niphon

Investment Thesis

CNH Industrial’s (NYSE:CNHI) stock is up ~37% since our last article in July. The company is experiencing good demand in the agriculture segment, which should continue into FY23. This, along with the projects related to the U.S. Infrastructure funding, should support revenue growth in FY23. The strong tailwinds in the agriculture end market and public construction should more than offset the softness in the residential end market. Higher price realization and sequential improvements in the supply chain constraints should benefit revenue growth. The margins should benefit from volume leverage, higher price realization, and the company’s efforts to control SG&A expenses.

Revenue Outlook

In Q3 FY22, the net sales increased by 24% Y/Y due to favorable price realization and increased volume, partially offset by a negative FX headwind. The net sales in the Agriculture segment increased 26% Y/Y due to strong Ag demand in Latin America and North America, favorable price realization, and a better mix, partially offset by the negative impact of foreign exchange rates. The Construction segment’s sales increased 16% Y/Y driven by favorable price realization and the contribution from the Sampierana business acquired in December 2021. In the Ag segment, the order book for tractors and combines is down ~10% and ~20% Y/Y due to the pause in taking new orders. The company is restricting new orders to maintain the price-cost balance in FY23 and to enhance its ability to deliver on time to its dealers and customers. The order book in the Construction segment was up ~20% in both Light and Heavy equipment due to the strong demand in North and South America.

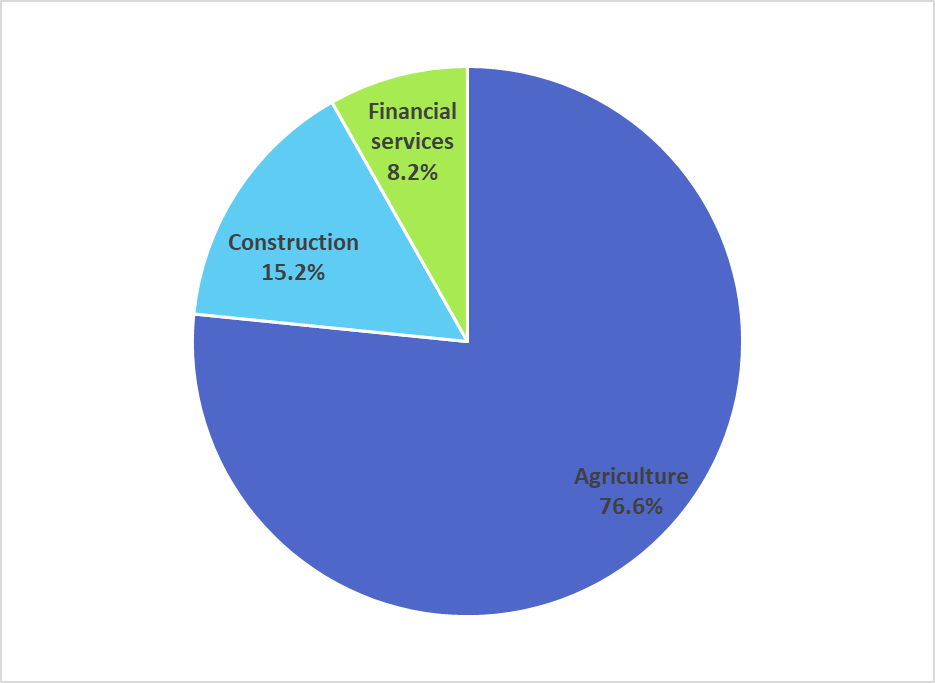

CNHI’s segmentwise distribution (Company data, GS Analytics Research)

Looking forward, the demand in the agriculture end market remains strong. Commodity prices have declined from the highs set at the onset of the Russia-Ukraine war but remain above the pre-pandemic and year-end 2021 levels. This creates an opportunity for CNHI’s precision agriculture products that are efficient and help farmers manage the elevated input costs. In North America, the demand for high-horsepower tractors remains strong, and industry-wide OEM supply and dealer inventories remain low. The demand for CNHI’s Ag products also remains strong in South America. In the Construction end market, the demand trend in the residential end market is experiencing softness due to rising interest rates. However, public construction remains strong and should offset the weakness in the residential market as the spending from the U.S. infrastructure bill ramps up in FY23.

The company is continuing to invest in the future by expanding its precision Ag product portfolio and creating the next generation of agriculture and construction products. The integration of Raven Industries’ technology with CNHI’s products is benefiting the company. In the Ag segment, the company launched the Case IH Trident 5550 applicator, which includes Raven autonomy and is a driverless spreader with Level 4 supervisor autonomy. In the Construction segment, the company started selling Sampierana mini excavators in Europe in the third quarter of FY22 and has opened a new assembly line to increase the capacity for those products. The increased throughput should help the company export products to other regions in FY23.

I believe CNHI’s revenue in FY23 should benefit from higher price realization, improvement in the supply chain, and strong demand in its end market. The company opened its order book for Ag products in several regions in November. The healthy demand trends in the Ag market and public construction should more than offset the slowdown in residential and commercial markets.

Margin Outlook

The gross margin in the third quarter of 2022 improved by 260 bps Y/Y primarily driven by favorable pricing, offsetting higher input costs. SG&A as a percentage of sales declined 180 bps Y/Y to 7.2% as the company is continuing to manage costs in front of increased activity levels. The adjusted EBIT margin of industrial activities (Agriculture and Construction segment) improved 270 bps Y/Y to 12.4% due to improved gross margin, lower SG&A as a percentage of sales, and volume leverage.

Looking forward, I believe the company’s margin should further benefit from the higher price realization. Additionally, the improvement in product mix and volume leverage from strong demand should support margin growth. The company is also working on controlling its SG&A expenses and improving its productivity.

Valuation & Conclusion

The stock is currently trading at 10.13x FY23 consensus EPS estimate of $1.60. The company is experiencing good demand in its Agriculture end market, which should continue into FY23. This, along with projects related to U.S. Infrastructure, should more than offset the weakening demand in the residential and commercial end markets. Additionally, the revenue growth should benefit from the higher price realization as well as improvement in supply chain constraints. The volume leverage from the strong demand, higher price realization, and the company’s initiative to control its expenses should benefit the margins. Given the good growth prospects and low valuation, I have a buy rating on the stock.

Be the first to comment