I have recently written an article on PepsiCo (NASDAQ:PEP), one of the 20 names in my All-Equities SRG portfolio that I believe has been unjustly punished during the bear market of the past six weeks. Standing right next to it among battered consumer staples stocks is its big-brother rival Coca-Cola (NYSE:KO).

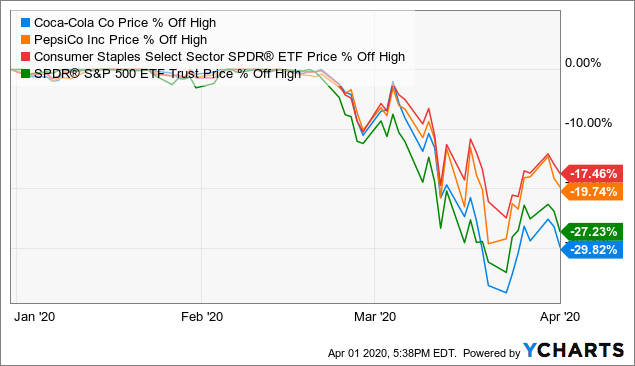

Shares of the Atlanta-based company, in fact, have corrected even more sharply than those of Pepsi (see first chart below). KO has been down an impressive 30% since its mid-February peak, which is a steeper selloff than those endured by the S&P 500 (NYSEARCA:SPY) and the Consumer Staples Select Sector SPDR ETF (NYSEARCA:XLP).

{kind=link}

Credit: The Intercept

Good for diversification and fundamentals

For similar reasons that lead me to believe that PEP is a buy at current levels, KO also looks compelling having just come off a five-year low share price of $38 (now $42) and trailing P/E in the high teens (now 20x). In my view, the most appealing feature of this stock is diversification which, to be fair, has not worked at all during the current market meltdown. But, also, I find it highly unlikely that a well-established global player in the beverage industry will suffer much through, and especially after, the current health crisis.

On diversification, it is worth noting that KO’s one-month price drop of 37.5% as of March 23 was the steepest experienced by the stock since the early 1960s at least. Such high correlation between shares and the broad market, even during periods of distress, is certainly not the norm. For example, since 1999, KO’s daily returns have only loosely followed the performance of the S&P 500, at a fairly low correlation factor of 0.49. During the mega bears of 2000-2001 and 2008-2009, KO’s cumulative market losses were less than one-third those of the S&P 500.

Data by YCharts

Data by YCharts

In what pertains to business fundamentals, it is understandable that Coca-Cola should suffer from the current coronavirus pandemic – just like virtually every business in the world, but likely to a lesser extent. The largest hit to the company will likely come from the concentrate side of the business, which, in 2019, accounted for 55% of Coca-Cola’s revenues. This is probably the case because restaurants and convenience stores have been hurt more severely by the worldwide quarantines. Finished products, on the other hand, might even benefit from the “pantry loading” phenomenon that has likely been a positive for snack and beverage peer Pepsi.

Looking past the current troubles, however, I believe Coca-Cola will experience little, if any, long-term deterioration in operational and financial performance as a result of COVID-19. While the company no longer expects to meet its financial outlook for 2020 due to the pandemic, and the revised guidance has yet to be delivered, beverage consumption and distribution should eventually normalize.

Coca-Cola had been growing revenues in each of its business segments before the COVID-19 crisis, even in the more mature North America region (ex-currency and M&A). Last time that I looked at the company’s financial results, both pricing and mix looked solid. Meanwhile, the more aggressive expectations for bottom-line growth in 2020 (now stale) suggested confidence in margin expansion, along with growth in free cash flow that I believe will eventually be achievable once again.

Affordable recession protection

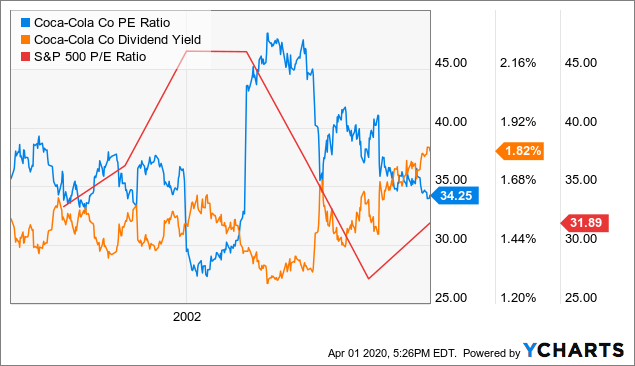

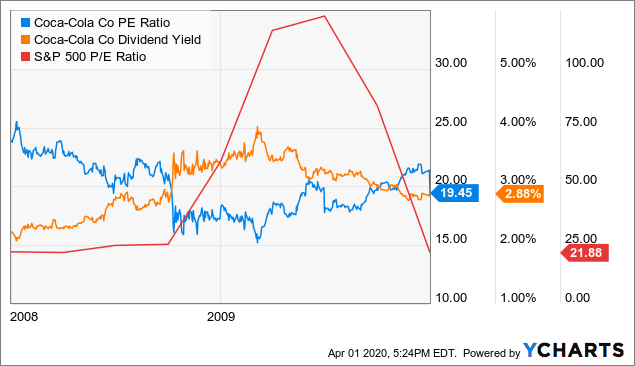

It is true that the good ol’ days of rich valuations have been left behind. For example, the S&P 500’s trailing P/E ratio has come down a massive six turns in only six weeks. Meanwhile, KO trades at a 20x multiple that is still higher than the broad market average.

But I believe the small valuation premium to be justifiable. Coca-Cola’s leadership position in the beverage space and unparalleled global reach should help it to maintain revenue growth and cash flow generation at reasonable levels even during a severe crisis, certainly relative to the rest of the corporate world. In addition, a trailing P/E of 20x and dividend yield of 3.7% are on par with, if not better than, KO’s comparable metrics during the two previous recessions.

Recession of 2001-2002:

Data by YCharts

Data by YCharts

Recession of 2008-2009:

Data by YCharts

Data by YCharts

Therefore, due to a combination of (1) the stock’s diversification properties, (2) fundamentals that will likely remain undisturbed in the long run and (3) share prices that have come down sharply and unusually fast, KO seems like a stock worth adding to a stock portfolio ahead of what will most likely be a period of global economic contraction.

Members of my Storm-Resistant Growth community will continue to get updates on PEP (allocation updates, insights, etc.) and the performance of my market-beating “All-Equities SRG” portfolio on a regular basis. To dig deeper into how I have built a risk-diversified strategy designed and back-tested to generate market-like returns with lower risk, join my Storm-Resistant Growth group. Take advantage of the 14-day free trial, read all the content written to date and get immediate access to the community.

Disclosure: I am/we are long PEP. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment