Sarah Kerver

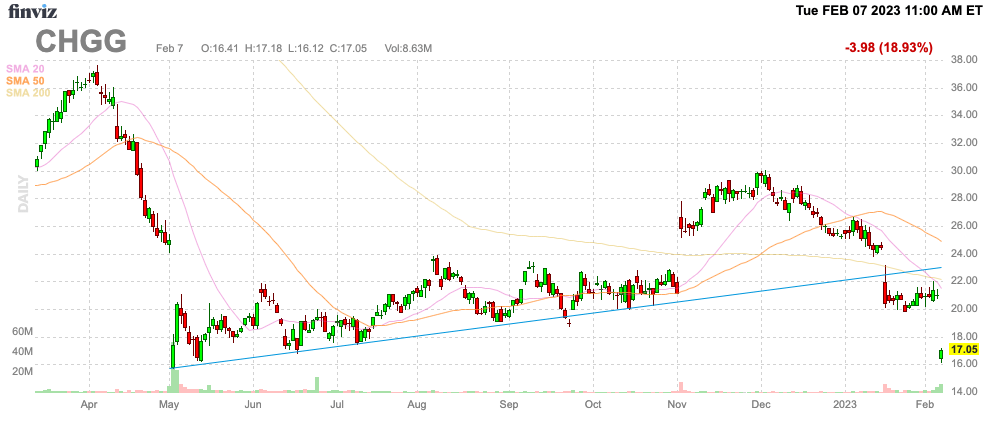

After another weak quarter, Chegg, Inc. (NYSE:CHGG) stock has fallen 20%, to prices far below pre-covid levels. The problem facing the student learning platform is that school systems aren’t pressing academic rigor to the same levels as pre-covid and fewer students showed up to higher education systems. My investment thesis is slightly Bullish on CHGG stock due to a compelling valuation and some expectations for the higher education system to normalize back at pre-covid rigor.

Finviz

No Growth

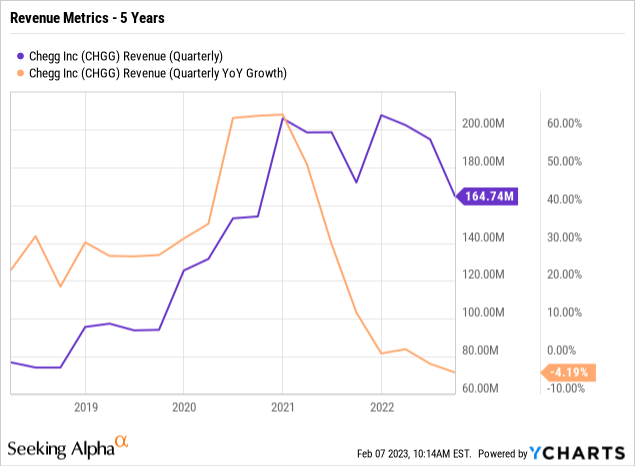

Chegg reported Q4’22 revenues decreased 1% from the prior year period of $205 million. The company has now entered a no-growth period as fewer students in the education systems make sales growth a difficult task after the covid surge in online education demand during 2020.

The education platform saw the subscriber base double during covid, with the quarterly revenue base surging from $100 million to over $200 million in a few quarters. The market shouldn’t be surprised to see Chegg now struggle for a short period to absorb this growth and recalibrate the business for a slightly different education system coming out of covid.

