Whenever I buy a stock for my dividend growth portfolio, I make sure that it’s a company that I wouldn’t mind holding if I weren’t allowed to touch my portfolio for at least a few decades. While I’m passionate about every single company I own, I own a few that I simply don’t check on a regular basis. The Chevron Corporation (NYSE:CVX) is becoming one of these companies. It’s one of my highest-yielding investments and one of three energy dividend stocks.

Author

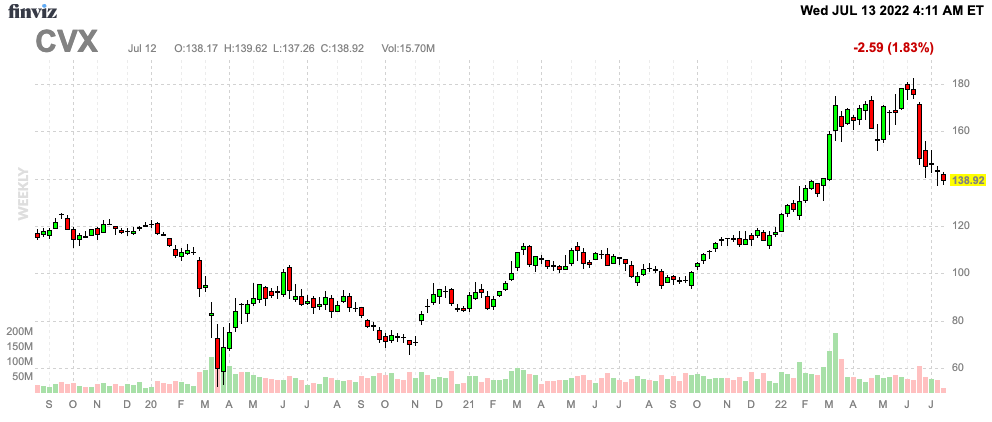

In September of 2021, I wrote my most recent (and only CVX) article covering the long-term oil outlook. Now, this bull case has gone into overdrive as higher demand is hitting significant supply issues. Yet, updating this bull case is not the only reason why I’m writing this article. Growth fears have caused CVX to lose a quarter of its value in recent weeks, which pushed the dividend yield back above 4.0%.

FINIVZ

In this article, I will:

Explain why I remain long-term bullish on oil prices

Dive into the outperformance of value stocks

Discuss why Chevron lets me sleep well at night

So, without further ado, let’s get to it.

The Oil Bull Case

I may be wrong, but I believe that energy has become my most-discussed macro topic in recent months. The energy industry (unfortunately) is one of the best examples of supply constraints.

On July 7, I wrote an article titled “Devon Energy: A 10% Yielding Beauty Thanks To Political Efforts”.

In that article, I discussed the oil industry from a supply point of view.

Basically, what we’re dealing with is a scenario where post-recession oil supply growth is not as strong as it was in prior cycles.

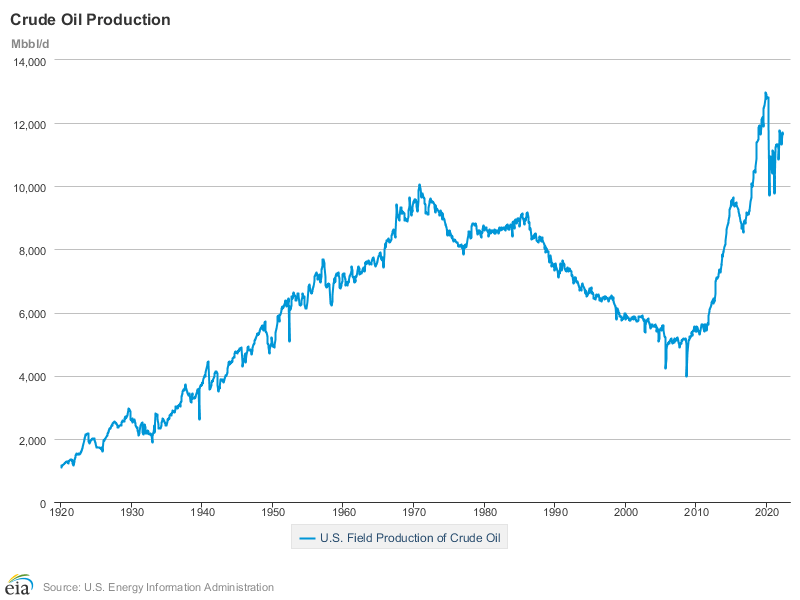

EIA

The shale revolution that started after the Great Financial Crisis has caused the US to boost crude oil production from roughly 5 million barrels per day to currently almost 12 million daily barrels.

In 2016, energy companies boosted production even more as low oil prices and weak demand did a number on their balance sheets. Higher production allowed them to make more money to lower debt again. It caused production to spike again.

In 2020, demand imploded as countries around the globe implemented lockdown orders to deal with what was a novel virus back then.

Then, something changed as I wrote in my Devon Energy (DVN) article. Production didn’t rise anymore. At least not as fast.

Production is now roughly where it was one year ago and well below peak levels close to 13 million barrels per day.

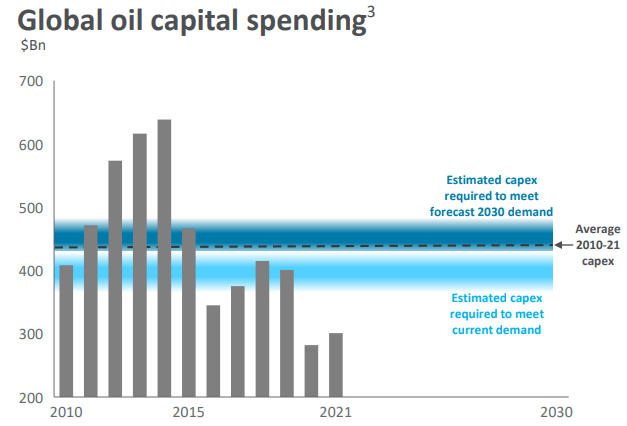

As the chart below shows, global oil capital expenditures have gradually been reduced. Prior to the 2014 oil crash (when Venezuela was still a rich country), global oil CapEx was close to $650 billion. This imploded when a lot of offshore projects became unprofitable. The surge in CapEx between 2016 and 2018 was mainly caused by US onshore drillers. Then, the pandemic caused another major decline to less than $300 billion. This is now expected to remain the base case. Needless to say, the global hunger for oil remains high and further rising. In order to satisfy 2030 demand, global oil CapEx is estimated to require at least $450 billion annually.

Seeking Alpha

The unwillingness to invest in growth is based on a number of reasons. However, the biggest reason is the global transition to renewable energy. The Paris Agreement and various initiatives to become carbon neutral have made oil and gas companies the “bad guys”.

This trend is fueled by a political desire to push for renewables as I wrote in a recent Marathon Oil (MRO) article.

The New York Post – among many others – reported that National Economic Council director Brian Deese (Biden’s personal advisor) had a somewhat unexpected answer to the following question asked by CNN:

“What do you say to those families who say, ‘Listen, we can’t afford to pay $4.85 a gallon for months, if not years. This is just not sustainable’?”

He answered:

“What you heard from the president today was a clear articulation of the stakes,” Deese answered. “This is about the future of the liberal world order and we have to stand firm.”

This is not only interesting because it’s stuff you usually read on conspiracy theory websites, but it perfectly confirms what we’re currently dealing with on a global basis: the refusal to boost fossil fuel production for the sake of the environment.

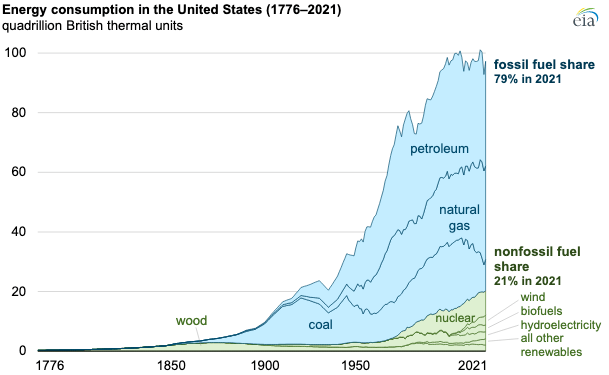

Personally, I’m not pushing for any political party. What matters to me is that the energy transition needs to be more gradual. After all, in the US, fossil fuels still account for 79% of the total energy supply. Causing inflation in fossil fuels quickly works its way through the entire economy.

