Spencer Platt

Written by Nick Ackerman. This article was originally published to members of Cash Builder Opportunities on January 25th, 2023.

Earnings season is upon us, and things haven’t been overly rosy. One statistic shows us that so far, for the S&P 500 companies that have reported as of January 25th, only 68% of them have been beating earnings. Generally, the fourth quarter had an average beat rate of 79%.

Additionally, most CEOs have noted some caution going forward, with weaker-than-expected guidance in several popular names. We’ve also been seeing plenty of headlines about laying off employees, which all suggest CEOs aren’t just talking about a weak outlook, but they certainly believe it as they look to get leaner.

At the same time, if everyone expects a recession, a CEO can’t necessarily come out and be overly optimistic, either. It is okay if a CEO is wrong about being pessimistic and economic pain never comes to fruition, or it isn’t as bad as initially thought.

All this being said, the sky doesn’t appear to be falling, and we are still getting more earnings beats than misses. Earnings haven’t been rosy, but they also aren’t the worst. As a longer-term investor, I tend to be more biased towards expecting better news will come eventually. At least historically, we’ve made it through every bear market so far.

I believe touching on the overall market picture and economy is important when talking about BlackRock (NYSE:BLK). BLK isn’t a market index, but it may as well be due to the significant impact the actual performance of stocks and bonds have on the name.

Earnings Review

Their last earnings were fairly strong, with an earnings beat on both the top and bottom lines.

Albeit, year-over-year revenue fell 15.1%, but that’s directly related to AUM declining from asset prices. However, for the entire year, we see revenue came in at $17.873 billion compared to $19.374 billion. That works out to only around an 8% decrease.

EPS of $48.93 for Q4 was a decline of 16% from the $10.68 announced in Q4 of the prior year. For the fiscal year, EPS came to $35.36 compared to $40.51 in the full year 2021. That worked out to a 13% decline.

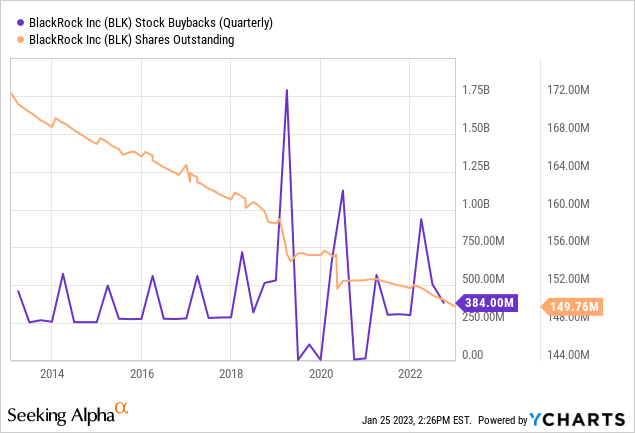

BLK has a strong history of buybacks, which can help boost earnings even if the underlying market is cooperating. In this case, they’ve been reducing shares for years now. They only stopped buybacks in 2020 when the economic outlook was truly uncertain.

Ycharts

Here is what they had to say about buybacks in their latest earnings.

We also remain committed to systematically returning excess cash to shareholders through a combination of dividends and share repurchases and returned a record $4.9 billion to shareholders in 2022, including $1.9 billion of share repurchases, an increase of over 30% from 2021.

Since inception of our current capital management strategy in 2013, we have now repurchased over $13 billion of BlackRock’s stock, reducing our total outstanding total shares by 13% and generating an unlevered compound annual return of approximately 15% for our shareholders.