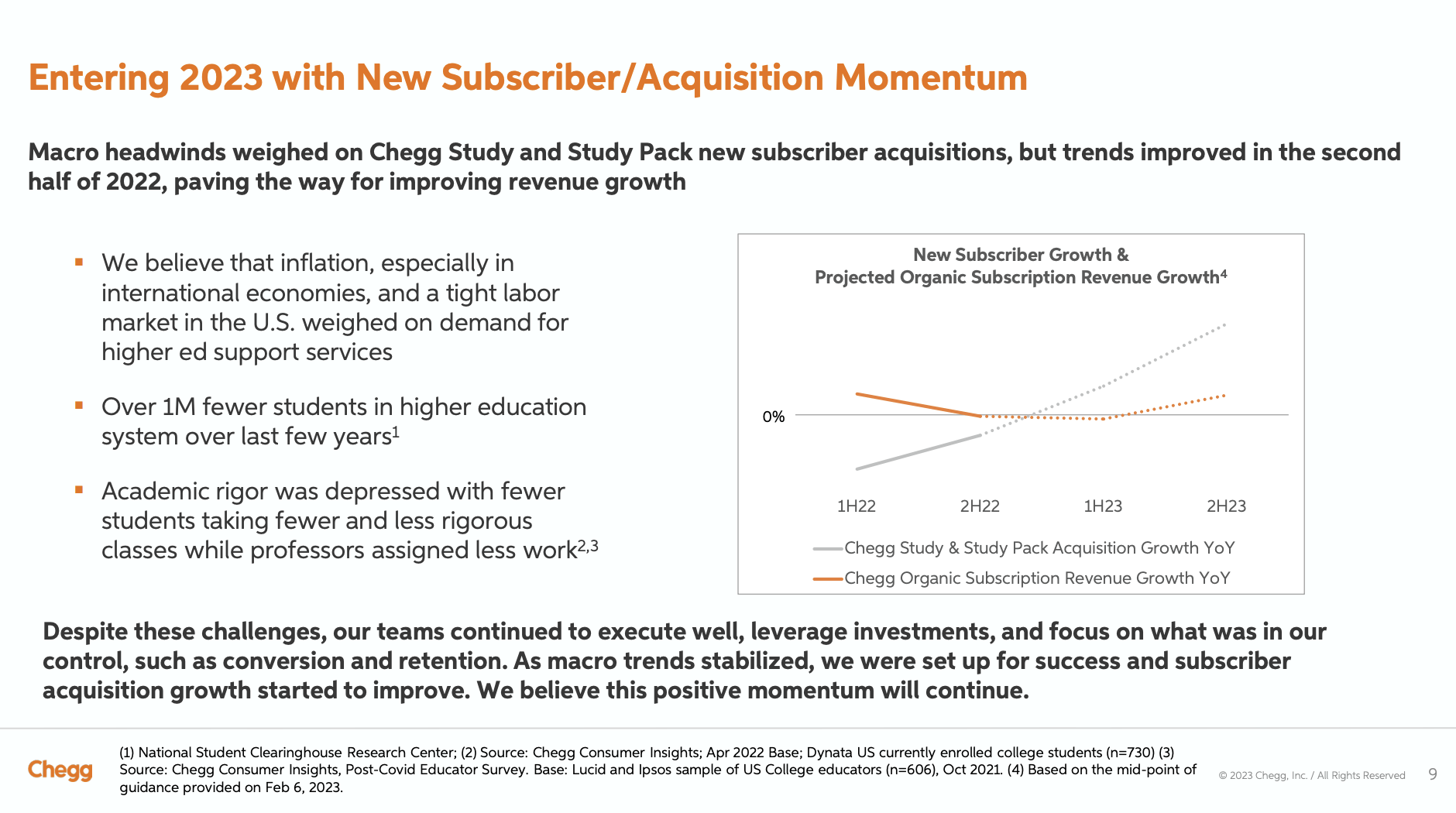

The company even suggests subscriber growth struggled during 2022 as professors assigned less work and were less rigorous coming out of covid, reducing the need for educational support. On top of inflation pressures, students have less income to afford the Chegg subscription services.

Chegg Q4’22 Presentation

The company enters 2023 with a subscription hole. As customer subscribers roll off, Chegg doesn’t have the same amount of replacements to enter the platform.

The education support platform remains highly profitable in order to survive this difficult period where some expectations exist for a more normalized educational environment heading into 2024 and beyond. The company earned $0.40 in Q4 alone and produced $74 million in adjusted EBITDA for an impressive margin of 36%.

Tough Year Ahead For Chegg

The problem facing the stock is that Chegg only guided to Q1’23 revenues of $185 million, down 8.5% from the prior year. The company still faces headwinds in turning new student subscribers into growing revenues.

The revenue guidance for the full year of just above $750 million is down slightly from 2022 levels. The guidance suggests an inflection point in the year ahead where Chegg returns to growth similar to the above chart.

The market doesn’t like guidance where improvements have to occur in the business in future periods in order to hit annual financial targets. The stock could easily slip further until Chegg starts generating the improved financial metrics to confirm the return to growth.

The forecast has 2023 adjusted EBITDA at nearly flat levels at $245 million, with impressive free cash flows of $190 million. The company already has $1.3 billion in cash on the balance sheet and a remaining share buyback approval of $643 million, allowing for continued repurchases of the $1.1 billion of outstanding convertible debt.

The market cap has dipped to only $2.1 billion following the weak reaction to a tough year ahead. The stock trades at ~3x forward sales, which is expensive for a stock with no growth and cheap, if Chegg can return to double-digit growth in 2024.

Chegg, Inc. stock trades at only ~11x prior 2023 EPS targets. Assuming a normalized education environment in 2024 where rigor returns to higher education, Chegg would be cheap on a normalized growth and profit view.

