imaginima

Investment Thesis

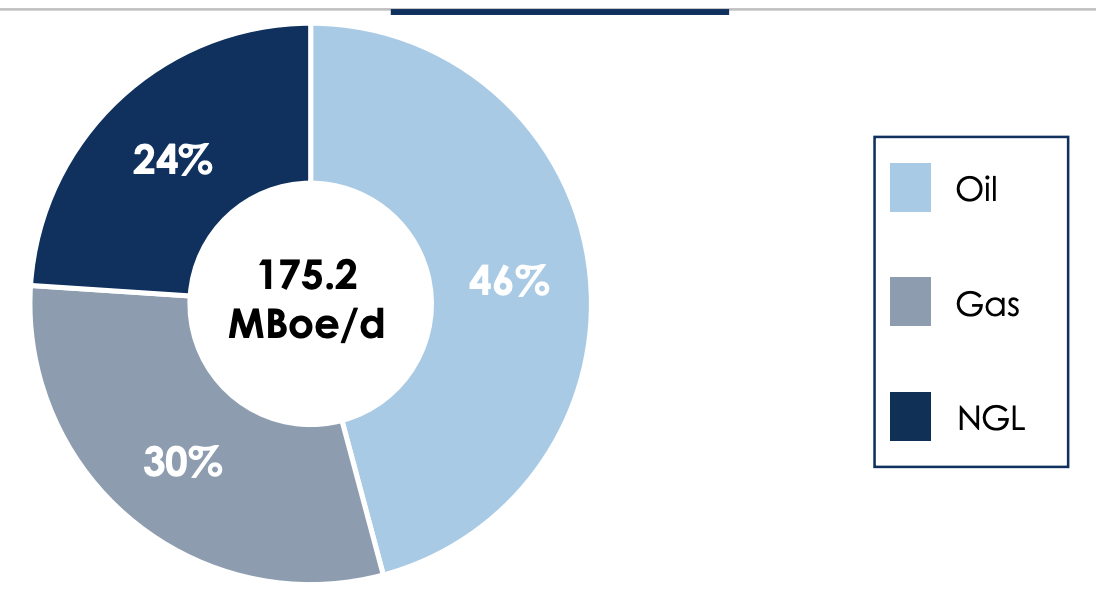

Civitas Resources, Inc. (NYSE:CIVI) is an oil and gas producer focused on the Denver-Julesburg Basin (DJ) in Colorado. Over approximately 500,000 acres, CIVI produces 175.2 mboe/d (thousands of barrels of oil equivalent per day).

What sets CIVI apart is its low cost of operations, which produces a high free cash flow (“FCF”) yield of 30%. The average annualized cash and lease operating expenses (LOE) cost for FY22 is at a sector-low $4.1/boe. CIVI has a fortress balance sheet with very low leverage target of only 0.5x Debt to EBITDA. This allows them to use much of the cash on hand for dividends, paying out a dividend yield north of 10%.

The sales volume marks a 314% increase in crude oil equivalent, with a 79% increase in average sales price over the same 2Q22 period, year over year.

Currently, the yield is at 12% with a base of 3.1% and 50% of trailing FCF paid out as a variable. The declared 3Q dividend represents a 30% increase to yield quarter over quarter, with $0.46 paid out as a base and $1.30 as a variable. This brings the annualized dividend up to $7.04.

We believe that the stock is deeply undervalued and could easily double over the next year as investors realize the sustainability of the free cash generation and dividend that CIVI has.

Estimated Fair Value (EFV)

EFV = E2023 EPS of $12.00 times P/E of 9 = $12 X 9 = $108

CIVI 2Q22 Report

|

Civitas Resources (CIVI) |

E2022 |

E2023 |

E2024 |

|

Price-to-Sales |

2.1 |

2.0 |

1.9 |

|

Price-to-Earnings |

7.2 |

6.3 |

5.4 |

|

EV/EBITDA |

3.0 |

2.7 |

2.7 |

Business Model

Oil and gas tend to be an expensive, high-leverage industry. However, CIVI remains committed to a “relentless” focus on keeping operating costs down.

Expenses remain low for the sector, per barrel of oil equivalent: $2.63 going toward leasing, $4.99 going toward extraction, and $0.47 going toward midstream expenses. Year over year, costs have greatly increased in extraction at 40% but CIVI has saved significant money on midstream expenses after acquiring its own architecture. According to CIVI, extraction costs have a direct correlation to sales volumes, which increased 314% over the same period given the large boom in oil and gas recently. This is also aided by their pure-play strategy within the DJ basin, which has proven reserves well past 2030.

These sector-low expenses allow CIVI to spend nearly $1 billion a year on capital expenditures, with at least $890 million going toward drilling and completion costs and $80 million going toward land acquisition costs and midstream costs. Excluding derivatives, CIVI could expect to see just over $1.5 billion in free cash flow at a yield of just over 30%. With the EIA expecting oil prices and gas prices to remain inflated well into FY23, CIVI’s operations are very low sensitivity.

So far in 2022, CIVI has 575 wells in the regulatory approval pipeline, with 70 locations fully approved, with 65 more awaiting final decision. The rest are in various stages of development, but CIVI expects to bring online 190 wells by the end of FY22.

|

Area Owned |

Total Undeveloped Locations |

Weighted Average IRR (from CIVI) |

|

Southern Basin |

407 |

43% |

|

Western Basin |

301 |

66% |

|

Eastern Basin |

256 |

29% |

Expansion

In our previous report, we talked about the March 2022 acquisition of the privately held Bison Oil and Gas. As Bison’s wells are retooled and connected to CIVI’s architecture, it is estimated that an extra 9,000 boe/d will be added to production with a 75% oil mix which is beginning to materialize.

Additionally, CIVI’s natural gas midstream capacity is roughly equivalent to where it was in 1Q at 315 mmcf/d with 280 miles of pipe, and crude pipelines of 35 miles with 77 mboe/d in capacities. Overall the midstream operating expense, including own and leased pipelines, is $0.47/boe, which is decreasing quickly. This is a serious reduction year-over-year in midstream costs at 57% despite their relatively modest book value of $320 million.

Risk

Commodity price risk is the biggest risk for any exploration and production company, including CIVI. We expect the demand for natural gas to continue to grow over the next 5 or 10 years as electricity production moves away from coal, and as Europe is cut off from Russian gas. Including the use of derivatives, CIVI has increased its realized price by 73% year over year in barrels of oil equivalent sold and maintains a modest hedging strategy.

Conclusion

Due to the explosive growth in CIVI’s dividend, and sustainingly favorable pricing for energy, we upgrade CIVI to a strong buy. Things have only gotten better for the stock, while the price has taken a small pullback from our previous buy rating. We believe that CIVI is undervalued, and often flies under the radar relative to its yield and valuation.

Be the first to comment