Editor’s note: Seeking Alpha is proud to welcome WR Investment Group as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

DINphotogallery/iStock via Getty Images

Investment Thesis

We believe Chesapeake Energy (NASDAQ:CHK) may be a great value Buy, as it is well positioned to capitalize on natural gas markets heading into 2023. Chesapeake are set to take advantage of record 2022 cashflows to fund 2023 initiatives and strategies. Impressive operational efficiency margins, recent acquisitions and increasingly unstable global supply uncertainties all bode well for the long-term longevity of recent profits. Insiders buying close to the current price range may provide the most bullish signal yet.

Brief Introduction

Chesapeake Energy is an independent oil and natural gas production and exploration company headquartered in Oklahoma City, Oklahoma with the core of its operations focused on Louisiana, Ohio, Oklahoma, Pennsylvania, Texas, and Wyoming. Share prices closed at $94.37 in the latest trading session of 2022, resulting in a gain of over 46% for the year, significantly outperforming the S&P 500’s loss of slightly over 19%.

Interview with CEO Nick Dell’Osso

CEO Nick Dell’Osso recently gave an exclusive interview with ‘Squawk Box’ where he discussed Chesapeake’s continued profitability at current natural gas prices, despite the strong recent gas price reduction heading into 2023, highlighting favorable supply and demand fundamentals as the reason for this. Nick also claims Chesapeake’s strong balance sheet renders it well suited to handle additional natural gas volatility in the years to come.

These claims may be supported by Deloitte’s 2023 oil and gas outlook report, whereby heightened cashflows throughout 2022 are expected to bolster energy corporation balance sheets and fund strategies and initiatives throughout 2023. The core concerns throughout the industry continue to revolve around energy security, supply diversification and low carbon technology transition; and the wider geopolitical and macroeconomic factors will be driving themes throughout the next year. Nick’s optimism comes as no surprise to us, as 93% of oil and gas executives expect the positive momentum of 2022 to continue across 2023.

It is of our opinion that energy companies focused on maintaining economic stability and sustainable financing are well positioned to continue generating the greatest profits throughout 2023.

Macroeconomic Factors

It is important to keep wider factors in mind when exploring the potential of Chesapeake. Disruption of energy trade between Russia and western markets in 2022 has driven oil and gas markets to new highs which has bolstered cashflow and profit; however, we have begun to see a sharp decline in natural gas prices heading into 2023, which will hurt margins.

On a more positive note for Chesapeake, a slower-than-expected adoption of low-carbon technologies and the shortage of agricultural products used in renewable fuels have disrupted the energy transition, maintaining favorable demand economics.

However, we should stay alert to political pressures, higher energy prices and increasing regulations which will continue to accelerate pressure on cleaner energy transitions and Chesapeake will need to further commit and adapt its operations to adopt these changes to remain competitive.

Qualitative Analysis

Analysts back Chesapeake as a buying opportunity with an average 12-month price target of around $115, representing a gain of 29%. This is most likely as a result of the company’s exposure to a favorable gas outlook, bolstering free cashflow; at current strip prices, Chesapeake could generate up to $5 billion of free cashflow in 2023.

Chesapeake’s EPS has been consistently beating analyst earnings expectations by more than 12% for the last three consecutive quarters, demonstrating favorable momentum which may be more likely than not to continue. Recent positive revisions to analyst estimates demonstrate the dynamic nature of business trends and may be interpreted as a good sign for the mid-term performance. Chesapeake Energy approaches its next earnings release towards the end of February, where it is projected to report earnings of $3.61 per share , which would represent an annual growth of 51%.

A good indicator of opportunity is insider activity – there have been no insider transactions in the last 6 months; however, the last transactions occurred at the end of June where executives bought $14 million worth of stock in the $80 – $85 region. The opportunity recognized by insiders at these prices suggests that current levels present an attractive buy.

Recent acquisitions of Chief E&D Holdings and Vine Energy have likely laid the path towards long-term lower production costs and greater production volume. Analysts are optimistic as a result of this and expect growth to continue at 22% per annum over the next 5 years.

Quantitative Analysis

Chesapeake’s profitability has a questionable history at best; however, development has seen impressive lately, with net income growing by 58% annually over the last 5 years to $2.8 billion. This gives Chesapeake a net margin of 27% which is relatively average compared to the wider industry. Net income also shrank by 38% from 2021-2022, a possible warning of potentially slowed development.

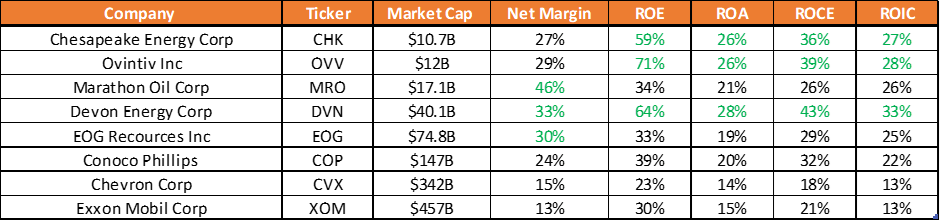

However, when we look at Chesapeake’s returns on assets, equity, capital employed and invested capital, margins stack up very well against the competition. This is a sign of efficiency when employing the resources available to Chesapeake, and potentially supports our earlier thesis that strong 2022 cashflows and acquisitions have put them in a stronger financial position which may enable them to capitalize on gas markets in the years to come. The table below compares key profitability and efficiency factors between competitors in this space.