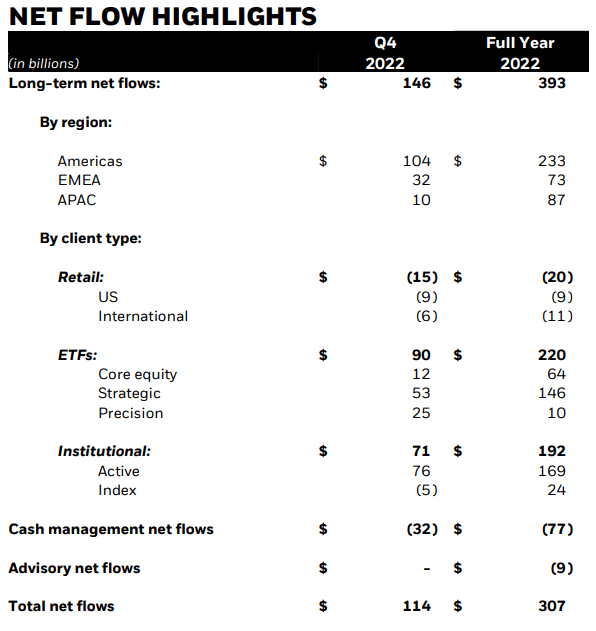

Despite the rough waters of 2022’s market, they still accumulated $146 billion in quarterly long-term net inflows. When looking at the net outflows of cash management, it was a total net inflow of $114 billion for the quarter alone. Those sorts of inflows can help soften the woes of the underlying decline in asset prices.

For Q4, BLK experienced a change of $374.183 billion due to the underlying market. For the year, it worked out to a decline of nearly $1.502 trillion. They had previously topped $10 trillion in AUM.

For the entirety of 2022, they raked in $300 billion. $230 billion of long-term net inflows from the United States alone. That’s despite several states announcing that they would be pulling pensions and state investments from this asset management behemoth. As we can see, that had almost no impact. $3 or $4 billion against total assets of nearly $8.6 trillion isn’t going to change the outlook.

Overall, the retail client type showed only outflows, while institutional index investments also showed a slight outflow in the latest quarter. For the entire year, the only outflows were under the retail client type. That includes both U.S. and international client types. However, that was more than offset by the ETF and institutional clients.

BLK Inflows/Outflows (BlackRock)

They continue to cite the pressure in the industry for retail clients being a shift out of actively managed fixed income and world allocation strategies. This is what they had to note in their earnings call.

Full year retail net outflows of $20 billion reflected ongoing industry pressures in active fixed income and world allocation strategies partially offset by strength in index SMAs and our systematic equity income and multi-strategy alternative funds. Fourth quarter retail net outflows of $15 billion reflected similar trends.

Performance Of Shares And Looking Forward

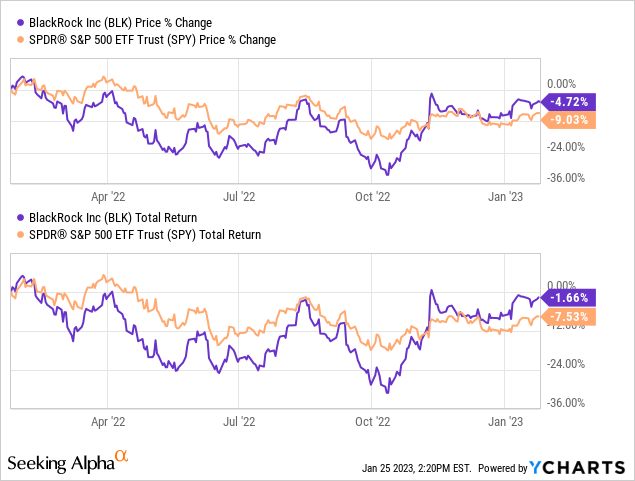

Interestingly, when things were looking direr, BLK was performing much worse than (SPY) in the last year. However, when things started to turn around, BLK started leaping ahead of the overall equity market.

Ycharts

One thing that the company can benefit from is the inflows experienced. This can act as a spring when the overall market starts to turn. Whether that be in the equity or bond market, as we’ve seen, they’ve experienced inflows across their ETFs and institutional investments.

With more assets accumulated in these investment vehicles, it can give a boost on the way up. That’s why over shorter periods of time, market volatility can impact BLK negatively, but over the longer run, inflows play such an important role.

It essentially can work in a reverse way when an ETF or closed-end fund has to deleverage. The downside move is amplified, so a higher move will be needed to recover to previous levels. However, it becomes much more difficult with a reduced asset base after deleveraging. Thinking about sequence of return risk is another similar scenario to what can play out if you think about BLK’s underlying fee-generating assets as one giant portfolio.

