Andy Feng

This is an update to my previous article in November 2022, on the resumption of share buybacks by Citigroup (NYSE:C). The focus of this article is on how Citi will likely optimize its balance sheet to drive lower capital ratios in 2023 and beyond.

An essential part of the investment thesis in Citigroup is its ability to buy back shares with well-below intrinsic value. After all, Citi is currently trading at 0.6x tangible book yet with a very credible path to deliver >12% RoTCE in the next few years. So buying back shares at the current valuation is exceptionally accretive for EPS or simply put, it is similar to buying a dollar for 50 cents.

Unfortunately, as many readers may be aware, Citi had to suspend its buyback program due to an increase of 1.5% in its capital requirements arising from:

- The 2022 CCAR stress test cycle where Citi’s Stress Capital Buffer (“SCB”) unexpectedly increased from 3% to 4% (more on that later).

- Citi’s GSIB surcharge increased from 3.0% to 3.5%

Citi’s previous minimum capital requirement (“CET1”) was 10.5% whereas currently, it is 12%. As Citi also maintains a management buffer of 100 basis points, the target capital ratio for Citi is ~13%.

Longer term, Citi expects its target CET1 ratio to remain in the range of 11.5% to 12%. Citi’s strategy of divesting its global consumer bank and pivoting to more stable businesses such as Services and Wealth Management should be very supportive of reducing its targeted capital ratios. As of Q3’2022, Citi’s CET1 ratio sits at 12.2%, so 80 basis points short of its targeted 13% target. Citi expects to reach its target by Q2’2023

Investors, quite naturally, are extremely focused on when Citi will resume buying back shares.

Understanding CCAR stress tests and the SCB

It is all to do with the Fed’s CCAR stress tests which introduce volatility to the capital requirements of the banks. In other words, the minimum capital requirements of large U.S. banks change every year depending on the CCAR results (or more specifically, the Stress Capital Buffer or SCB for each bank).

SCB is measured as the maximum capital drawdown for each firm under the Fed’s severely adverse scenario. The higher the drawdown the more capital a particular bank would need to maintain in the next 12 months.

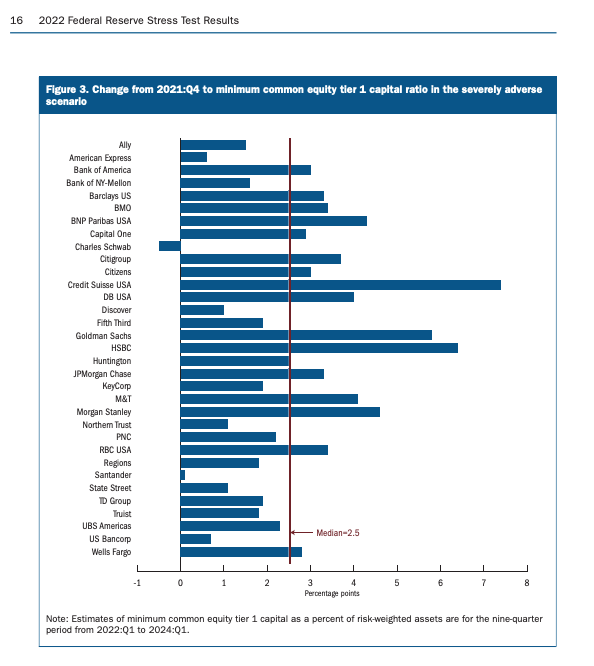

The 2022 SCB results for all the banks are shown below:

Federal Reserve Website

As you can see from above, Citi’s SCB in 2022 is 3.6% above the median of 2.5% and thus rounded up to 4% in its minimum capital requirements effective as of 1st October 2022.

