FotoMaximum/iStock via Getty Images

Quick Investment Take

When I look at Chubb (NYSE:CB), I see a multitude of reasons on why it could be a great investment. In pursuit of flashy growth it’s easy for investors to forget the point of investing and the primary goal of any business. The primary goal of any business is to increase the value for shareholders and for some time now, I see this reflected more in Chubb than a lot of other stocks. What factors allow Chubb to achieve this?

- Diversified Business

- Strong Financial Performance

- Strong position (Market and Profitability)

In my write-up I will expand on each of these factors and also offer insight into how it can provide less correlated returns against the index which is important if you have a concentrated market exposure.

Diversified Business Model

Chubb is a global insurance company (world’s largest publicly traded P&C insurance) that provides a wide range of insurance products and services to individuals, families, and businesses around the world. For individuals and families, their wide array of products cover Home, Auto, Valuables, Boats & Yachts, Cyber, Liability, Travel, Natural Disasters and bespoke services. Under Business Insurance, they cover a broad range of services with categories extending from Accident and Health Insurance to Workplace benefits.

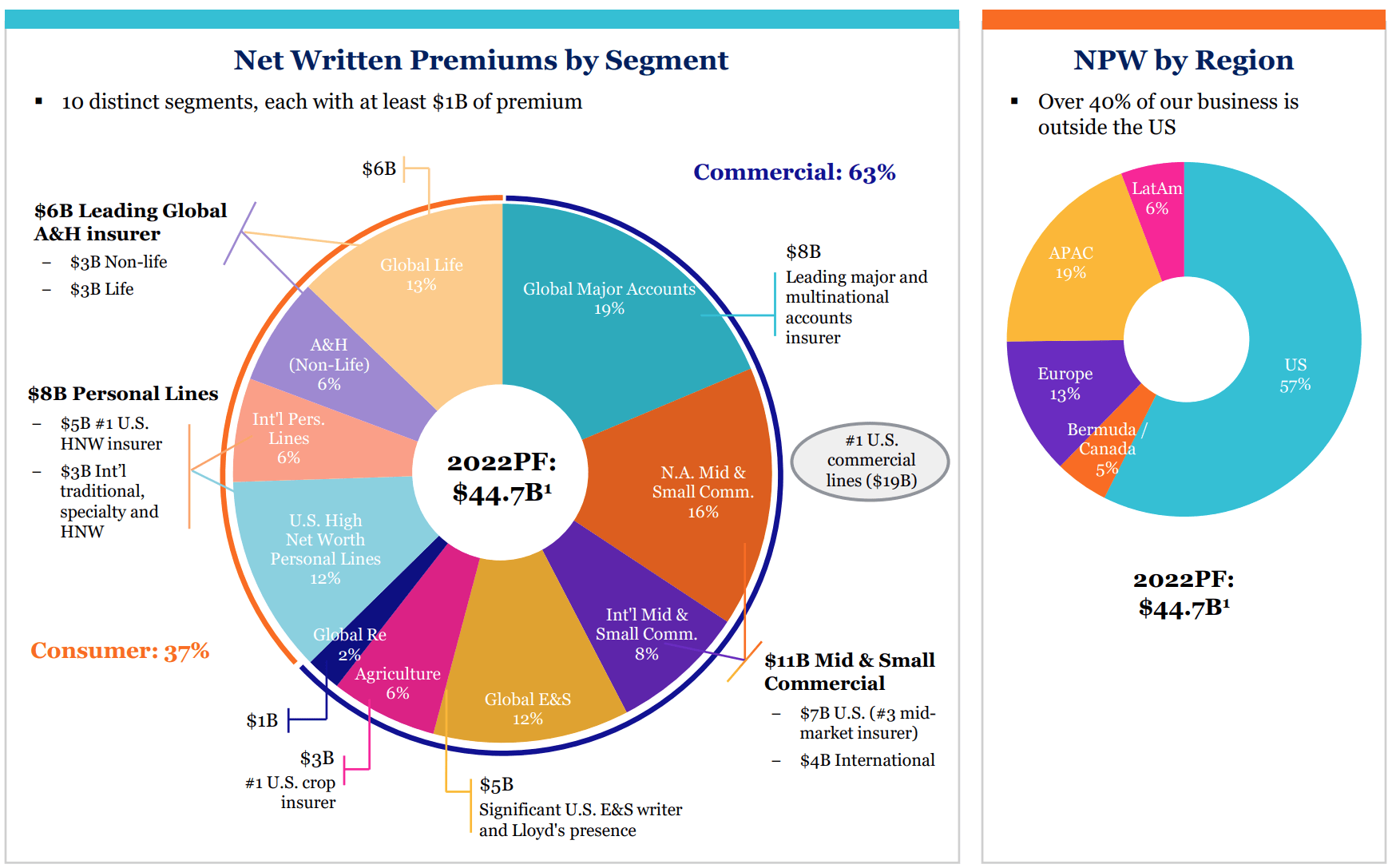

This diversification is all the more evident when one looks at how premiums are distributed across segments. With multiple distinct segments having at least $1B in written premiums, the business is estimated to generate more than 40% of its premiums outside of its core US market for 2022. Over the last ten years, its consumer to commercial split has also improved from being 28% of its premiums to 37% of its premiums.

Company Website – Investor Presentation

Strong Financial Performance

Let’s look at its Q3 YTD 2022 performance and compare this against the same time period of 2019

- Gross premiums written stands at $39.6B an increase of 31%

- P&C underwriting income stands at $3.4B, an increase of 56%

- Core operating income at $4.8B an increase of 32% from 2019

- Core operating Earnings Per Share at $11.2, an increase of 43%

- Operating Cash flow at $8.6B an increase of 75%

