filadendron/iStock Unreleased via Getty Images

One stock many “keep it simple” investors start with is the time-tested and globally dominant Coca-Cola Company (KO). For over 30 years, Warren Buffett has openly named this specific brand as a “wonderful business“, and back in 2018 I named it one of the first ten stocks to buy for a ten year old, as many children able to read, drink, add, and subtract should be able to understand how this business makes money. Now that my then-10-year-old is now 16, I feel it is time to give him a more advanced investment lesson around the brand that remains his single biggest holding by teaching him to compare KO with the many other Coca-Cola branded stocks listed both in the US and around the world. These other stocks sharing the Coca-Cola name include the following, from largest to smallest as of this writing:

- United Kingdom-based Coca-Cola Europacific Partners PLC (NASDAQ:CCEP)

- Mexico’s Coca-Cola FEMSA, S.A.B. de C.V. (NYSE:KOF)

- Swiss-based Coca-Cola HBC AG (OTCPK:CCHGY)

- The US distributor Coca-Cola Consolidated, Inc. (COKE), and

- Coca-Cola Bottlers Japan Holdings Inc. (OTCPK:CCOJY)

Two other Coca-Cola stocks I would love to compare, but unfortunately don’t have tickers here on Seeking Alpha, are Turkey’s Coca-Cola Icecek and the separately listed Japanese bottler for the northern island of Hokkaido. Although I periodically compare all eight of these companies, for the purposes of this article, I simply wanted to run a comparison of KO vs CCEP and KOF to see which looked most attractive to add money to in today’s market. If any of the Dennison kids are also reading this, don’t expect this article to do your homework for you; I still expect you to read at least one annual report for whichever of the other seven Coca-Cola stocks you want to add to your portfolio.

This article mostly aims to be a comparison between Europe’s CCEP vs Latin America’s KOF, though I include the comparison to KO in case there are any factors that might make KO a better investment than the other two. For background, I also suggest reading my earlier article on Coca-Cola’s lost decades, and how I plan to avoid owning it over its next one.

Round 0: Size

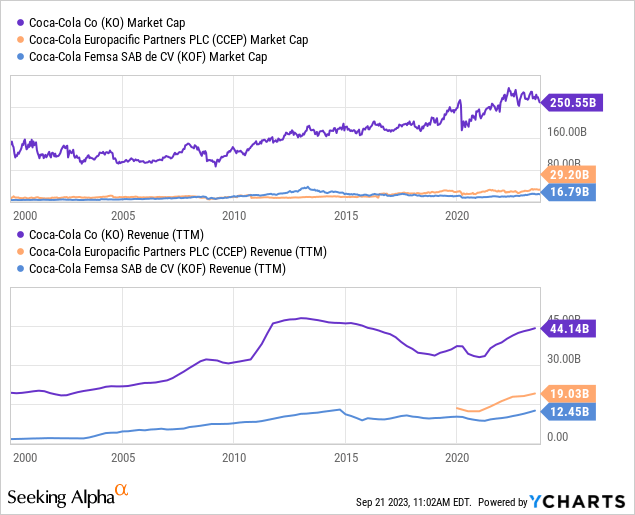

I’m guessing many readers of this article will of course know KO, but may not be as familiar with CCEP or KOF for one simple reason: the market cap of KO is more than 5x that of CCEP and KOF combined. The same can’t be said for size when measured by revenue, though, as KO’s total revenues are only about 50% more than the combined revenues of CCEP and KOF.

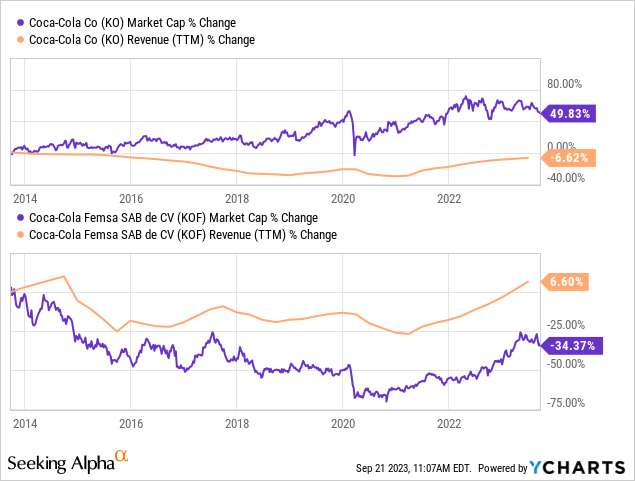

What I find especially notable is when I zoom in on the past 10 years, and look at how KO’s market cap is up almost 50% while its revenues have declined, while almost the exact opposite has happened to KOF. YCharts unfortunately doesn’t have 10 years of continuous data for CCEP, but overall, it seems KO might be getting relatively overvalued relative to the size of its sales in ways the other two are not.

