imaginima/iStock via Getty Images

Investment Thesis

Cloudflare (NYSE:NET) is about to report its Q4 earnings this Thursday after hours. With the stock going nowhere in two years and being down more than 70% from its all-time highs, it’s worthwhile revising this investment thesis.

Clearly, investors got too excited about Cloudflare in the bubble years. And frankly, I don’t believe many shareholders would contradict that statement. Moreover, the path from this point is far from easy.

That being said, I charge that the stock is now derisked, with the multiple today meaningfully more attractive. This is not the time to give up.

The Message Percolating Through The Earnings Season

Results from Microsoft’s Azure (MSFT) and Amazon’s AWS (AMZN) echo each other. Enterprise spend is coming down. There was a lot of excitement from digitally enabling platforms, and companies in unison bought into the idea that they needed to increase their cloud infrastructure.

Furthermore, 2022 saw companies buy into the idea that cyber security was not a discretionary item. In the same way that households buy flood insurance after a recent flood, the same dynamics took place here.

With the black swan events in Europe, companies suddenly turned their focus to ensure they had all the cyber security protection they needed to operate in a zero-trust environment.

That being said, presently, perhaps due to the inflationary environment or the effects of higher interest rates or possibly both, the narrative coming out of those two tech giants is that cloud spend is slowing down. This will affect Cloudlfare’s performance in 2023.

Meaning that this could cause a near-term hiccup in Cloudflare’s prospects and something that we should keep our eyes on.

But there are more reasons to be bullish on Cloudflare.

Cloudflare’s 2022 Didn’t Miss a Beat to Gain Market Share

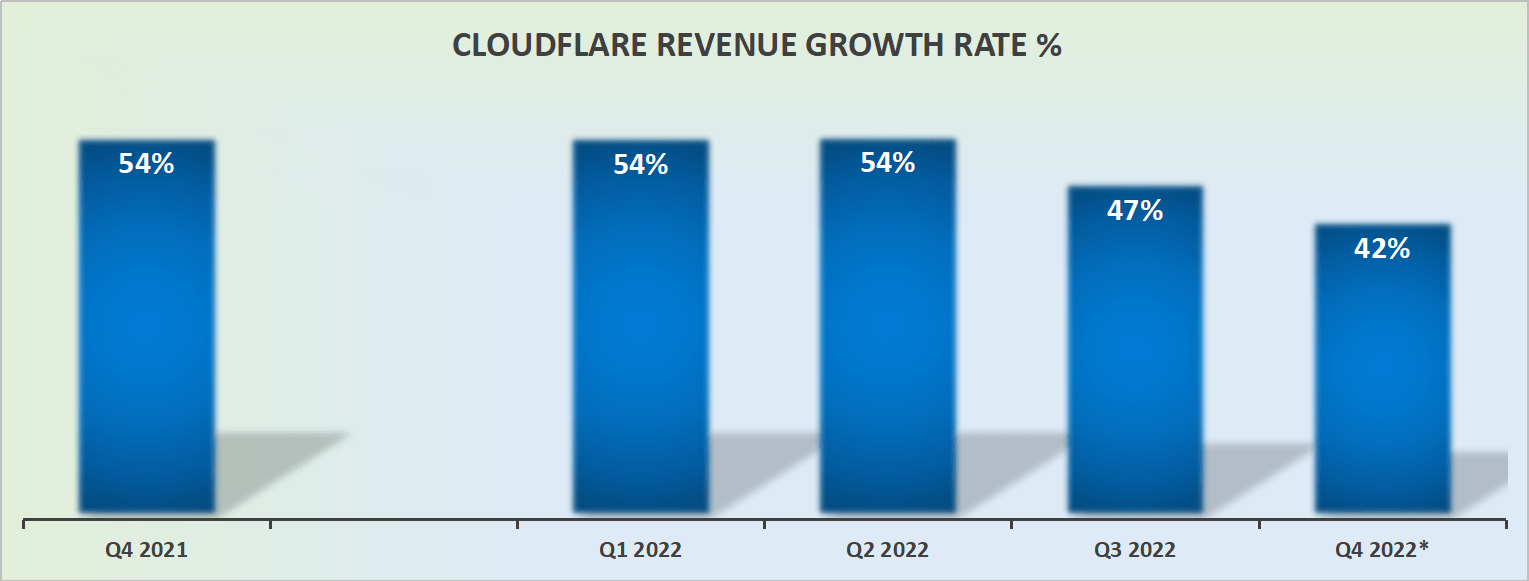

NET revenue growth rates

I recognize that Cloudflare’s growth rates have been nothing short of astonishing. It’s one of the few companies within the SaaS space that has continued to grow relentlessly and persistently throughout 2022 without missing a beat.

While many of Cloudflare’s peers in 2022 reported slowing growth rates, Cloudflare has not missed a beat.

If I was to posit one consideration that allowed Cloudflare to outdistance and gain market share from the likes of Fastly (FSLY), it would be down to Cloudflare’s culture. While many of Cloudlfare’s peers used a usage-based revenue model, in the long run, that lead to their customers feeling deceived.

As the customers scaled their operations, they ended the month with a huge bill. This could certainly be a contributing factor. Treat your customers as you’d like to be treated.

NET Will Not Go in the Bargain Basement

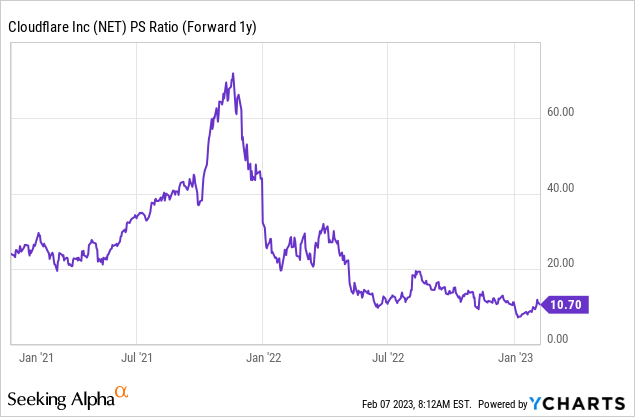

The graphic that follows highlights the gut-wrenching journey that shareholders have been on with Cloudflare.

As it stands right now, Cloudflare is priced at less than 11x forward sales. This is the lowest multiple the company has had for a while (ever?).

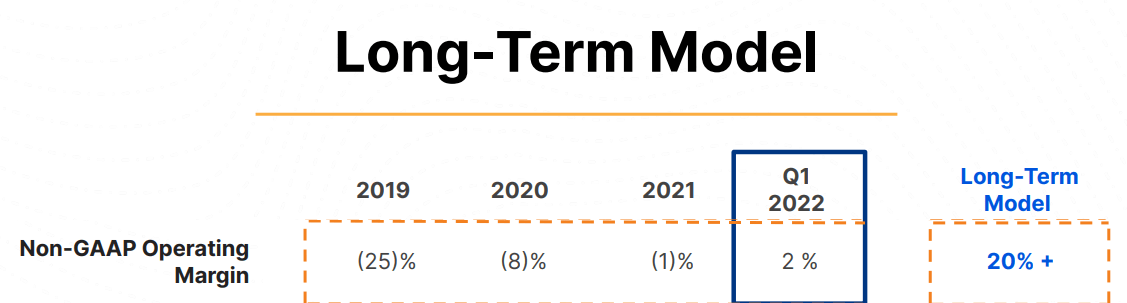

While I recognize that Cloudflare’s growth rates in 2023 are unlikely to be a match to its 2020-2022 period, this line of thinking detracts too much from the fact that Cloudflare was already profitable before it was ”cool” to be profitable.

NET investor day

Cloudflare has often alluded to the fact that it ”chooses” to be barely profitable. And that if the business was to make a profit, that would mean that in that period it wasn’t aggressive enough in gaining market share.

While that sort of aggressive stance made sense when interest rates were at close to 0%, I’m not sure that the same can be said now with interest rates headed for 5%.

The Bottom Line

In sum, there was a lot of frothiness and Kool-Aid drinking in the market and within the whole of the technology sector in the past couple of years.

But now that most tech companies have seen investor expectations reset, I am of the opinion that innovative companies can change their corporate culture from a ”growth at any cost” mindset to a smaller and yet more profitable growth propensity. The companies that succeed in this pivot will be the best companies to come out of 2023. I’m bullish on NET.

Be the first to comment