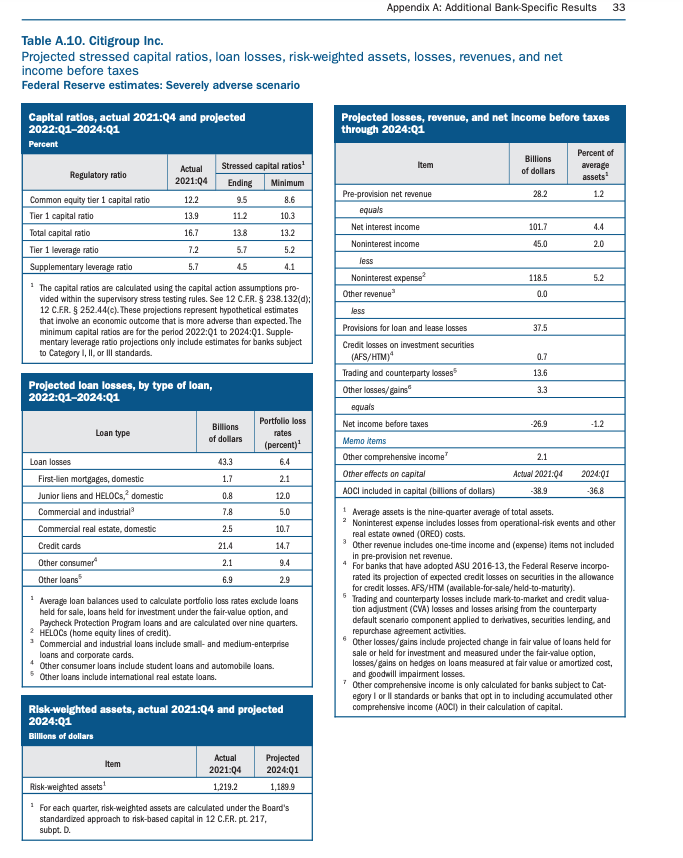

The below chart delves into Citi’s specific CCAR calculation:

Federal Reserve Website

As you can see above, Citi’s starting CET1 position was 12.2% with a minimum ratio of 8.6% representing a maximum drawdown of 3.6%.

The key drivers for the SCB calculations are:

- Pre-provision net revenue estimates

- Loan loss provisions (i.e. $43.3 billion)

- Trading and counterparty losses (i.e. $13.6 billion)

Why is Q4 positioning so important?

The 2023 CCAR calculation will be published in June 2023 and again may change the minimum capital requirements for Citi. Importantly, it is calculated on the basis of the 31 December 2022 Citigroup’s balance sheet. I expect Citi to position its balance sheet in Q4 to optimize the 2023 CCAR outcome.

There are a number of important considerations and potential differences from the 2022 cycle. Firstly, I expect the pre-provision net revenue estimates to be marginally better as the less volatile Services businesses’ (TTS and Security Services) revenue have outperformed in 2022 and should be a tailwind.

Loan loss provisions should be broadly flat. The increase in Cards loan balances may be offset by some of the disposals in the global consumer business. Ultimately though, the main driver will be the scenario outlined in the Fed’s severely adverse scenario.

Finally, the trading and counterparty losses item will be an important one. This scenario contemplates a default of a major counterparty of Citigroup (e.g. assumes JPMorgan (JPM) defaults). There are a number of actions Citi can take to optimize this line item. For example, it can manage its net derivatives exposure to a particular counterparty or purchase additional out-of-the-money options/tail risk hedges to bring down its overall risk exposures. In prior CCAR cycles, Citi’s losses from the trading and counterparty scenario were much lower than in the 2022 cycle.

I expect Citi’s management team to be laser-focused on ‘managing’ the CCAR results in the 2023 cycle.

Final thoughts

The 2023 CCAR cycle is an exceptionally important catalyst for Citigroup. I expect Citi to be able to manage its SCB from 4% to 3.5% or lower (but ultimately depending on what the Fed’s CCAR scenarios would look like).

In the interim, Citi should continue to build its capital position. One of the first items, I will be looking at in the Q4 earnings release is going to be its CET1 position (expect 12.5% or above). By the 2nd half of 2023, Citi’s capital target could reduce to 12.5% or lower – this could mean that Citi will find itself with excess capital (especially as more divestments close and release capital over time). Citi should then be in a position to massively buy back shares.

One risk to highlight is the early indications by the Fed’s regulatory chief on the need to potentially increase banks’ capital requirements (see this article), in my view, any modifications will be quite prolonged (subject to lobbying and consultations) and in any case, should not be implemented before 2025.

There is a lot to like about Citigroup in 2023 and beyond and it remains my #1 conviction buy for 2023 in the U.S. banking space.

Be the first to comment