jetcityimage/iStock Editorial via Getty Images

A new year requires a new strategy as the market is consistently changing. Long gone are the days of tech stock dominance during the pandemic as the smart money continues to flow to the quality names and those with stable earnings. As the base case for 2023 has become a shallow recession, companies with earnings that can hold steady in a recessionary environment become great options for the coming year. Coke Consolidated (NASDAQ:COKE) the largest Coca-Cola bottler in the world is a perfect example, with very stable demand and earnings potential even in a recessionary scenario. The time to focus on technology and unprofitable companies is over, with the focus on quality cash flowing businesses with stable revenues. COKE can continue to increase dividends and accelerate returns to shareholders, allowing for future multiple expansion in the stock in coming years.

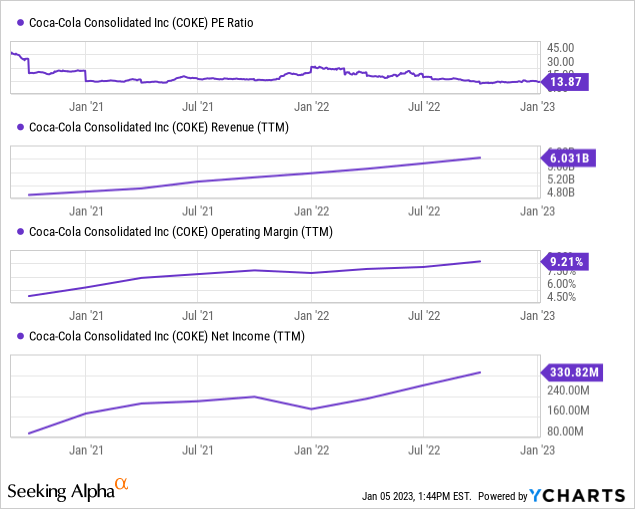

Q3 strength and Growing dividend

As you can see above, COKE has seen no P/E expansion over the past 2 years even as the company has increased operating margin from 6.2% to 9.2%. The revenue growth has stayed consistent in that time, with 11.7% revenue growth in the most recent quarter over Q3 2021. Gross margins have improved significantly as inflation pressures are starting to subside, with 38.1% gross margins over 35.5% in 2021 Q3. This led to a significant increase in net income, up to $189.9 million from $137.0 million last year or a 38.6% gain. Gross margins have been as high as 42% in past years, and an increase in efficiency bottling could lead to that level again in the coming cycle. This could mean an operating margin north of 12% within 5 years. Net income has increased significantly yet the stock has not been rewarded with margin expansion. Expectations are for 3%+ revenue growth in 2023, with upside likely as the consumer remains strong. Debt is down to under $600 million, with just 0.6 debt to shareholder equity. This gives COKE flexibility to make acquisitions as the company has great cash flow to pay back debt if an opportunity presents itself. Growth in automation is a long term tailwind for the stock, as the company reduces labor as a % of expenses and gains efficiencies on costs.

Aluminum prices are falling significantly and will provide a continued tailwind as industrial applications slow in 2023. As you can see below the peak was in early 2022 due to the inflation spike from the war in Ukraine. Since the price has trended back towards long term average which is around $2000/ton. Trading economics shows that economists predict a continued fall with a consensus of $2142 a year from now. Labor won’t be as much of a headwind in 2023 with wage increases likely to be closer to 3% than the 5+% of 2022. This means additional cash to the bottom line to come in 2023. Selling, delivery and administration expense will likely decline from 26.5% of sales in 2023 with the reduced labor pressure. Transportation costs will see benefit as Diesel prices peak out and decline with increased production coming online in 2023. This is one of the hardest costs to predict but should decline from these extreme levels over time at $5.10/gallon.

Aluminum Price 2018-2023 (Trading Economics)

Improvements in margins as well as a strong consumer throughout 2022 were a great boon for COKE. Management sees this great momentum in earnings and cash flow allowing a robust dividend increase of 100%, plus a special dividend of $3.00 being paid in February. While the stock only pays out $2.00 per year baseline for 2023, they have potential to raise the dividend further over time. The company sees continued growth as a more important avenue, plus the company is paying down debt consistently. Major service locations like restaurants and sports venues have seen a return to growth with the reopening of the economy increasing demand. Monster Beverage (MNST) and sparking beverages are areas of strong demand growth which should continue into 2023. As many people have seen with shrinkflation, mini-cans are an area of growth allowing for improved margins and increasing volumes as well. Innovation in the industry will continue to assist in volume expansion and continued service growth will help lead to growth in revenue even in a difficult macro environment.

Bottom Line

Anyone investing for 2023 must be looking at capital preservation first and foremost with a focus on quality names. If demand and consumer strength wanes, owning a stock with very stable demand like COKE will prove prudent. The stock will continue to outperform longer with margin and cash flow improvements as well as dividend increases. Dividend growers will continue to beat the market, as investors continue to move money from cash burners to cash flowers. The company is a consumer staple with a solid growth rate over the past 5 years, putting it in the sweet spot. It would be a good riskier option for income oriented investors and a safer option for growth investors looking for a safer dividend grower.

Be the first to comment