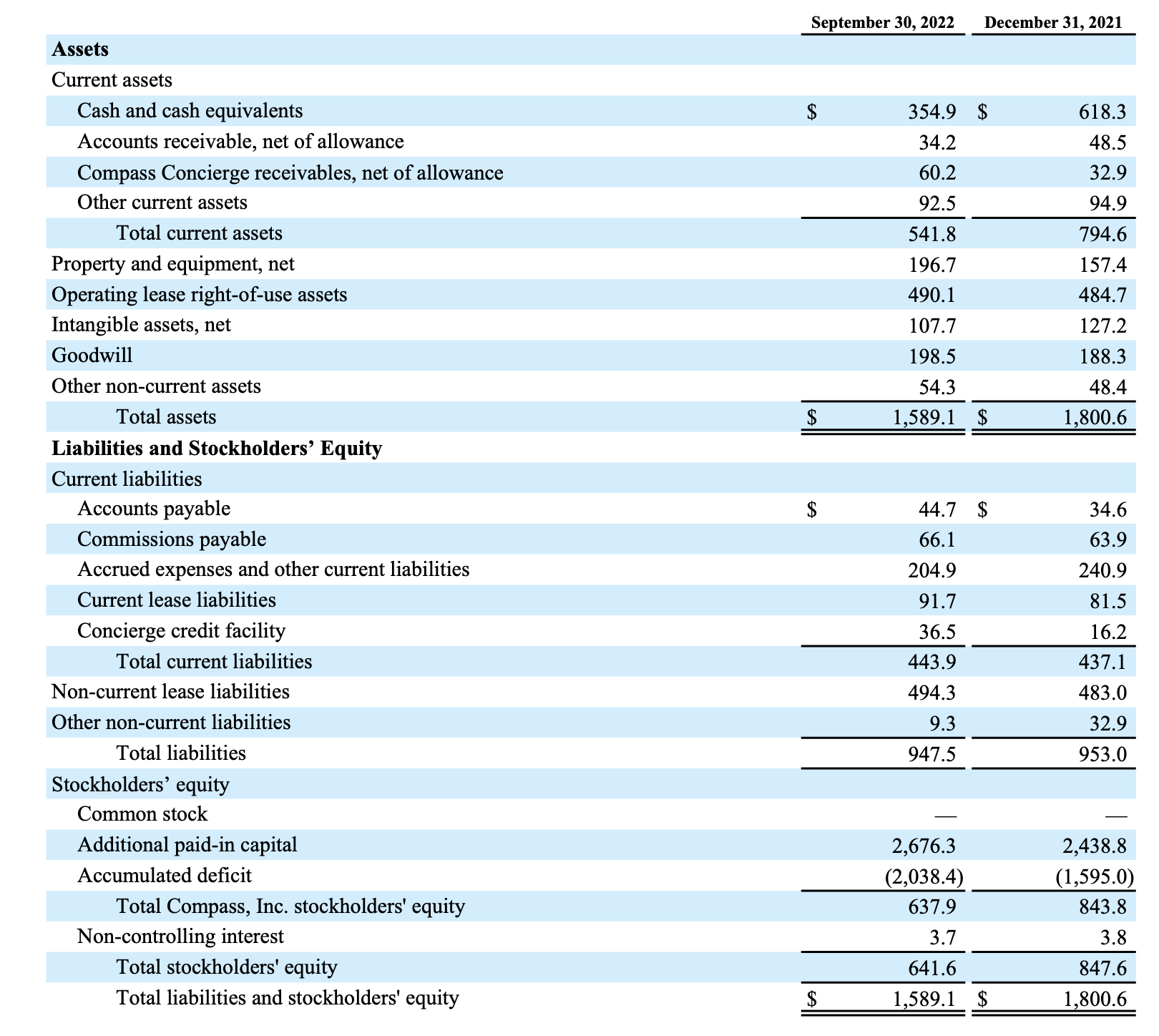

The best draw to investing in Compass, of course, is its tiny valuation. At current share prices just under $4, Compass trades at a market cap of $1.57 billion. After we net off the $354.9 million of cash and $36.5 million of debt on Compass’ most recent balance sheet, the company’s resulting enterprise value is $1.25 billion.

Now, near-term multiples aren’t going to mean much for Compass given it is currently unprofitable (it had just started to crank out positive adjusted EBITDA before the real estate recession kicked in). But do note that the company is currently at a ~$6 billion annual revenue scale with an ambition to generate 10% adjusted EBITDA margins and 8-9% FCF margins in the future.

Market share is holding

In Compass’ most recent quarter, the company reported -14% y/y revenue growth to $1.49 billion, and its guidance for Q4 ($1.15-$1.30 billion in revenue) represents a wide range of -29% y/y to -19% y/y decline. But the key thing to realize here is that this is simply the market. We note that for the same Q3 period, Redfin (RDFN) reported a -17% y/y decline in its brokerage revenue.

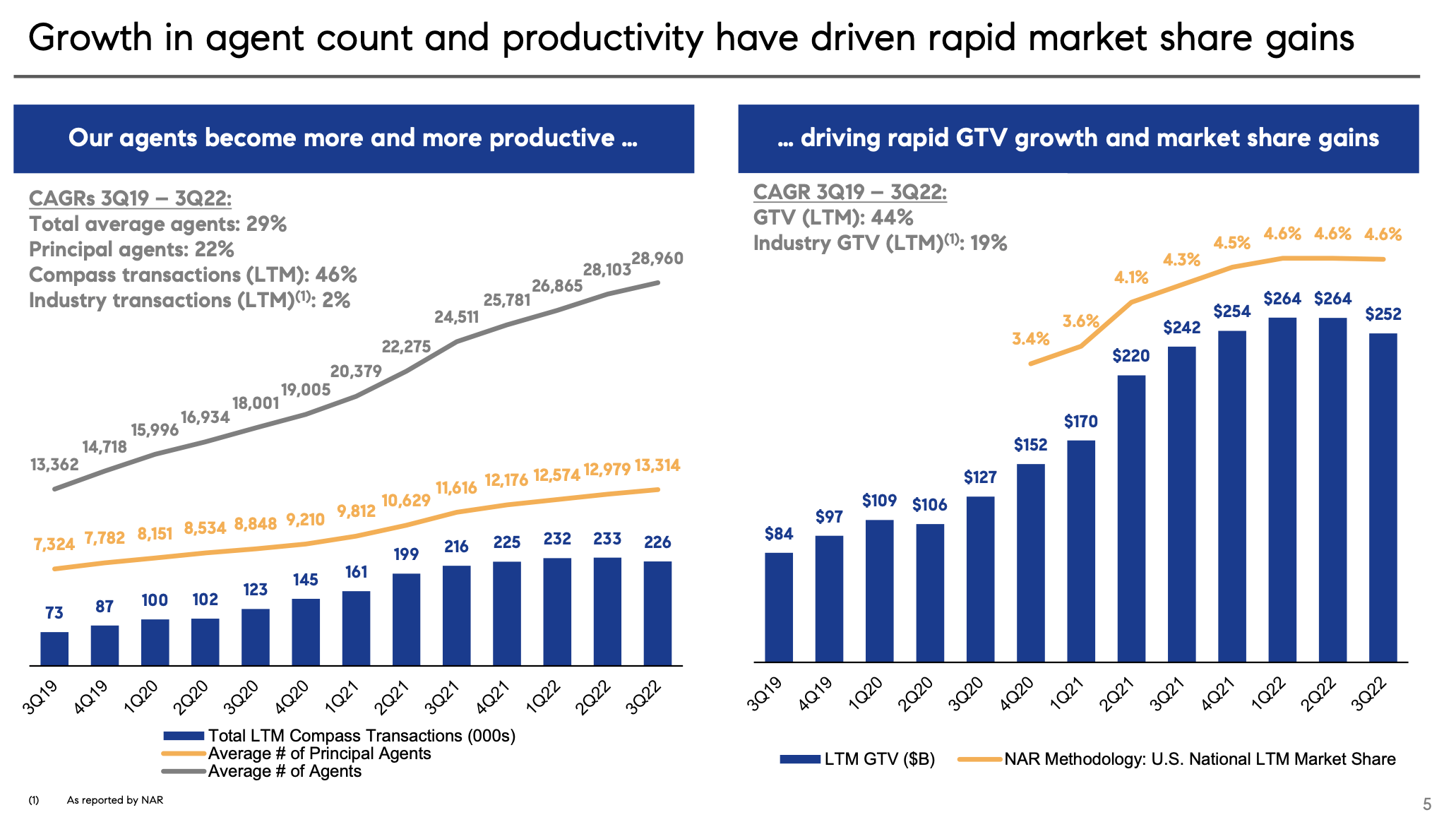

As shown in the chart below, Compass has managed to maintain a 4.6% market share despite recent headwinds. (We note as well one more comparison to Redfin, which only has a 0.8% market share, despite its market value being only roughly half of Compass’):

Compass market stats (Compass Q3 earnings presentation )

Note as well that from a pure transactions volume standpoint, Compass declined “only” -12% y/y in the third quarter, compared to -21% y/y in the U.S. residential real estate market as reported by NAR (per CFO Greg Hart’s remarks on the Q3 earnings call).

Compass is tightening its belt and planning for free cash flow positive in 2023

One other positive we should note: Compass leadership is not blind to the state of the economy and it is planning for a downturn in real estate in 2023. The company has been aggressively managing expenses and expects to be free cash flow neutral by the second quarter of 2023, with an eye to becoming free cash flow positive for the entirety of 2023.

Per CEO Robert Reffkin’s remarks on the Q3 earnings call regarding expense controls:

The past 12 months have been tough and the next 18 months fear that they can be tougher. Compass will be diligent and persistent. We’re focused on getting to the other side. Since the second quarter of this year, we have been aggressively meeting down our expenses to adapt to this rapidly deteriorating market and already achieve significant cost reductions in our technology, engineering and other operating expenses through a variety of measures, including reductions in force […]

With our heavy investment period behind us, we are operating the business more efficiently. We have achieved significant market share gains among weakening competitors. We have built an incredibly strong agent network, a highly regarded brand in the most advanced technology platform that helps us recruit agents and make them more productive. We believe that the actions we have taken to date and cost reduction initiatives currently in place put us on pace to deliver our targeted non-GAAP operating expense run rate of between $1.05 billion and $1.15 billion exiting 2022.”

Compass also has a healthy cash balance of $355 million on its most recent balance sheet, versus an expected adjusted EBITDA loss of $50-$80 million in Q4 (which should improve sequentially as cost cuts ramp).

Compass balance sheet (Compass Q3 earnings presentation )

Key takeaways

All in all, with the discipline that Compass is displaying on the opex side, plus the fact that Compass is performing better or at least on par with real estate competitors, I think the company is well-positioned to survive through a short-lived real estate downturn. Stay long here.

Be the first to comment