Chubb has had one major acquisition in the last five years (Cigna) which has been a contributing factor to its growth in business. There is confidence that Chubb can maintain its momentum on growth. As part of its growth and long term strategy, it is expanding its Asia presence through increased ownership stake in Huatai. Its vision is to significantly grow and improve Huatai’s profitability over the next 5 years and a big opportunity lies in the Chinese insurance market itself which is seen as early stage and underdeveloped. With a strong balance sheet, an investor can have confidence in its ability to execute on its long term vision.

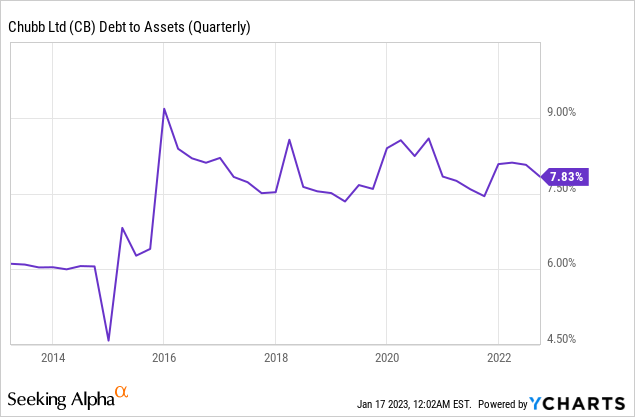

- Its Debt to Assets has always remained below 10% and currently stands at 7.83%

- Debt ($14 – $15B) and Interest on its debt ($1.4B) compares well to its cash flow from operations and EBIT (LTM – $7B)

Market Position

Chubb ranks third in Specialty Insurer category, first in High net-worth insurance, first in Multi-peril crop insurance and has greater than 90% retention rate in most of these categories in North America. Also, in the North American market alone it is expected to bring in about $33B in Gross Written premiums.

Overseas, it provides general insurance in about 51 countries and for the full year it is expected to bring in $13B in Gross written premiums. Although, it is not the market leader in any category here, it has shown significant growth in Europe Retail ( ↑ 47%), London Wholesale ( ↑ 75%), Latin America ( ↑ 21%) and Asia Pacific and Far East region ( ↑ 35%) from 2019.

Zooming specifically into Asia, it is spread across 15 countries, has 200 offices and 75k agents with very few brokers having comparable depth in Asia. With 40% of the world’s GDP but only 26% of the world insurance market, the company sees a big growth opportunity here and as such it will be attempting to deepen its Asia presence by increasing its ownership in Huatai to 82%. Regulatory approval is expected to close in the first quarter of 2023. As of 2021, Huatai brings in about $2B in revenue and has assets over $10B.

Profitability Position

Combined and Expense Ratios are the parameters used to measure profitability in the insurance industry. While combined ratio compares incurred losses and expenses to its earned premium, expense ratio compares only expenses (Acquiring, Underwriting etc.) to the net premiums earned by the company. In both instances, Chubb is better positioned than its peers and has been outperforming its peers for a significant period of time.

