StockByM

Chimera Investment (NYSE:CIM) went public less than a year before the 2008 financial crisis went into full swing. The internally managed mortgage REIT would start trading on the NYSE in November 2007, ten months before Lehman Brothers collapsed and Merrill Lynch, who underwrote its IPO, was acquired.

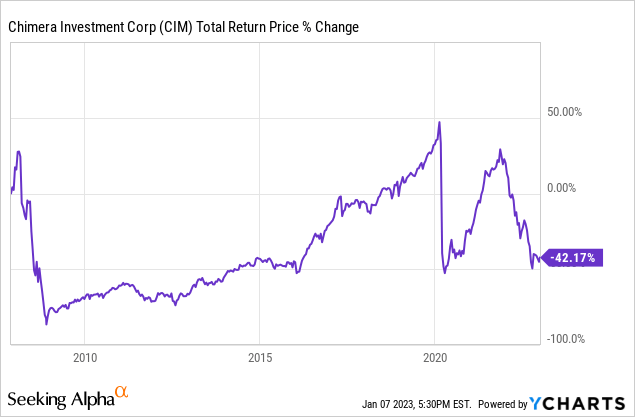

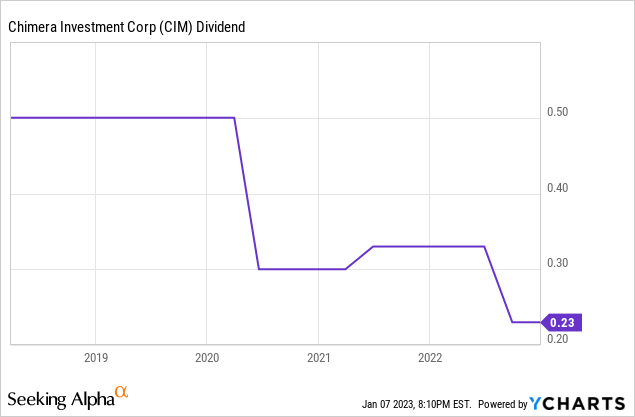

Hence, in many ways, Chimera’s current crisis of confidence has happened before. The mREIT is currently down 58.5% over the last 12 months, 52.16% when you include dividends for its worst drawdown, excluding the flash pandemic meltdown, since the 2008 crisis. It’s not hard to see why as the US and global economy face still salient economic issues that have disrupted and will continue to pose intense headwinds to the market for residential mortgage loans and mortgage-backed securities. Chimera has already had to pare back its dividend payout from the prior 5-year peak of $0.50 per share. The risk here is that more cuts are coming.

New York-based Chimera is a hybrid mortgage REIT because it invests in non-agency and agency residential mortgage-backed securities, agency commercial mortgage-backed securities, and residential mortgage loans. Agency RMBS are securities backed by a pool of mortgages issued by government-sponsored agencies like Fannie Mae, Ginnie Mae and Freddie Mac. These are typically lower risk than non-agency RMBS with cash flows derived from mortgage payments paid to the owners of the RMBS.

