naphtalina/iStock via Getty Images

~ by Snehasish Chaudhuri, MBA (Finance)

Community Healthcare Trust Incorporated (NYSE:CHCT) is a small-cap healthcare real estate investment trust (REIT), which generated an annual average total return of 24.5 percent during the period 2016 and 2021. The stock not only outperformed its peers, but also the broader market. CHCT’s common equities are currently trading at $35.38, and have a market capitalization of $857.16 million. This healthcare REIT’s portfolio of properties is quite diversified and primarily falls within two broad categories – traditional medical facilities and specialty centers. Its properties have a high occupancy rate and are under long term lease agreements, extending up to 2039. CHCT pays quarterly dividends and generates a low but decent yield on a consistent basis.

CHCT’s Properties Have High Occupancy and Long-Term Lease Agreements

Community Healthcare Trust Incorporated finances, acquires, or operates outpatient healthcare services at non-urban markets. Due to its low asset base, this healthcare REIT seeks to discover off-market or lightly-marketed acquisition opportunities in secondary markets. Such acquisition deals are settled between the acquirer and acquiree on mutually agreed terms without any involvement of the clearing corporation or the stock exchange. Its properties are leased to healthcare service providers such as doctors, hospitals, care providers, etc. It has a portfolio of more than 300 leased properties located in 34 states, totaling approximately 3.2 million square feet.

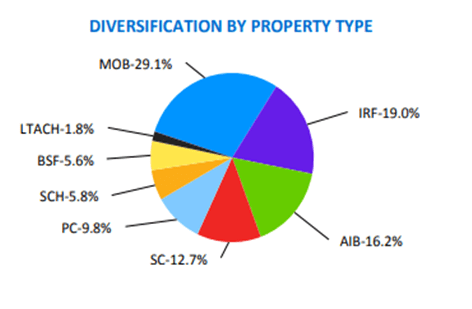

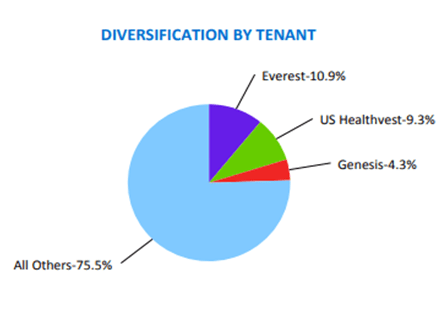

CHCT’s traditional medical facilities include medical office buildings (MOB), physician clinics, surgical centers and hospitals. Specialty centers include dialysis clinics, urgent care centers, inpatient rehabilitation facilities, behavioral specialty facilities, radiation oncology centers, and long-term acute care hospitals. CHCT’s properties have a high occupancy rate of almost 90 percent with lease expirations ranging from 2022 through 2039. However, the weighted average remaining lease term is somewhere around 7.5 years. At present, this REIT has more than 200 tenants, and none of those tenant accounts for more than 10 percent of total annualized rent.

CHCT Diversification by property type (CHCT website) CHCT Diversification by tenant (CHCT website)

Community Healthcare Trust Performed Much Better than What I Expected

I covered this stock almost 6 months back, and I was not bullish at that point. However, the stock was still generating a high price growth. In that article I mentioned that…

I don’t find any convincing reason to buy this stock. The only positive thing about this stock is its 50 percent price growth over the past five years. However, that growth was mainly due to the poor US equity market scenario five years back. Second half of 2017 and the entire 2018 were hugely impacted by US governments’ policies regarding tax cuts, and the economic scenario which was again impacted by unemployment, tariff hikes, etc.

Community Healthcare Trust performed much better than what I expected in May. Historically, it generated an annual average yield in the range of 3.6 to 5.6 percent, and its 4-year average yield stood at 4.1 percent. Despite such low yield and a very low asset base, this healthcare REIT generates a total return which is way above its peers. And in spite of a price loss of almost 25 percent during this year, CHCT has been able to post an annual average total return of 17.5 percent since 2016. This return no doubt is quite high, when compared to the broader market. During the same period S&P500 generated a return of less than 12.5 percent.