I call this round zero because I don’t think it makes sense to call one stock or another a “winner” purely on size, but we will look at that growth factor later. Given that last chart, though, I feel KOF is already off to a bit of a lead.

Round 1: Dividend

Low-growth staple companies, like those with the Coca-Cola brand, are ones I mostly buy for their dividends, so I expect to start with a dividend yield at least as good as what I can earn on long-dated inflation-indexed bonds (LTPZ) (TIP), and a dividend growth rate significantly above the expected future rate of inflation. Since the yield on the long-dated TIPS in LTPZ and TIP is now around 2%, that means I would expect a dividend yield of at least 2%, which all of these names except COKE currently offer. Of these names, one with the highest yield is KOF with a 4% dividend yield, and I generally prefer higher yields to lower yields as long as the dividend looks solid, which generally means having a consistent history of dividend growth and earnings to cover that dividend growth. The dividend history of KOF on Seeking Alpha looks pretty solid going back to 1994, but since this is a Mexican stock, I also want to check the dividend record in Mexican Pesos on Coca-Cola Femsa’s own website. Here I see a solid record of dividend increases in pesos, with the most recent hike being from MXN 5.43 per share in 2022 to MXN 5.80 per share this year. I will put on my calendar to watch and see if we get another dividend hike in May 2024, but for now, I feel confident in declaring KOF the winner of this round.

Round 1 winner: KOF

Round 2: Earnings Surprises & Revisions

Given how large and widely followed KO is, it should come as no surprise that KO’s earnings surprises have been relatively small. Although they have been positive 7 out of the past 12 years, KO’s annual earnings surprises have tended to be on the order of less than +/- 1%, with the largest surprise over the past 12 years being the +2.7% surprise for the highly uncertain year of 2020. By comparison, the earnings surprises of CCEP and KOF have been much larger, with CCEP missing by over 13% in 2022, and KOF beating by 20% that same year. That KOF still had such a large earnings beat after beating estimates by 14% in 2021 tells me that analysts might still be underestimating KOF given its Mexico risk. Although both CCEP and KOF have seen positive earnings revisions this quarter, only 8 out of 13 of CCEP’s revenue revisions have been upward, while all 13 of KOF’s revenue revisions have been upward.

Round 2 winner: KOF

Round 3: Valuation

Here we see a very clear ranking according to Seeking Alpha valuation grades, which is not the same as a comprehensive manual valuation, but I still find very useful for getting a quick look at which stocks are relatively cheap vs relatively expensive. Here, we see KO currently getting a “D”, CCEP getting a “C”, while KOF gets a “B”. Looking through the components of these grades, I see no reason to make any significant adjustments, so on this basis, it again seems like KOF is the clear winner.

Round 3 winner: KOF

Round 4: Growth

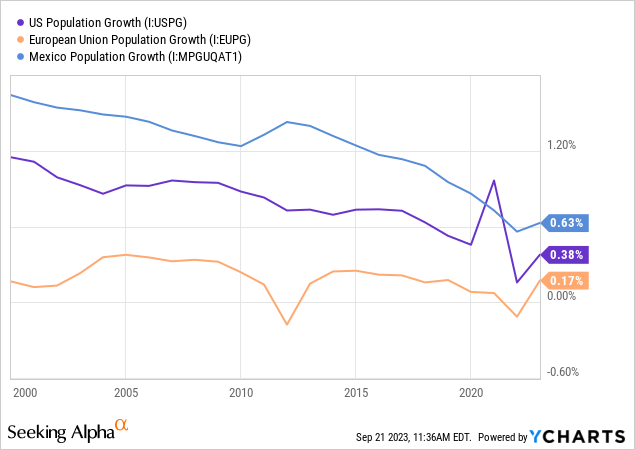

Here again looking at the Seeking Alpha grades for growth, we see KOF having the slightly better grade of a B-, compared with a current C- for both KO and CCEP. This makes sense from a high level if we are right about Latin America still being a relative “growth” market while the US and Europe are relatively mature markets, with even the parent Coca-Cola Company’s global brand already pretty saturated around the world by the turn of the century. As a sanity check on these growth rates, I quickly look at the population growth rates of these three regions, which although are declining across the board, are still higher in Mexico than north of the border or across the pond.

Round 4 winner: KOF

Round 5: Profitability

According to the current Seeking Alpha profitability grades, we finally see a category where KO comes out on top of the other two, with an “A+” profitability grade, versus “A-” for CCEP and “B+” for KOF. Given the different business of the relatively capital light parent and the more capital intensive bottling and distribution businesses, what actually surprises me about these grades is that KO’s grade is only 2 and 3 notches higher than CCEP and KOF respectively. I explain this by noting that A+ is the highest possible grade, and CCEP and KOF are still “highly profitable”, even if not quite as highly profitable as KO. So while KO would be the winner of this round in a 3-way race, I give this one to CCEP versus KOF.