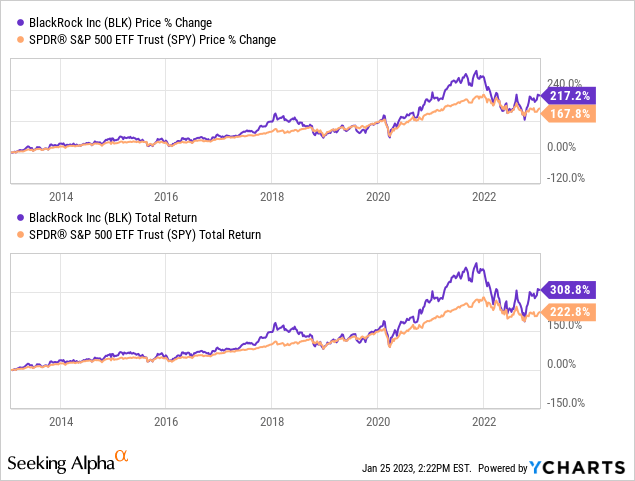

Over the long term, BLK has put up superior total return results compared to the S&P 500. Here is a look at the last ten years on a price change and total return basis. The total return would factor in the dividends that each of these entities paid, and it assumes reinvestment. 2022 was a rare year where not only equities were down, but also fixed-income securities were down along with them as interest rates blasted higher.

Ycharts

Despite the doom and gloom, looking forward, analysts seem to be fairly optimistic as they are anticipating earnings only to take a slight decline this year. From here, they then anticipate that earnings will start rising rapidly once again.

BLK EPS Estimates (Seeking Alpha)

Given an EPS surprise for 14 out of the last 16 quarters, it wouldn’t be overly surprising to see EPS come in better than expected. The revenue estimate beats aren’t as strong, but they still come in, beating 10 out of the last 16 quarters.

Valuation

Any sort of positive moves in the underlying market would only propel the outlook for BLK. Of course, the caveat is that the reverse of this is also true; with any return to a bear market or new lows, the outlook for BLK could diminish.

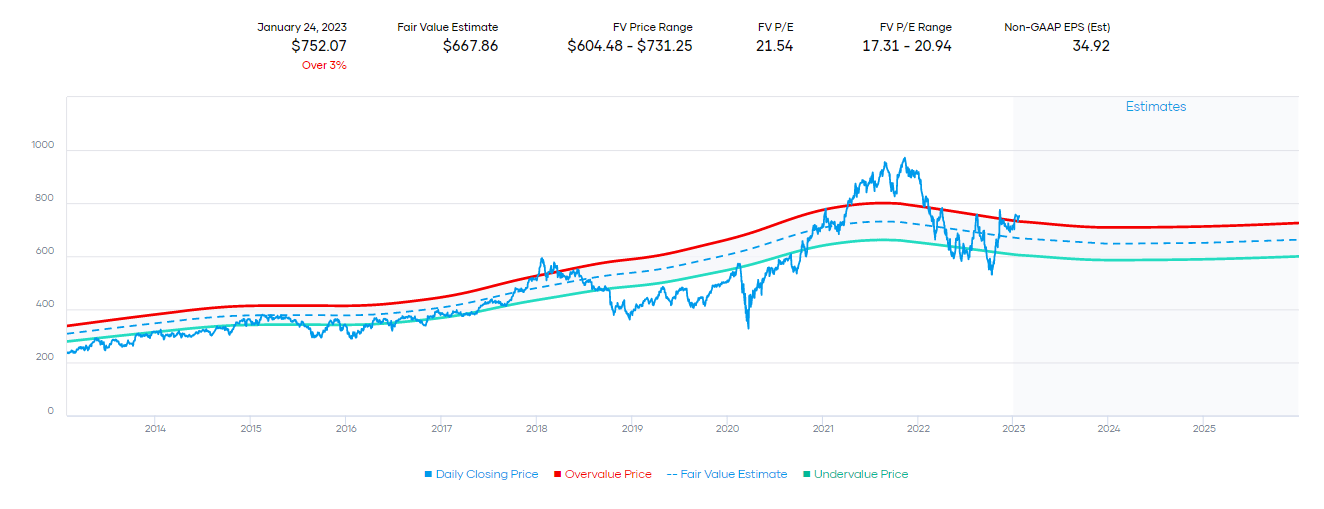

At this time, the S&P 500 index shows that the P/E ratio is around 21. Perhaps unsurprisingly, that’s pretty much right where BLK is trading as well. Historically, the average P/E for BLK in the last ten years shows a fair value range of 17.31x to 20.94x. That means that we are currently trading in an overvalued range.

That would suggest that the market is pricing in a fairly optimistic view of BLK shares at the current time, meaning that if we don’t see better-than-expected moves from here, we could see shares of BLK decline. It might not be a terrible time for a long-term investor to consider investing in BLK. For a more patient investor, though, it would suggest that we might see a better entry point.