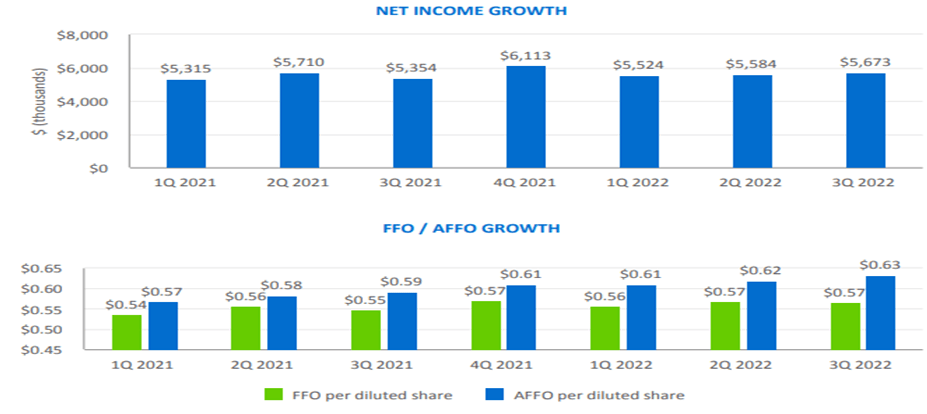

Community Healthcare Trust was also able to record significant growth in its funds from operations (FFO) – a key metrics for evaluating the growth of any REIT. During the past 20 quarters, its quarterly FFO per share rose from $0.37 to $0.57, and the average quarterly FFO during these 5 years remained at $0.47. That suggests FFOs are growing at a stable rate. Moreover, average FFO during this period was higher than average dividend pay-outs of $0.425. However, unlike FFO the pay-outs have not witnessed significant growth and have largely ranged between $0.4 to $0.45. In my opinion, this steady growth in FFO is one of the primary reasons for this stock doing well in the market.

Despite High Historical Growth, CHCT Has its Own Share of Challenges

CHCT’s growth is dependent on three basic factors – high FFO growth, long term lease agreements, and acquisition of properties at low cost. So far, the company has been able to successfully achieve all these three. But there are concerns going forward. FFOs have recorded significant growth from $0.37 to $0.53 between Q4, 2017 and Q4 2020. However, during the past 8 quarters, there is no significant growth in quarterly FFO. The same is the case for net income, which is moving around $5.5 million between the past 8 quarters.

CHCT Performance (CHCT website)

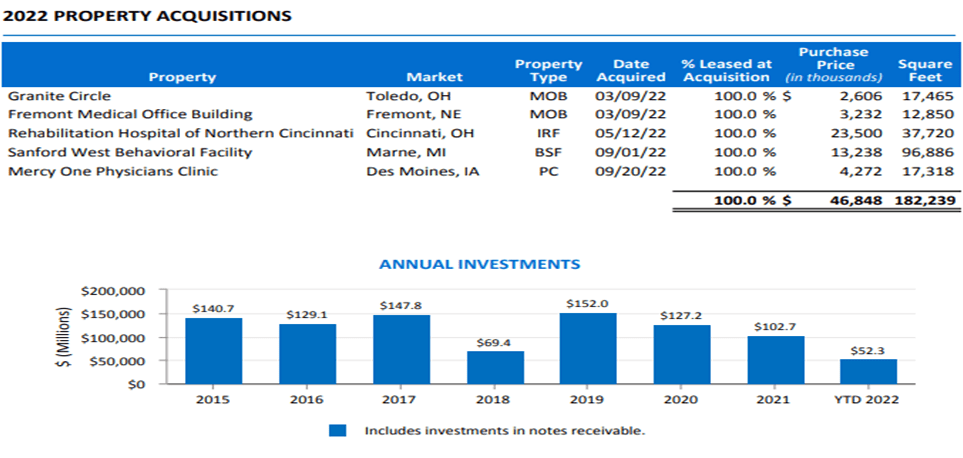

In order to grow its FFO exponentially, Community Healthcare Trust has to aggressively go for acquisitions of healthcare properties. However, the pace of acquisitions in 2022 has been disappointing. Till Q3, 2022, CHCT acquired only 0.18 million square feet of healthcare facilities, spending less than $47 million. Moreover, annual investments in acquisitions are decreasing every year, and the average annual investments stood at around $102.7 million, which is much lower than its annual investments in initial years. Since the company sources most acquisitions by means of personal relationships between senior management and healthcare operators, this raise concerns as to whether they will be able to continue discovering and closing those off-market or lightly-marketed acquisition opportunities.

CHCT acquisition (CHCT website)

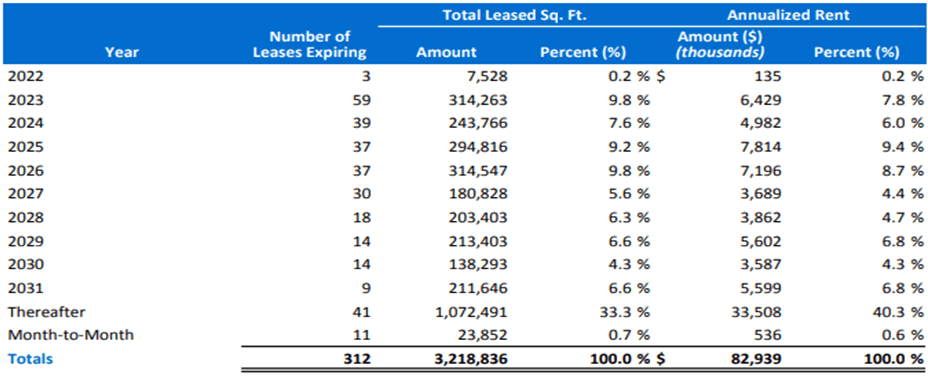

Long term lease agreements, another key driving force behind the growth of Community Healthcare Trust, is also under scanner. Although the lease agreements are expiring in a gradual manner till 2039, almost two-third of its more than 300 lease agreements are maturing within the next five years. When a large percentage of lease agreements expires within a short span of time, the company is bound to feel the pinch in its rentals and correspondingly in FFO. Another thing to consider here is that healthcare operators are less likely to compete with their peers for facilities in non-urban markets, where CHCT mostly operates. This will make things difficult for CHCT in order to find a tenant when an existing lease expires. However, the good news is that those properties constitute only 36.3 percent of CHCT’s annualized rent.

CHCT leases (CHCT website)

Investment Thesis

Community Healthcare Trust is a small-cap REIT that finances, acquires, or operates outpatient healthcare services at non-urban markets. The stock not only outperformed its peers, but also the broader market. Its properties have a high occupancy rate and are under long term lease agreements, extending up to 2039. It has a portfolio of more than 300 leased properties located in 34 states, totaling approximately 3.2 million square feet. The REIT has a huge tenant base, and has achieved significant growth from its funds from operations. CHCT pays quarterly dividends and generates a low but decent yield on a consistent basis. During the past 5 years, CHCT has ticked on all the necessary boxes that an investor seeks while investing in a healthcare REIT.

However, CHCT has its own share of challenges. During the past 8 quarters, there is no significant growth in its quarterly FFO. The pace of acquisitions has been disappointing and annual investments in acquisitions are decreasing every year. Since the company sources most acquisitions by means of personal relationships, this raises concerns as to whether they will be able to continue discovering and closing those off-market or lightly-marketed acquisition opportunities. Although the lease agreements are expiring in a gradual manner till 2039, almost two-third of those agreements are maturing within the next five years. Healthcare operators are less likely to compete with their peers for facilities in non-urban markets. Thus, although it is doing well at present and beating the broader market, I’ll be cautiously optimistic about investing in Community Healthcare Trust. However, there is no reason why existing investors should liquidate their stakes at this well-performing REIT.

Be the first to comment