A Case Of Deja Vu As Housing Comes Under Pressure

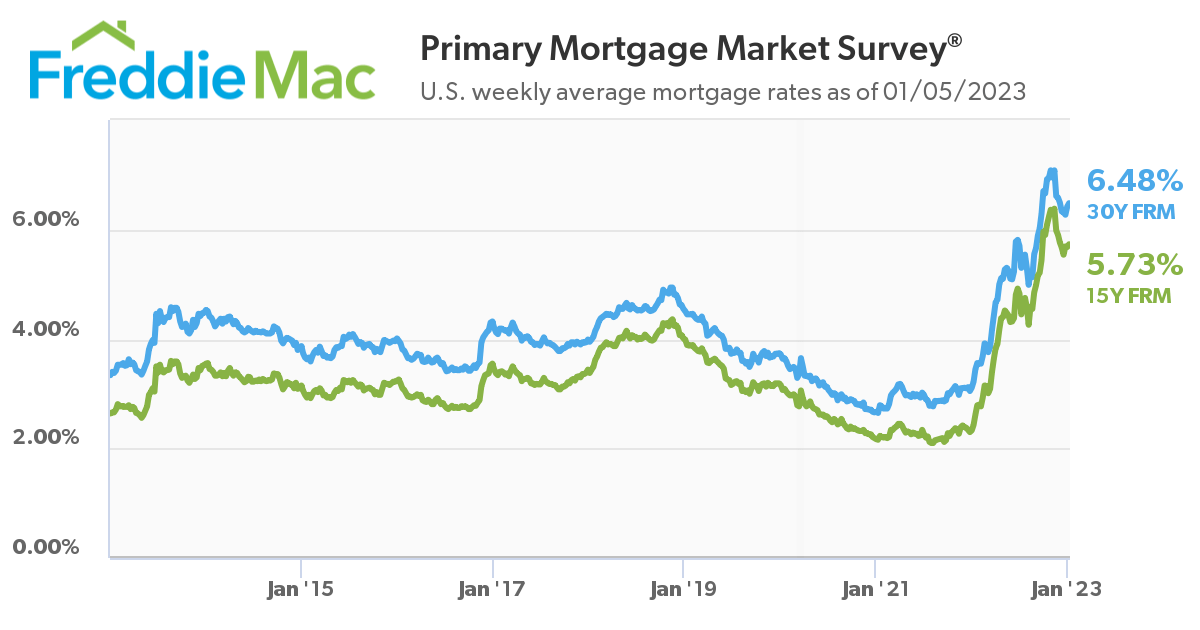

Chimera last declared a quarterly per-share dividend of $0.23, in line with the prior payout, for a yield of 14.6%. The risk here is that the dividend is cut back markedly against a housing market under intense pressure from a brutally hawkish Fed set on seeing through its strategy to get inflation back to its 2% target. The 30-year fixed-rate mortgage rate has spiked to a more than decade-long high and the cost of services mortgages has more than tripled from its 2021 lows.

Freddie Mac

Mortgages now face the dual pressure of rising rates and what looks to be the onset of a recession. Real estate purchases are slowing down and US house prices are forecasted to fall by up to 20% this year. Indeed, investor homes purchases fell by 30% year-over-year nationwide in the third quarter of 2022, the most significant decline since the 2008 financial crisis. And a recent Bloomberg survey of economists in December put the chance of a recession this year at 70% with the Fed fund rates expected to increase to between 5% to 5.25% next year, a 17-year high.

The macroeconomic backdrop is dire, and Chimera’s already lowered dividend is at risk. The mREIT last reported earnings for its fiscal 2022 third quarter, this saw net interest income come in at $104.84 million, a significant decline of 29.7% over the year-ago quarter and a miss by $5.72 million on consensus estimates.