Round 5 winner: CCEP

Round 6: Geographic Exposure

One factor which especially interests me as a global investor, and one which often requires some digging into annual reports, is the geographic exposure of the different businesses. Here, the parent KO is obviously the most global, so for this comparison, I mostly want to look at the geographic mixes of the revenues of CCEP versus those of KOF.

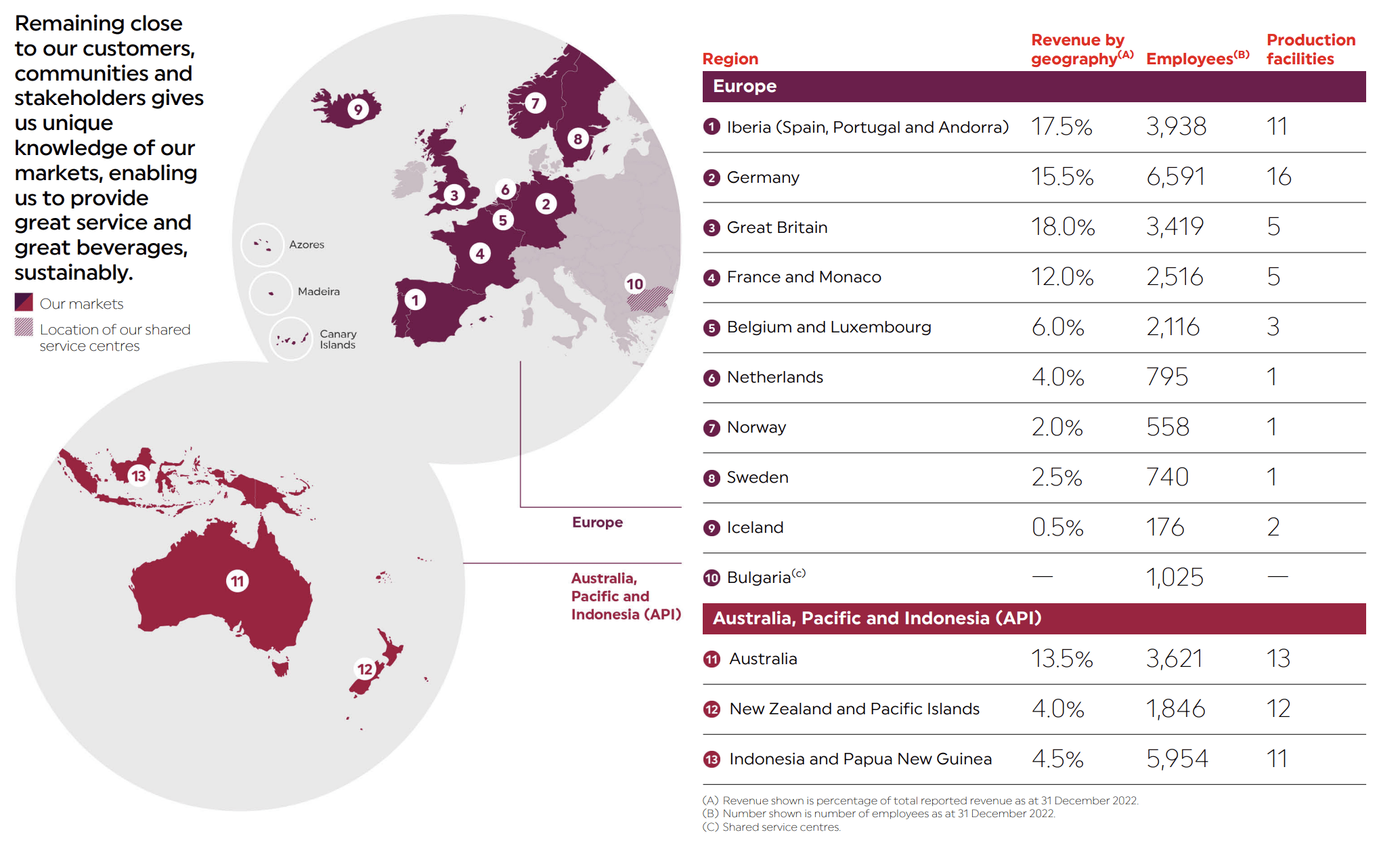

CCEP’s revenue breakdown appears on page 5 of their 2022 annual report, which shows that the vast majority of CCEP’s business comes from Western Europe, with a little more than 20% coming from Australia, New Zealand, Indonesia, and other islands in that region. I would rather see more exposure to Eastern Europe, Africa, or other parts of Asia, but for now, it is fair to say that CCEP mostly covers “developed markets”, while KOF as we will see covers “emerging markets”.