BLK Fair Value Estimate P/E Range (Portfolio Insight)

Wall St. analysts are more optimistic. They assign an average price target of $807.

Dividend

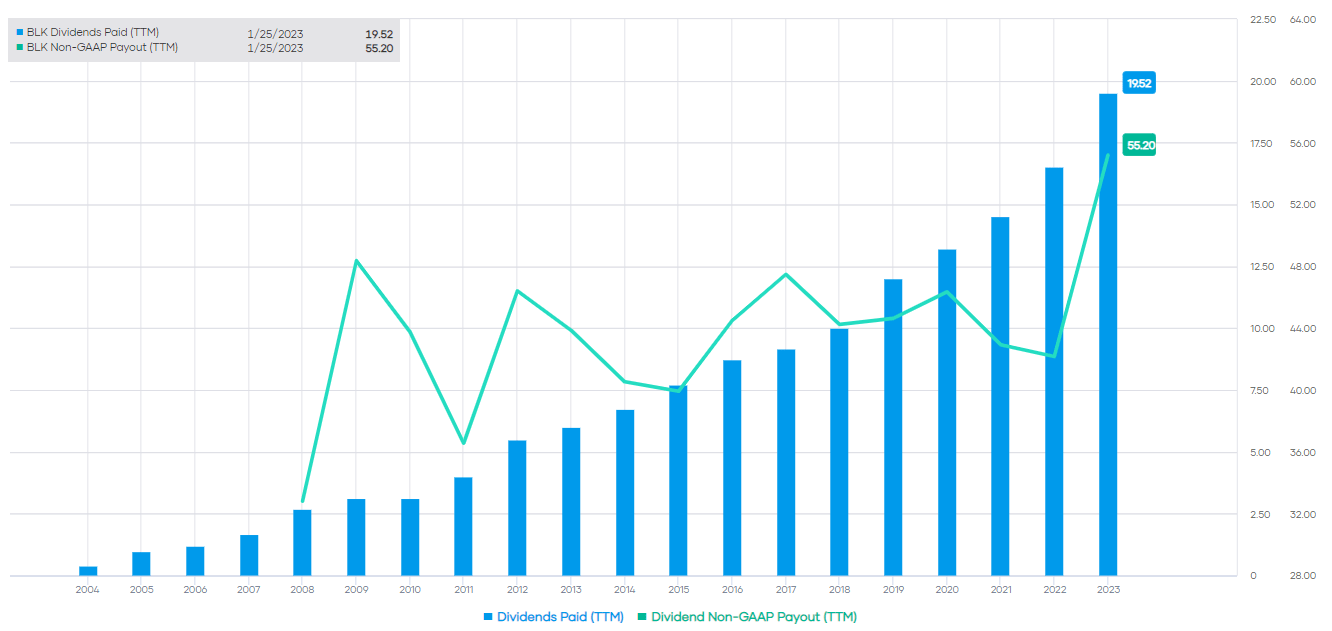

BLK has been raising its dividend for 13 consecutive years. They’ve been paying out a dividend for even longer. The consecutive annual raises would have been longer, but a pause in 2009/10 (for obvious reasons) halted the streak of raises.

BLK Dividend And Non-GAAP Payout Ratio (Portfolio Insight)

While the payout ratio has jumped up quite meaningfully, we are nowhere near any sort of danger zone.

However, this has also meant that the latest dividend increase has been one of the smallest we’ve seen. Certainly not unexpected, given the current environment and not something that I would get too worked up about.

The increase was a 2.5% increase to $5 per quarter. That gives us an annualized $20 against the estimated $34.92 EPS resulting in a forward payout ratio of 57.27%. That is quite a comfortable level, in my opinion, until earnings can start heading back in the upward direction.

Conclusion

Shares of BLK have been recovering along with most assets lately, as expected. While showing a decline, the latest earnings weren’t as bad as they could have been given the overall move in assets over the last year. That includes both equities and fixed-income broadly falling. That being said, 2023 could be a difficult year. On top of this, shares of BLK are trading at a historically elevated level. Meaning that investors are actually pricing in a more rosy outlook, in my opinion.

It might not be the worst time for a long-term investor to buy with many years ahead of them. However, for a more patient investor, waiting for a potential pullback isn’t a bad strategy either. At this time, there are certainly still attractive names that are showing to be relatively undervalued.

Be the first to comment