EIA

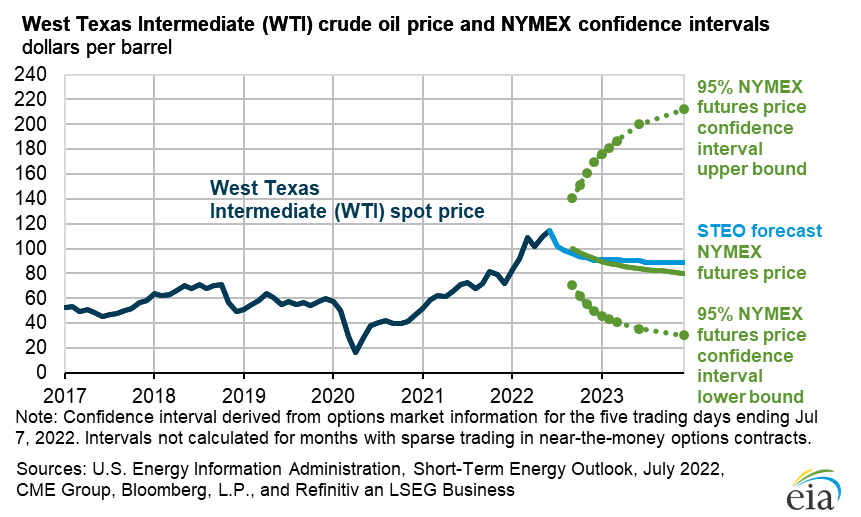

The latest EIA energy outlook shows that oil is likely to remain above $80 WTI for at least 1.5 more years. I agree with that and wouldn’t bet against long-term prices above $100 if demand remains strong in the years ahead.

EIA

Now, before I address Chevron, let’s take a quick detour to discuss value stocks.

Value Outperformance

On June 26, the Wall Street Journal wrote an article highlighting the outperformance of value stocks. Value stocks beat growth stocks by the widest margin since 2001.

The paper mentioned high inflation as a driver of outperformance. This makes sense as it makes companies with earnings more attractive than companies that are expected to make money somewhere in the future (high inflation makes discounting future growth less attractive):

Among the stocks at the top of the leaderboard are traditionally slower-growing businesses like Exxon Mobil Corp., Merck & Co. and Molson Coors Beverage Co. All have notched double-digit gains in 2022, while the S&P 500 has dropped 18%. The big technology stocks that propelled the market’s gains for much of the past decade, meanwhile, have fallen as the Federal Reserve raises interest rates in a bid to tame high inflation.

Mr. Asness, managing and founding principal at AQR Capital Management, and Mr. Arnott, founder and chairman of Research Affiliates, say value stocks are still unusually cheap in comparison with growth, despite their recent run.

“People like me, both for legal and for honesty reasons, should never use the word guarantee, and I won’t,” Mr. Asness said in a recent interview. “But I’ve never been more excited about value.”

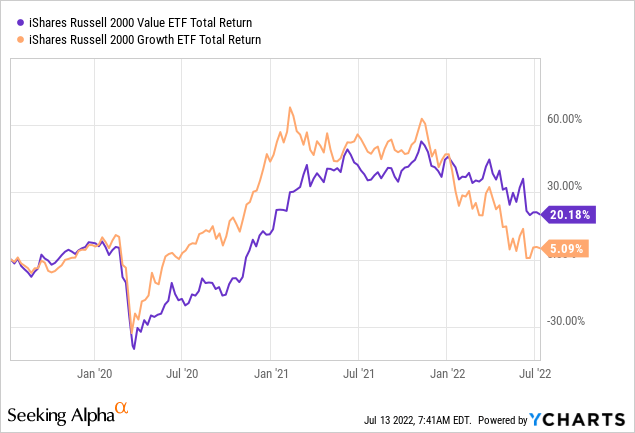

Over the past three years, we witness that value is outperforming growth by 15 points. In this case, I’m using Russell 2000 stocks. Yet, in general, it’s fair to say that value is doing better.

Data by YCharts

This week, Wall Street Journal published another article highlighting the strong performance of dividend stocks. Again, this makes sense as paying a dividend is a core quality of a value company.

The outperformance of dividend stocks highlights the market rotation of 2022. For the past decade, mega-cap technology shares and stocks with high valuations led the major indexes higher. This year, rising rates and hot inflation turned the market upside down, with investors ditching highflying companies for overlooked stocks like dividend-payers that offer greater stability. Dividends finished the first half as the only investment factor with a positive return, according to a Bank of America analysis.