Company Website – Investor Presentation

Nature of Returns

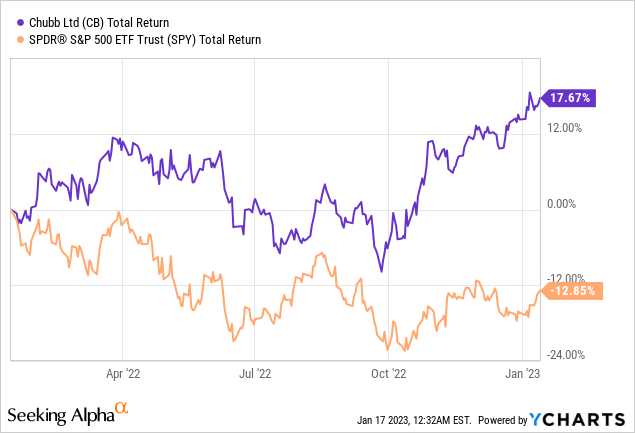

When I look at the price action of Chubb it is very evident that it provides returns less correlated to the overall market. It has a Beta value of 0.7 (lower the beta, the lesser it is affected by the market gyrations). I believe the nature of the industry (Insurance) Chubb operates in is a big contributor to its nature of return. Looking at the price action of the past five years Chubb has returned 73% compared to SPY’s 57%. Most of this outperformance came in the last year (18% vs -13%) which underscores our point that it’s returns could be more stable and steady than the overall market. This is important if your portfolio has a concentrated exposure easily affected by the market movements. In a rising market, returns from a high beta portfolio can easily be mistaken or attributed to one’s ingenuity but a punishing market will severely hamper the same portfolio. So it’s important to have a balanced portfolio and Chubb can potentially play a good role in bringing a balance to such portfolios.

Is This a Good Time to Get in?

Chubb is a mature company with a steady and predictable cash flow. Its cash flows are also less likely to be impacted by changes in the broader economy. So let’s try to answer this question by using levered Discounted Cash Flow Analysis.

Step I – Forecasting cash flows for the next five years, I have a used a growth rate of 5% increase in revenues from 2023 and a cash flow margin of 20% (much less than the average of the last five years)

Author Computed using Company Data

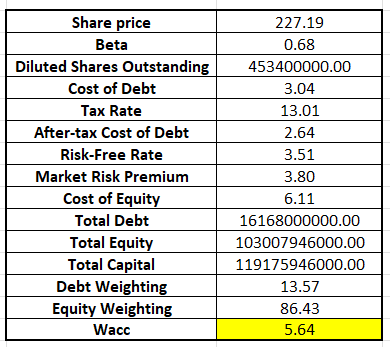

Step II – Next step is to find the Weighted average cost of capital. We are setting a value of 3.5% for our risk-free rate (current 10Y Treasury yield). Market Risk premium comes out to be 3.8% giving us (WACC) at 5.64%.

Author Computed using company data

Step III – Plugging this number (WACC) for our Free Cash Flow build-up gives us the sum of present value of the leveraged Free Cash Flow at $4.7B

Author computed using company data

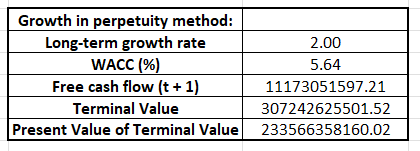

Step IV – Calculating the Terminal value using growth in perpetuity method with Long-term growth rate at 2% gives the present value of terminal value.

Author computed using company data

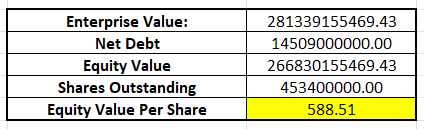

Step V – At the final step, we calculate the intrinsic value and compare this against the current market price. The gap (>50%) we observe indicates to us that this stock is undervalued and there is a very strong case for buying at these levels.

Author computed using company data

It goes without saying that DCF analysis can get subjective and a variety of factors can affect this valuation. A slower revenue growth assumption or a lower operating Cash flow (OCF margin) can bring down our intrinsic value. Lower operating cash flow can be a result of a low IRR project or a bad acquisition. Another important factor is the market risk premium. Higher market risk premium as a result of lower yields or higher stock market return could play a huge role in bringing down our intrinsic valuation.

From my trials, I discovered that when I moved OCF margin to <14% and also revised the market risk premium higher by 2 – 3%, the intrinsic value starts becoming comparable to the present stock price level. However, such a scenario looks extremely rare and hard to justify as of this moment so I will be sticking to my earlier analysis.

Risks

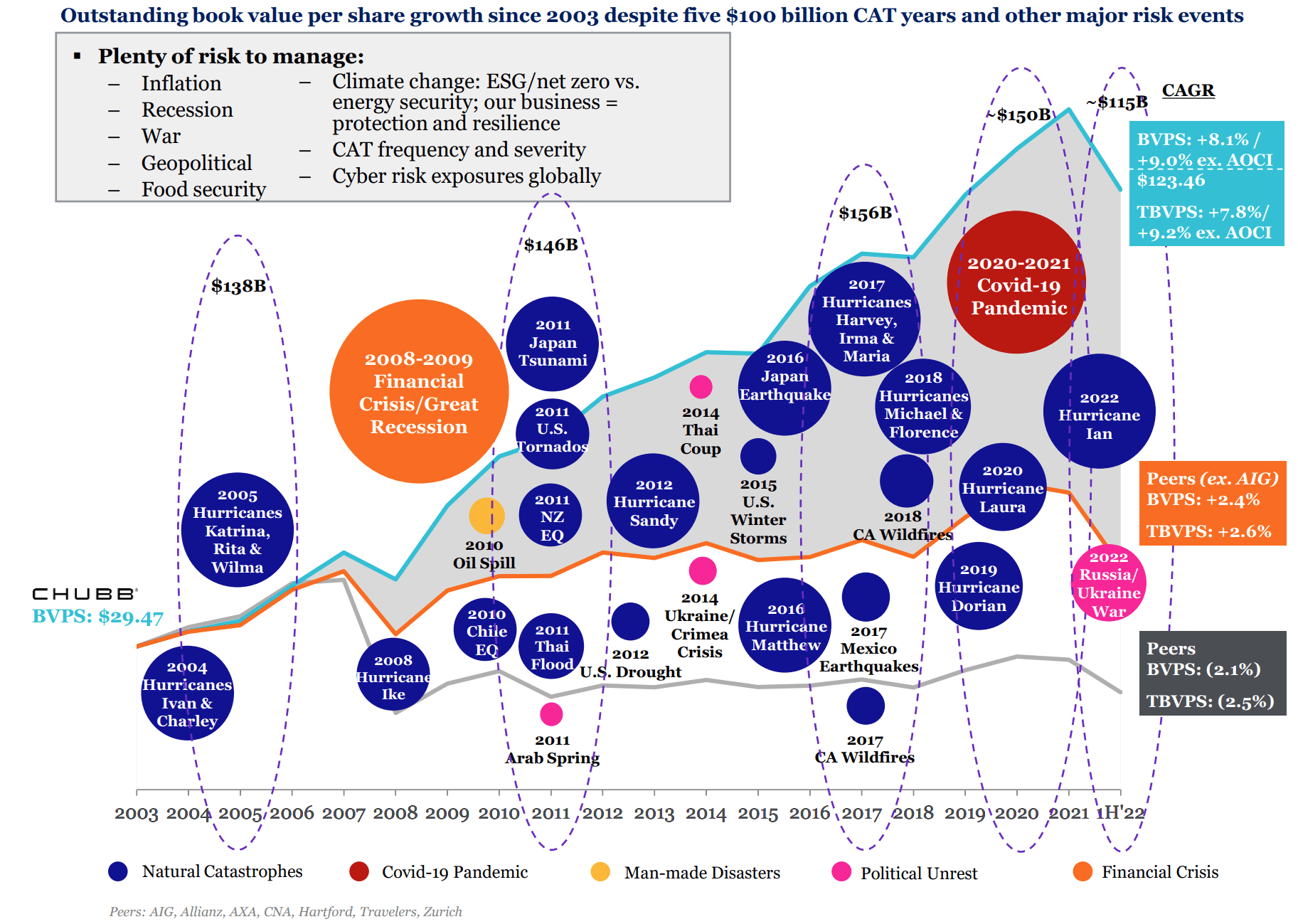

Chubb has done a tremendous job of handling typical risks faced by an insurance company. The last two decades have been quite eventful but Chubb has survived these events well and managed to grow its book value per share throughout these years.

Company Investor presentation

The one outstanding risk that would be unique to Chubb and also unprecedented in its history as a public company would be the company’s increased exposure to China. Initially seen as a growth opportunity, the sentiment has slowly been turning away from investing in China, and this is acknowledged by the company as a source of risk. At a time when companies are reducing their exposure to China, its decision to increase the exposure may prove to be unwise. In a worst-case scenario, the company may be forced to write off this investment.

Action

I will be initiating a small position in the company. If this stock sees a significant leg down, I will be examining to see if there is another opportunity to add to my position. In any instance, the total position would not exceed 5% of my portfolio.

Be the first to comment