Compiled by the Author

The strongest three results for each parameter have been highlighted in green text. It can be seen that Chesapeake’s overall position is consistently strong, as the return margins are high across the board despite an average net margin; suggesting higher efficiency with less capital, which may position Chesapeake well as they continue to grow. The highest performing competitors in this space are Ovintiv (OVV) and Devon Energy (DVN), which must be continuously monitored over time to ensure Chesapeake’s efficiency remains comparably high.

Free cashflow has also been consistently growing from 2020 and has risen by 249% over the last year to a total of $2.1 billion. Capital expenditure is also being decelerated, indicative of intentionally slowed development but allowing greater potential for cashflow to be distributed to shareholders through increasing dividend pay-outs or share buybacks, a positive sign for investors in the medium to long term.

Valuation

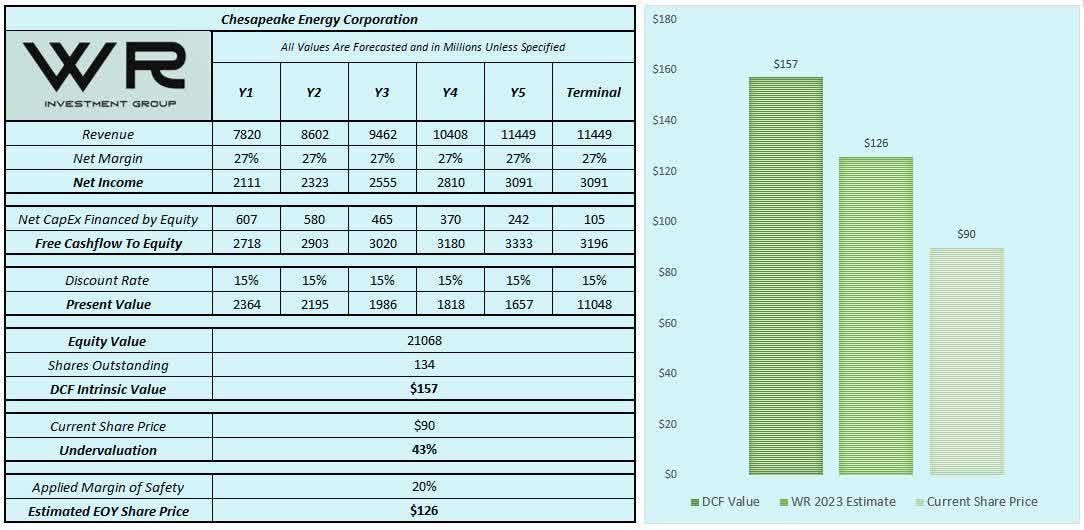

Valuation is also important, so investors should note that Chesapeake Energy has a Forward P/E ratio of 5.42 at the time of writing. We have performed a relatively straightforward equity based DCF analysis, the results of which are summarized below. As a measure of comprehensive safety, we have used conservative inputs such as modest annual revenue growth of 10%, an aggressive discount rate of 15% as well as a terminal rate of 0%. Assumptions which should be noted are a consistent net margins and discount rates across the 5-year period.

DCF Analysis (Author’s calculations)

We have found that even under restrictive inputs, it can be speculated that the intrinsic value likely lies around or above $157, representing a margin of safety of 43% compared to the current price at around $90. Applying a margin of safety to this suggests a target of $126 by the end of 2023 is feasible; thus representing a strong value-oriented investor opportunity worth considering.

Discussion of Risks

Chesapeake’s solvency is likely its greatest weakness at the moment, while a current ratio of 0.49 and quick ratio of 0.02 indicate short-term assets and cash are not substantial enough to cover liabilities; however, an interest coverage ratio of 24.74 indicates the debt is manageable and sustainable financing is still being practiced. The debt/equity ratio of 0.43 further supports this.

Chesapeake’s Altman-Z score sits at around 2.1, which initially indicates some struggle; however, we must keep in mind that this is its highest level in years, indicating that financing and profits are heading in the right direction.

One factor to remain aware of is that Chesapeake’s CEO has claimed that the company strategy is to maintain relatively flat production for the next couple of years until an increase in structural demand is observed; this may weaken Chesapeake’s position in the event of unexpected demand rise.

Conclusion

In conclusion, we have found that Chesapeake Energy may possess a significant undervaluation when considering its record cashflows which may well continue into 2023 as a result of long-term profitability rise and high capital efficiency.

Chesapeake’s debt is high compared to its cash and current assets; however, compared to equity and income, this debt and its interest payments seem sustainable. Investors should remain cautious of intentionally slowed capital expenditure, but recognize that this could be part of a strategy geared towards share buybacks and/or increasing dividends in the medium term.

Analysts are generally optimistic that earnings growth and upwards price action will continue over the next few years, and company insiders agree as they have bought $14 million of stock within the current price region. Chesapeake’s focus on bolstering its finances using the record 2022 cashflows as well as new acquisitions could aid in funding its initiatives in the years to come, potentially supporting resistance to adverse gas price swings and wider instability.

Despite this, investors should remain cautious about decelerated development, wider macroeconomic events, and political pressures which have a direct impact on Chesapeake’s profitability and its ability to remain competitive.

Be the first to comment