Companies paying out a slice of their earnings to shareholders typically have a record of strong profits, an appealing trait as investors worry elevated costs and strapped consumers could dent corporate results. These companies also tend to be in industries like utilities, telecommunications and consumer staples, which consumers rely on regardless of the economic environment.

Now, it’s expected that dividend growth will become more muted as economic growth is slowing. The good news for income-oriented investors is that this means companies start by dialing back buybacks first. If that’s not enough, the dividend may slow as the last step a company will take is reducing its dividend as that is often a sign of weakness. Cutting a dividend is like admitting that one has serious issues. It scares away investors and it’s just a bad look on any company.

The chart below (modified by me) confirms these expectations. Below, we’re looking at S&P 500 dividend futures. These futures show expected S&P 500 dividends per year. For example, in April, expectations were that the 2025 dividend would be close to $63. The 2031 dividend was expected to be $70.

Now, the entire curve has moved lower as the market doesn’t expect any dividend hikes until 2029.

CME Group (Modified by the author)

With that said, these futures are volatile and prone to big moves. This by no means indicates that dividend growth will be flat for almost a decade.

What I get from this is a confirmation that investors are cautious. The big dividend hikes may be over. This happens in an above-average inflationary environment.

In other words, buying quality dividend income is key.

Now, this is where I combine the first two parts of this article (oil & dividends) as Chevron is delivering what investors are looking for.

Chevron’s High-Quality Dividends

Like Exxon Mobil (XOM), which I own as well, we’re dealing with a well-integrated oil company engaged in upstream, midstream (minor operations), and downstream operations (drilling, transporting, and selling it).