Chimera Investment Corporation

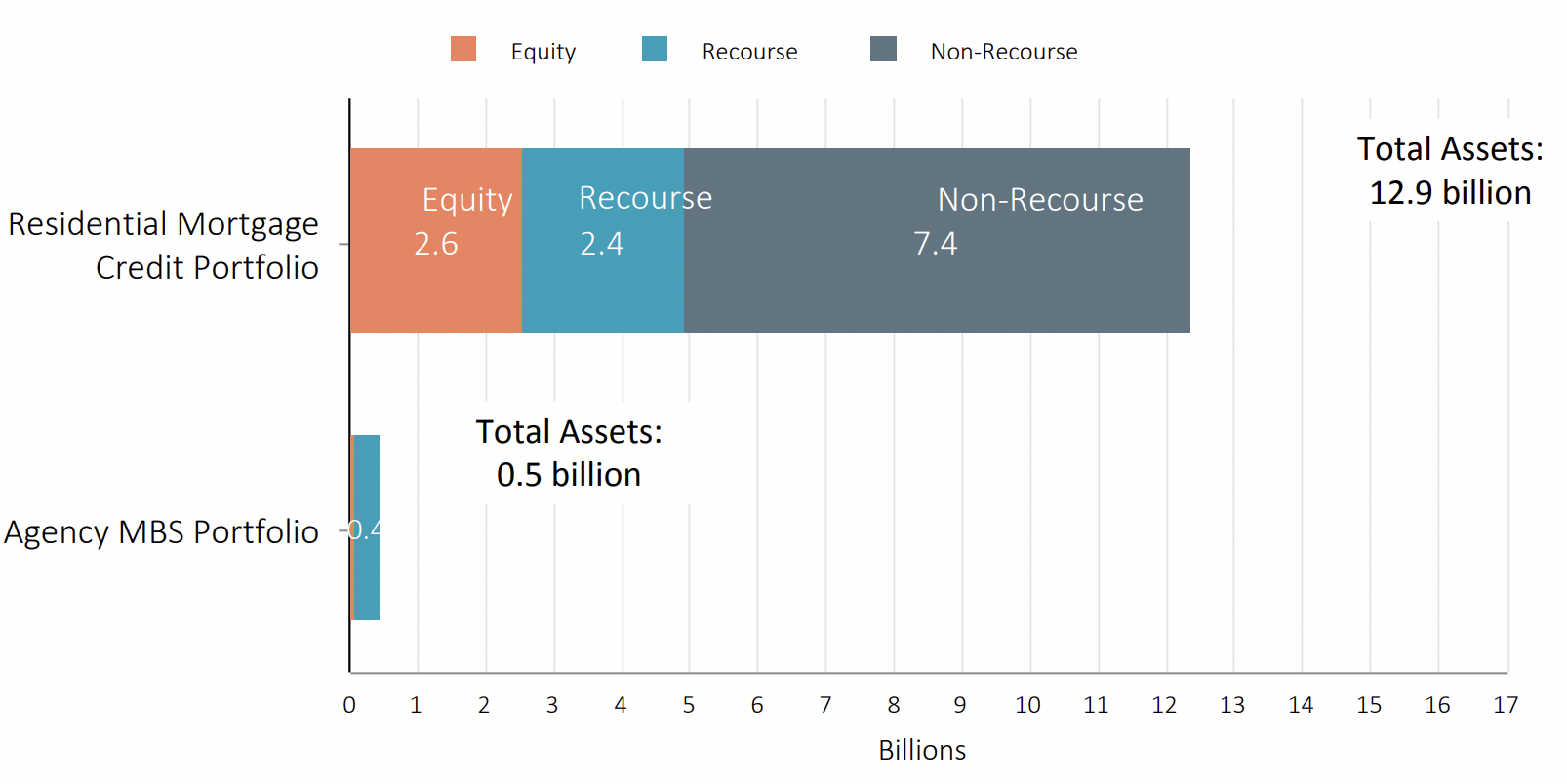

The total portfolio stood at $13.4 billion as of the end of the third quarter, which drove a GAAP book value of $7.44 per share, down 15.6% from $8.82 per share from the prior second quarter. The earnings call shed more light on the continued negative impact the rising Fed fund rate is having. Book value has declined by 2% to 3% since the third quarter’s end.

Chimera is now on the defensive, the mREIT increased its cash position during the third quarter to $350 million and has moved to hedge its overall exposure to variable rate financing with $1.1 billion of fixed interest rate swaps executed during the period. This meant cash available for distribution came in at $0.27 per diluted share, down from $0.42 in the year-ago period but matching consensus estimates.

Hedging Downside Risk With The Preferreds

Whilst the quarterly payout to common shareholders is currently covered by cash available for distribution, this available cash has fallen by 35.7% over its year-ago comp. The decline of book value has also continued post-period end just as three further 25 basis point hikes look to be on the Fed’s roadmap for fighting inflation year. Hence, there will be even more pressure on the company’s book value.

Prospective investors might want to consider Chimera’s 8.00% Series B Fixed to Floating Rate Cumulative Redeemable Preferred Stock (NYSE:CIM.PB).

QuantumOnline

The preferreds currently pay a coupon of $2 which works to be a 9.4% yield against the current price preferreds. Further, at $21.88, these are trading 12.5% below their $25 redemption value. This is future potential capital upside on top of the current yield with shareholders having up until March 2024 until Chimera is allowed to redeem the preferreds.

However, it is unlikely they’ll be a redemption event at this date due to the current high cost of capital and the pressures already being exerted on the company’s net interest income. To be clear, the preferreds offer a 9.4% yield and a 12.5% upside potential. They are also cumulative which reduces the likelihood of a suspension. The floating rate mechanism will see the annual coupon rate be more volatile with a move to three-month LIBOR plus a 5.791% spread at the call date. Fundamentally, whilst the commons look set for more pain, the preferreds offer a good income hedge.

Be the first to comment