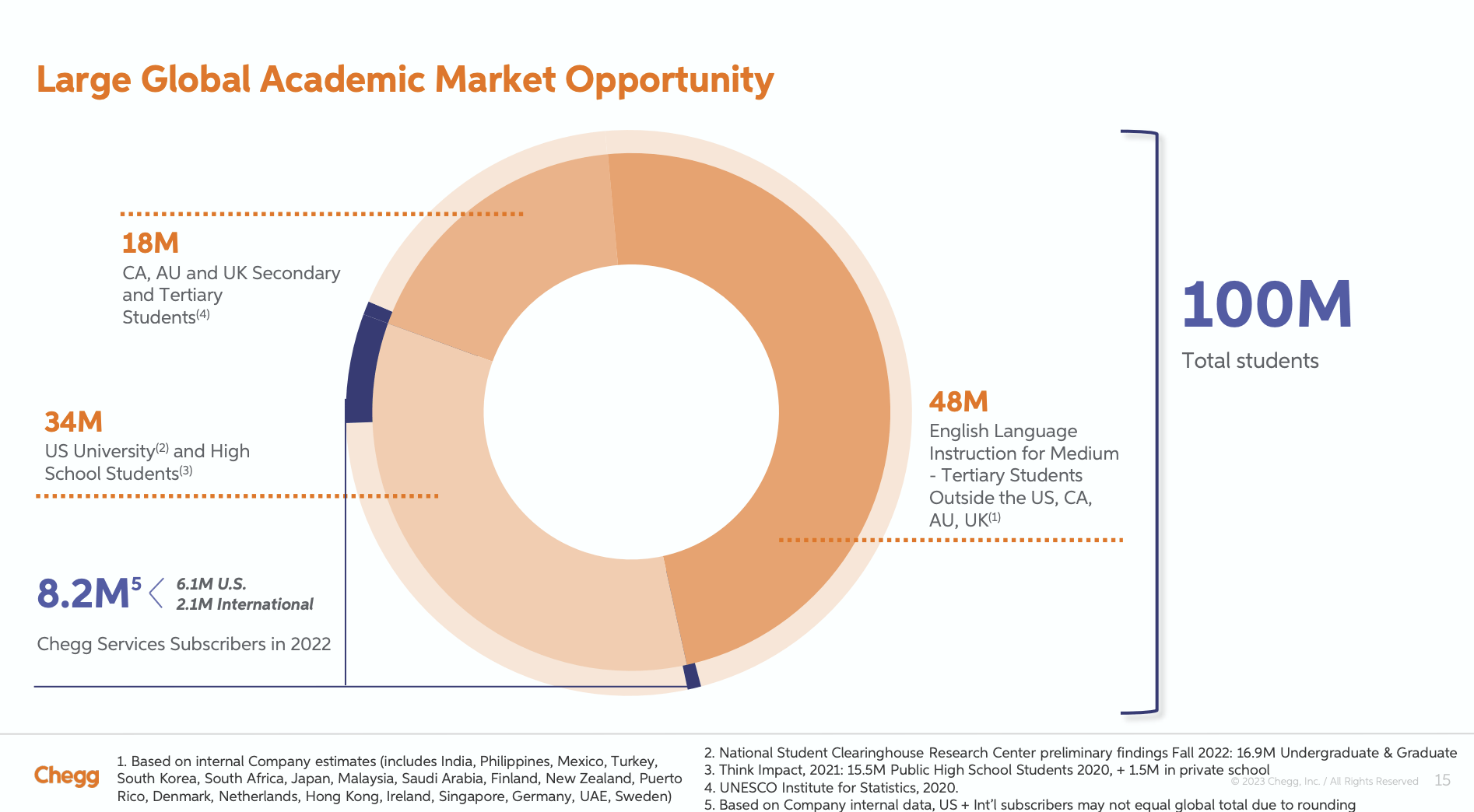

The company has a massive global market opportunity, with 100 million students in English language schools. In addition, Chegg predicts an easy ability to raise monthly subscription prices and even move to annual subscription options once the economy improves.

Chegg Q4’22 Presentation

Takeaway

The key investor takeaway is that Chegg now has a compelling valuation after this massive dip from the covid peaks above $100. The stock no longer prices in any growth for the online learning platform, despite the opportunity to return to growth mode in the future as education normalizes following the volatile covid period.

Chegg has a compelling risk/reward profile trading at the recent lows, but investors should wait for a complete shakeout of the stock before investing. The risk still exists that higher education demand is permanently reduced and Chegg, Inc. struggles to generate future growth.

Be the first to comment