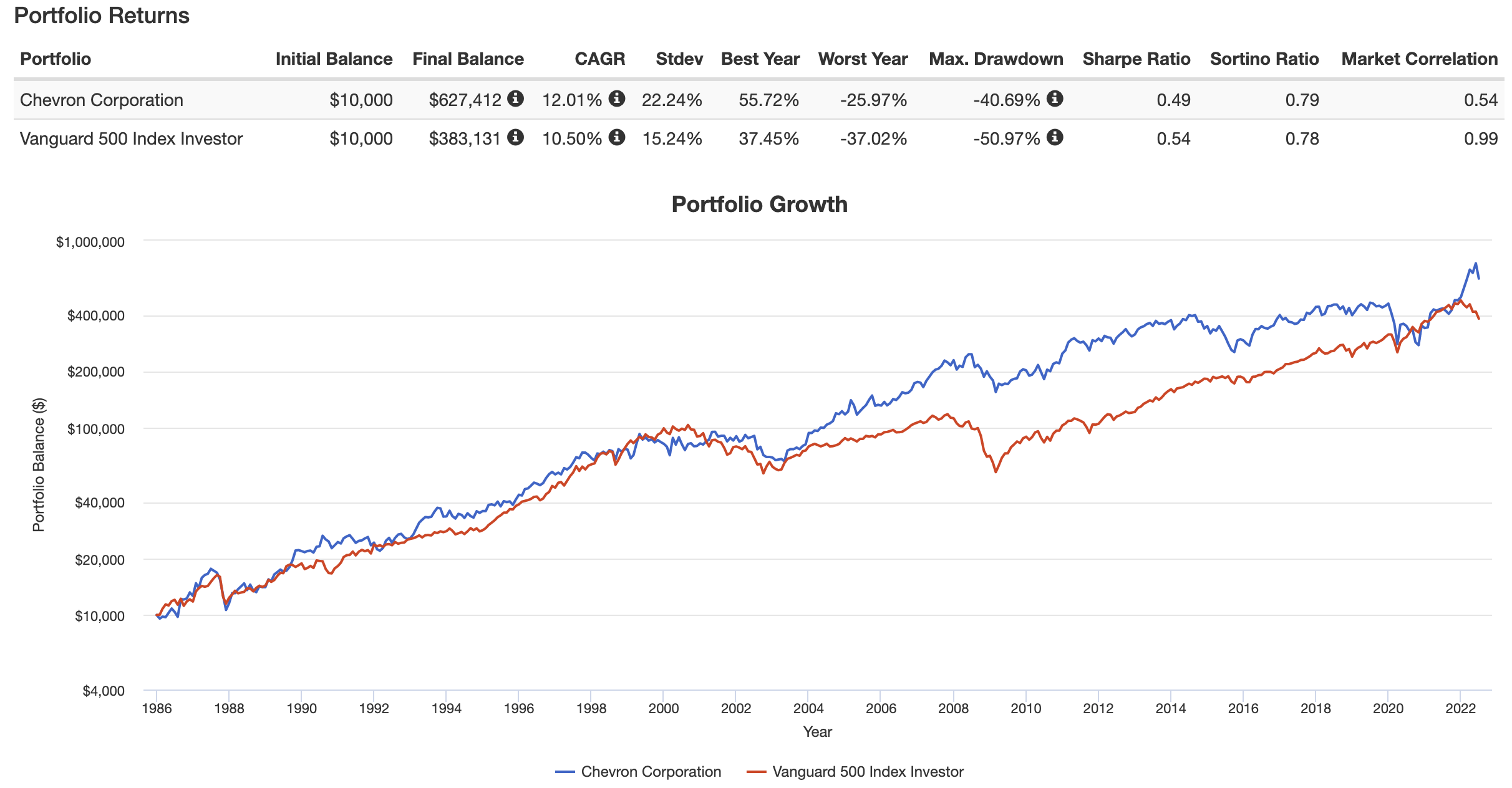

Since 1985, Chevron has returned 12.0% per year, beating the S&P 500 by roughly 150 basis points. The standard deviation was just 22.2%, which allowed the company to keep up with the S&P 50 on a volatility-adjusted basis as well (Sharpe/Sortino ratios).

Portfolio Visualizer

Since 2010, CVX has returned 9.5% per year, underperforming the S&P 500 by 280 basis points. The standard deviation was 24.6% during this period.

The underperformance is no surprise as almost the entire 2010-2022 period saw subdued inflation, which benefited tech/growth over boring “big oil” and related commodity-focused companies.