CCEP Annual Report 2022

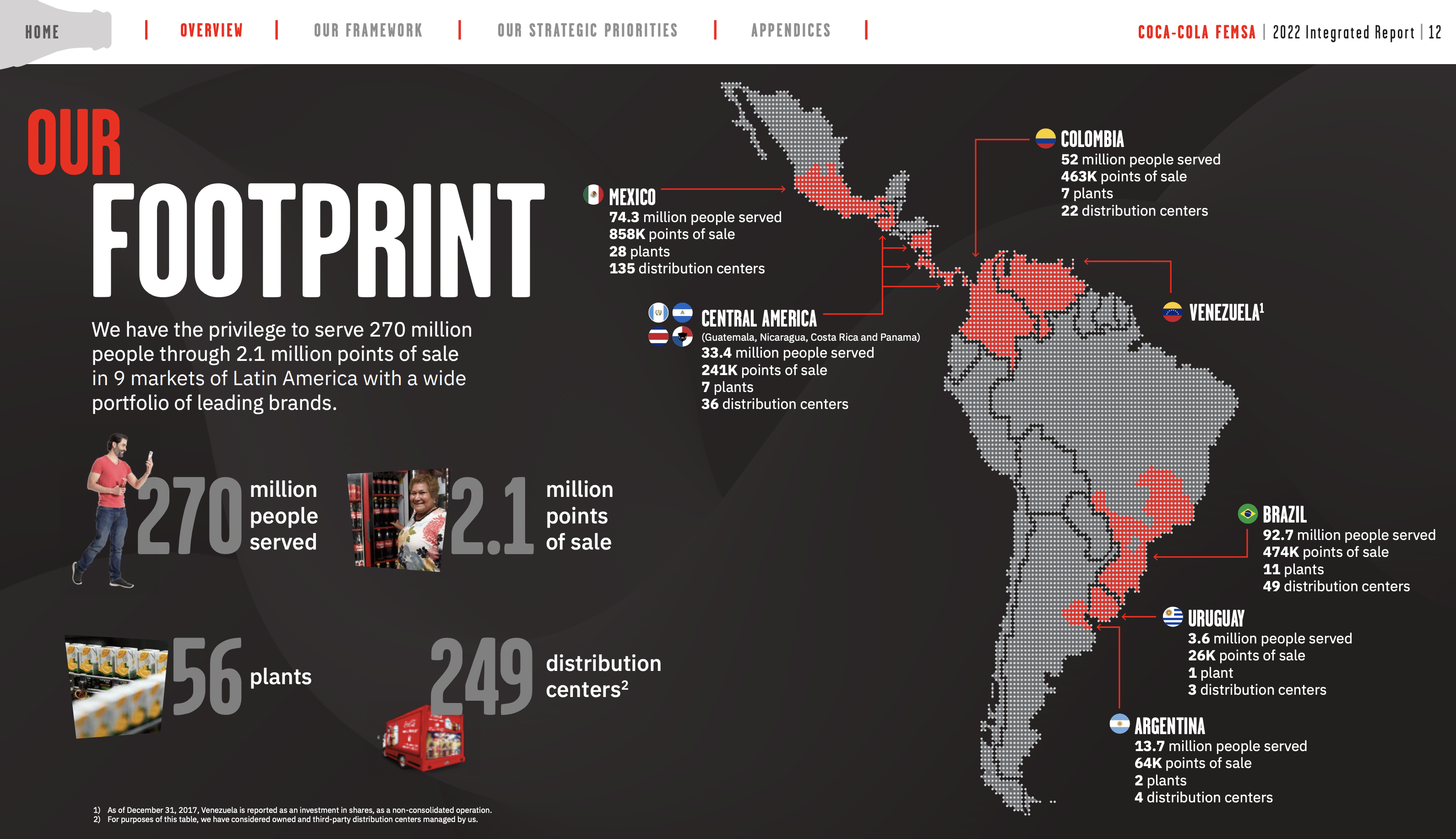

KOF’s geographic exposure appears on pages 12 and 13 of their 2022 annual report, which shows its three biggest markets are Mexico, Brazil, and Colombia, and that KOF also has a footprint in several other markets in Latin America.

Coca-Cola Femsa 2022 Annual Report

While this may seem like a cop-out, I generally like Coca-Cola businesses, and want to own them in every part of the world where I can earn a good rate of return. So I see balancing my risk between Europe and Latin America as a better way of doing this than simply owning one or the other, especially since the above differences in profitability and valuation are relatively minor.

Round 6 result: Tie

Conclusion

I own, and will continue to own, all of the names mentioned at the beginning of this article with the exception of COKE, so the comparison here is mostly a review on which ones I should buy more of at current valuations. Both CCEP and KOF seem significantly better valued than KO, especially when I look at metrics other than dividend yield, but when I consider the yield and growth prospects, KOF currently seems like a clear winner according to these rounds.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment