bhofack2

Chipotle (NYSE:CMG) saw its stock dip 6% after reporting its close to the 2022 year. The company reported a disappointment in comparable sales growth but continued to nonetheless show margin expansion. Yet expectations remain high as they should for a stock trading at 50x earnings. The long-term thesis continues to center around the company’s ability to raise prices over the long term and the associated operating leverage that comes with that. While the high earnings multiple may not lend itself to feelings of a bargain, I still view the stock as being highly buyable here as the company appears to have a long growth runway ahead of it in the fast-casual space.

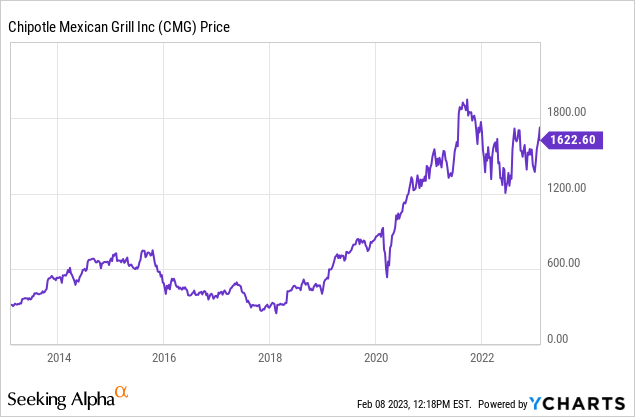

CMG Stock Price

CMG has recovered strongly since its e. coli outbreak in 2015, but has gone nowhere over the past couple of years.

I last covered the stock in April 2022 where I rated it a buy on account of its potential for operating leverage. The stock has since returned 13%, implying steep multiple contraction considering that the company grew earnings at a 40% clip over the past year.

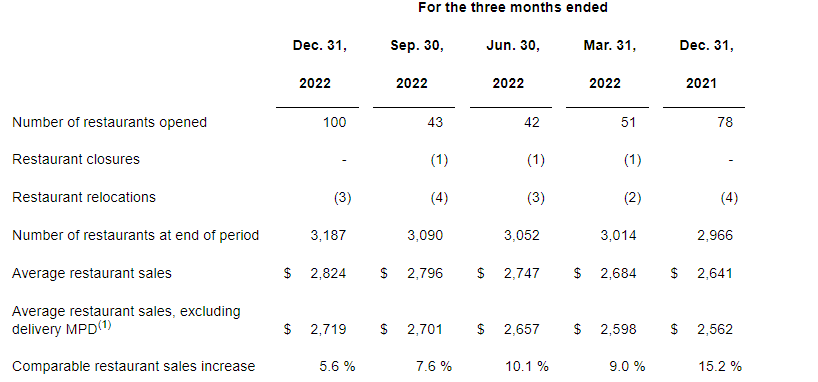

CMG Stock Key Metrics

The latest quarter saw the company deliver 11.2% total revenue growth, driven both by 236 new restaurant openings (100 new restaurants in the quarter) as well as 5.6% comparable sales growth. CMG had previously guided for comparable sales growth in the mid to high single digits, so that result probably explains the weak stock price action today. Restaurant level operating margins increased 380 bps to 24% and overall operating margin increased 550 bps to 13.6%. Adjusted earnings grew 48.6% to $8.29 per share.

2022 Q4 Release

The improvement in restaurant operating margin was attributed due to operating leverage as the company increased prices during the 2022 year. These results show that inflation can benefit restaurant stocks as they are sometimes able to offset rising food costs by passing on those costs to customers. The company noted that its rollout of garlic guajillo steak did not yield the anticipated return. As a big fan of their “ordinary” steak myself, perhaps that disappointment was not too surprising. Management also noted that they are seeing increased productivity in large part due to their “Chipotlanes” drive-thru capabilities. Management believes that restaurants with drive-thru lanes have 1,500 bps greater productivity than those without upon opening.

The company ended the quarter with $1.3 billion in cash and no debt. The company repurchased $198.9 million of stock in the quarter and the Board of Directors increased that authorization by an additional $200 million ($413.9 million was available as of the end of the quarter).

Looking ahead, CMG is guiding for comparable sales growth in the high single-digits in the first quarter with 255 to 285 new restaurant openings for the full year. That outlook is squarely in-line with their medium term guidance for 8% to 10% new restaurant openings per year.

On the conference call, management noted that comps may “moderate” in the second and third quarters due to lapping their menu price increases. Between that and a recession, it’s plausible for 2023 to see slower earnings growth than that seen in 2022.

Is CMG Stock A Buy, Sell, or Hold?

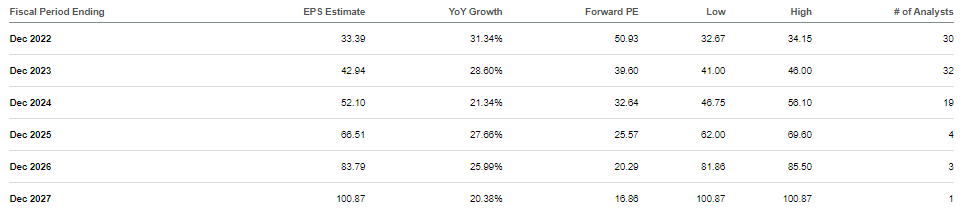

CMG stock might not look obviously cheap at first glance. The stock trades at 50x trailing earnings with fast growth expected over coming years.

Seeking Alpha

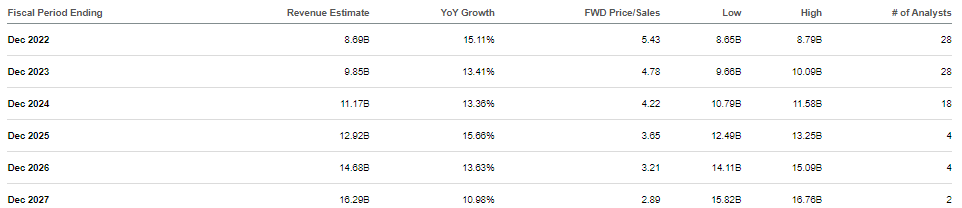

That earnings growth is expected to be driven by low double-digit top line growth.

Seeking Alpha

What’s going on? Why does CMG trade at 2x the multiple of McDonald’s (MCD)? The answer lies in operating leverage. Any loyal CMG customer can likely agree that the restaurant offers great value as compared to alternatives. That feeling doesn’t just make customers feel good but is also a driver of the long term thesis. Consider that if CMG were to raise prices by 10%, then net income could double (based on 2022 numbers). Yet I could see prices rise by 50% based on today’s standards and still being competitive. So one way to look at the stock is that it’s trading at around 25x earnings (assuming a 10% price increase) while the company continues to both expand its store base by 8% to 10% annually and take market share. Even without annual price increases, the company can generate double-digit earnings growth that comes close to justifying the sticker 50x earnings multiple.

I can see the company sustaining around 24% forward growth from store openings, market share gains, and annual price increases in-line with inflation. Based on a 1.5x price to earnings growth ratio (‘PEG ratio’), the stock might trade at 36x earnings. That implies 44% potential upside (assuming that aforementioned 10% price increase) for the stock over the next 12 months.

What are the key risks? For starters, that valuation model is heavily forward looking, not too dissimilar with how I might value tech stocks. Considering that tech stocks have seen a steep valuation reset over the past couple of years, it’s possible that CMG is due for its own correction. Perhaps the GAAP profits can help provide some sort of valuation support, but I note that even highly profitable tech stocks like Meta Platforms (META) and Alphabet (GOOG) (GOOGL) have seen steep multiple contraction. Another risk is that of changing consumer tastes. Chipotle is popular right now but might not be popular in the future. There are admittedly not a lot of long-running food chains that remain extremely popular today. With MCD trading at around 25x earnings, there may be some valuation support in such a scenario, but the long-term growth trajectory may prove more modest than expected. If one can get comfortable with the operating leverage exercise, then CMG looks highly buyable here as it continues to prove itself as a long term compounder.

Be the first to comment