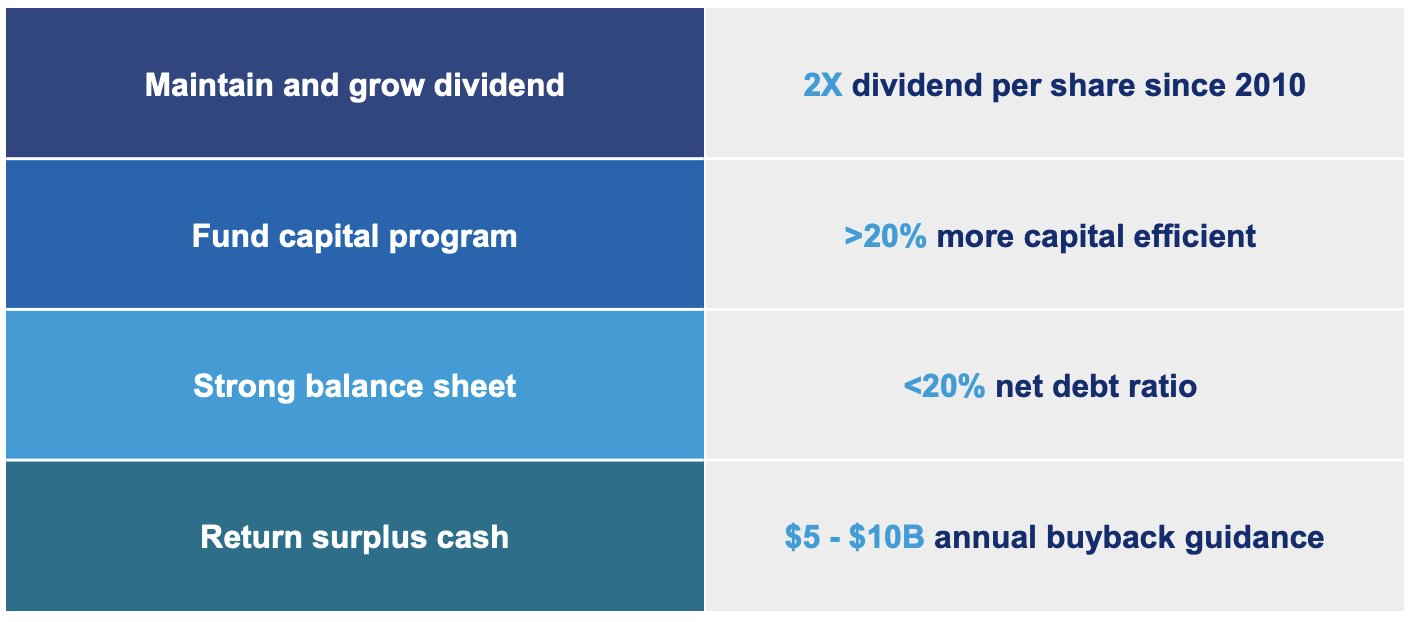

What makes Chevron unique is its focus on quality dividend growth, a strong balance sheet, and the willingness to distribute cash to shareholders.

Chevron

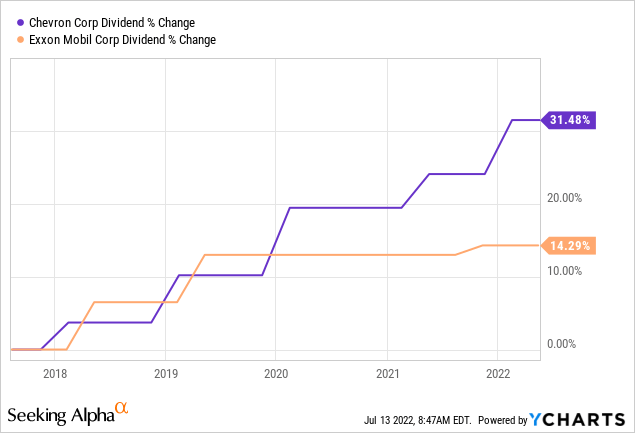

Since 2010, the Chevron dividend has doubled. Over the past 10 years, the average annual dividend growth was 5.3%. Over the past 5 years, the dividend has been hiked by 31.5%, beating XOM’s hikes by roughly 15 points.

Data by YCharts

The most recent hike was announced on January 26, when the company hiked by 6%.

Even if long-term dividend growth falls to the 4-5% range, that’s decent and enough to support the income stream this 4.1%-yielding stock generates.

It helps tremendously that Chevron’s breakeven oil price is roughly $50. This is above the breakeven price of efficient onshore drillers with prime real estate in the United States, yet it’s a decent price that I don’t expect to see for a long time.

Please note that the company’s $50 breakeven price not only covers production expenditures but also its current dividend (no buybacks). In other words, if oil falls to $50, investors won’t have to fear that the company needs to cut its payout. Even if oil crashes below $50, the company has a history of using debt to fill the gap. It has a healthy balance sheet as I will show you in this article and all oil crashes have been short-lived so far.

At $75 Brent, the company has room to boost both its dividend and buybacks. If Brent remains at $75 between now and 2026, the company estimates to be able to repurchase 20% of all shares outstanding.

So far, buybacks haven’t achieved a lot. in 2017, the company had 1.88 billion shares outstanding. At the end of 2021, that number was 1.92 billion.

For example, between the end of 2021 and the end of 1Q22, the company bought back shares worth $1.3 billion. Yet $4.6 billion in shares were issued for stock option exercises.

About two-thirds of the vested options at year-end 2021 were exercised during the first quarter, lowering the potential future rate of dilution from the outstanding balance. Over time, we expect our share buybacks to more than offset the first quarter dilutive effect.

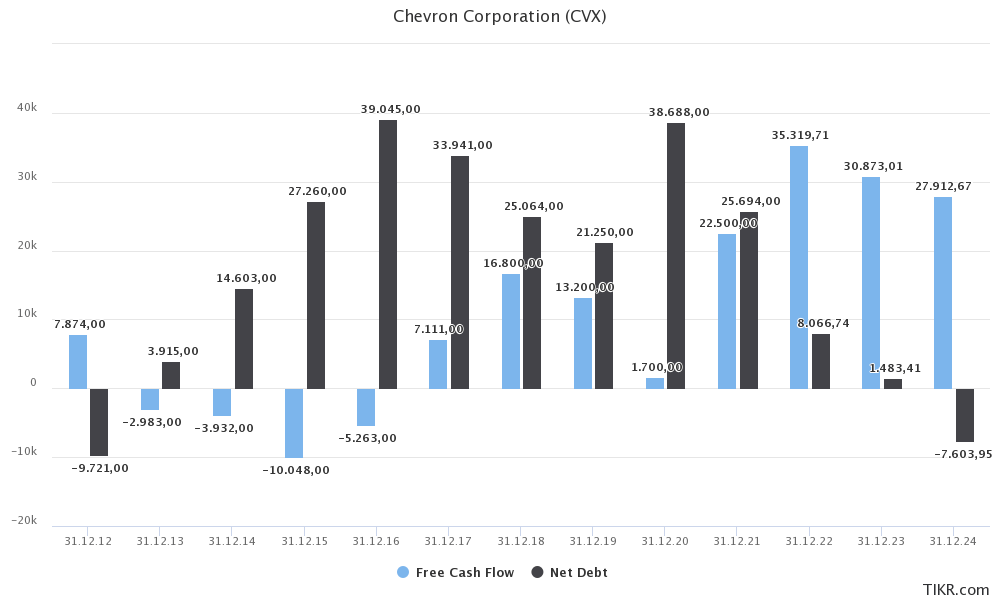

The environment for aggressive shareholder returns couldn’t be better. According to current estimates, the company is in a good spot to do $31.3 billion in average free cash flow over the next 3 years (including 2022). That’s 11.4% of the company’s $273 billion market cap. Moreover, if the company doesn’t do aggressive buybacks, its net debt balance will be negative by 2024 – meaning more cash than gross debt.

TIKR.com

In other words, these numbers support $10 billion in annual buybacks, the 4.1% dividend yield, and debt reduction.

As a result, Chevron has an AA- debt rating with a stable outlook as affirmed by S&P Global last year. AA- is high-grade debt. It beats the credit rating of many respected countries.

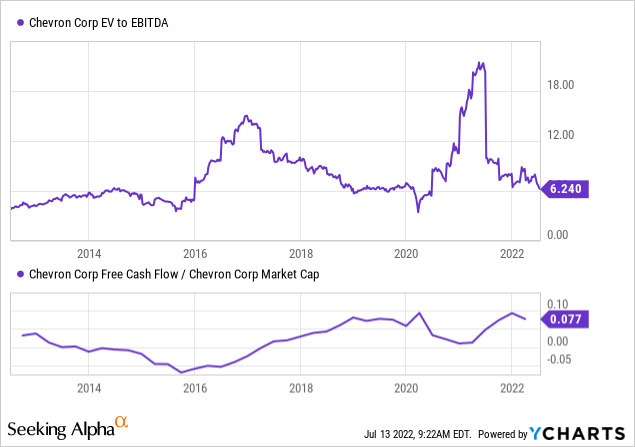

With that said, the company is also cheap. Using its $273 billion market cap, $1.5 billion in expected 2023 net debt (to price in the impact of high free cash flow), $5.9 billion in pension-related liabilities, $880 million in minority interest, and $55.3 billion in EBITDA gives the company an enterprise value of $281.3 billion and an EV/EBITDA multiple of 5.1x.

That valuation is attractive. The same goes for the implied free cash flow yield of 11.4%, which is one of the highest in decades, indicating that investors are not overpaying to get access to the company’s cash flows – which is extremely important.

Data by YCharts

Takeaway

Chevron is one of my favorite sleep-well-at-night stocks. It’s so conservative that I sometimes “forget” that I own it. America’s second-largest oil company has a lot going in its favor. The oil supply is tight and expected to remain tight. If anything, things could get worse once demand accelerates again as drillers are either unwilling or unable to increase production due to years of underinvestments and political/corporate pressure to focus on renewables.

Moreover, in this inflationary environment, investors favor value/dividend stocks. Chevron offers a 4.1% dividend after its stock price fell roughly 25%. This is a good yield. It gets better as the company remains in a fantastic position to not only boost its dividend (on a long-term basis) but also to accelerate buybacks thanks to high free cash flow and a low breakeven oil price.

The company has a fortress balance sheet and rapidly falling outstanding stock options that will allow management to reduce the number of stocks outstanding by up to 20% in the 4 years ahead.

However, bear in mind that oil is volatile. Do not go overweight oil and be aware that the main reason to buy CVX is buying income. If you want high(er) long-term growth, other stocks offer more opportunities.

Other than that, I think Chevron is in a good spot for investors to either initiate a position or add exposure to an existing position.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment