everythingpossible

Investment Summary

Mergers and acquisitions in the broad healthcare spectrum have been rife across FY20-FY22′. After a slow start to the year, revenue obtained from healthcare M&A shot to an all-time high of c.$19Bn by Q2 this year. The trend somewhat continued in Q3 with ~$8.3Bn in M&A revenues, a 59% YoY increase.

Within that scope, healthcare services giant CVS Health (CVS) agreed to acquire Signify Health (NYSE:SGFY) for $30.50 per share in an all-cash consideration, placing the valuation at $8Bn. For reference, SGFY currently trades at a $6.7Bn market cap or $28.47/share, and a $5.3Bn enterprise value (“EV”). We’ve been actively pursuing selective opportunities within the healthcare space with uncorrelated/differentiated alpha in FY22, so this deal naturally piqued our interest. Here I’ll discuss our examination findings, and what it may mean for SGFY longs looking ahead.

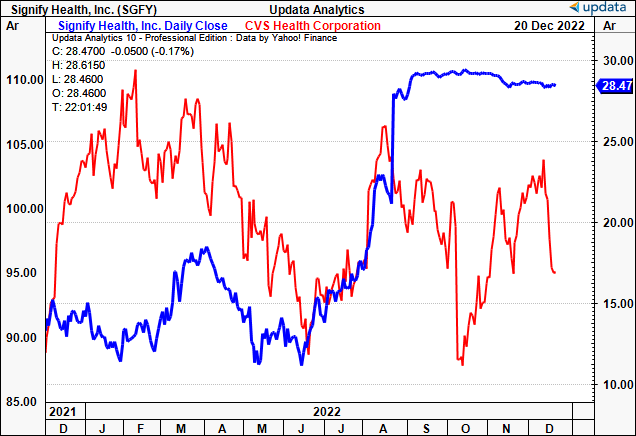

SGFY vs. CVS share price evolution, December 2021-December 2022

Data: Updata

Recent Developments for SGFY

Turning to the most recent advancements in SGFY’s growth engine, it’s worth reminding investors that it completed the acquisition of Caravan Health in March this year. It finalized the transaction on a $250mm valuation, made of cash-script consideration of $190mm in cash and $60mm in SGFY common stock, respectively.

Embedded in the deal are certain milestone payments of $50mm in cash dependent on Caravan Health’s performance. We can expect further data for both the integrated company’s financials in the full-year results from SGFY early next year.

For SGFY, this was a logical and smart move in our estimation. The deal sees the company now overseeing ~$10Bn in medical expenditure under management, whilst diversifying the stream of income to its top-line. This has two main benefits: 1). It hedges top-line growth from large sigma events, and disruption from large accounts by more evenly distributing the revenue across more sources; 2). It also provides additional sources of value to the company, potentially increasing the revenue run-rate.

Moving to more recent developments, in October, SGFY also expanded its at-home diagnostics segment for Medicare and Medicaid members. Most notably, we saw that its offering now spreads to diagnostics for chronic obstructive pulmonary disease (“COPD”), peripheral arterial disease (“PAD”), colorectal cancer, chronic kidney disease (“CKD”), diabetes, and low bone density (osteopenia and osteoporosis). With an ageing population, in which we’ve talked about extensively in the past, we believe this is a sound progression to expand its at-home offering.

And finally, it’s worth noting that SGFY also expanded its collaboration with Ardent Health Services in December. Ardent has more than 200 sites operating across 6 states and is a strategic collaboration for SGFY in our estimation. Specifically, Ardent will roll into an FY23 “(SGFY)-enabled accountable care organization (“ACO”) to implement care transformation, manage risk and provide high-quality, coordinated care for its Medicare patients.” Note, this aligns with CMS’ objective of rolling all Medicare beneficiaries into an accountable relationship over the coming decade and could be a good sign in the eye of regulators.

SGFY financial health leading into transaction

It’s first worth pointing out that the CVS acquisition of SGFY has received support from key stakeholders. New Mountain Capital, purportedly the 60% owner of SGFY’s common equity, was quick to assign its proxy vote in favor of the acquisition.

The deal, expected to close in H1 FY23, is therefore likely seen as a positive in both companies’ eyes. Turning to the numbers, in Q3 FY23, SGFY reported revenue of $139.8mm, down from $199.2mm the year prior.

On this, OpEx jumped to $226.2mm, driven in part by a $16.7mm one-line item of restructuring expense, but mainly from the $123mm in service-related expenditure. It brought this down to an operating loss of $86.4mm and EPS of negative $0.90, behind the positive $0.12 in EPS last year. Net-net, it also realized $23.3mm in CFFO for the quarter, an 81% YoY decrease.

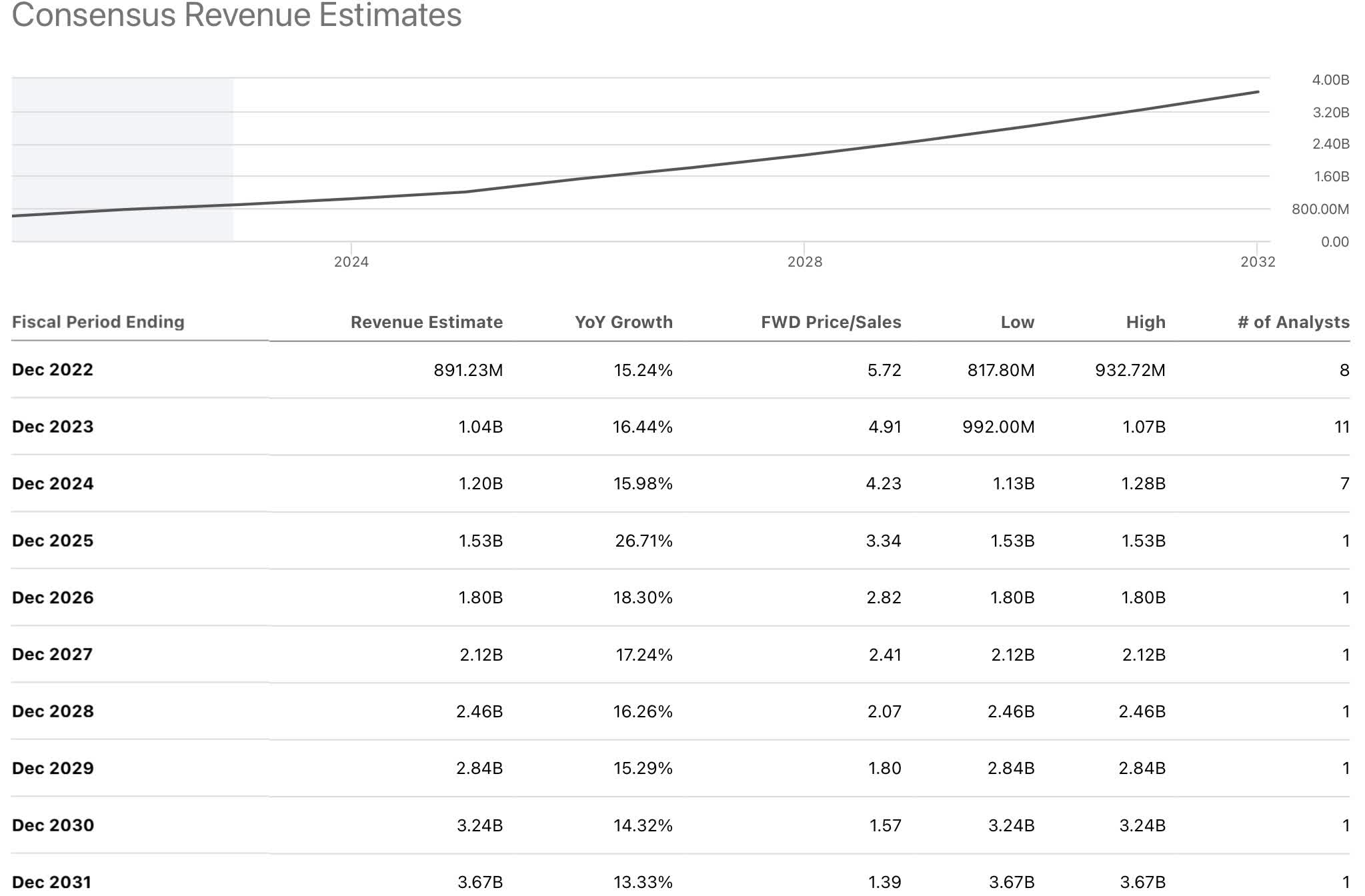

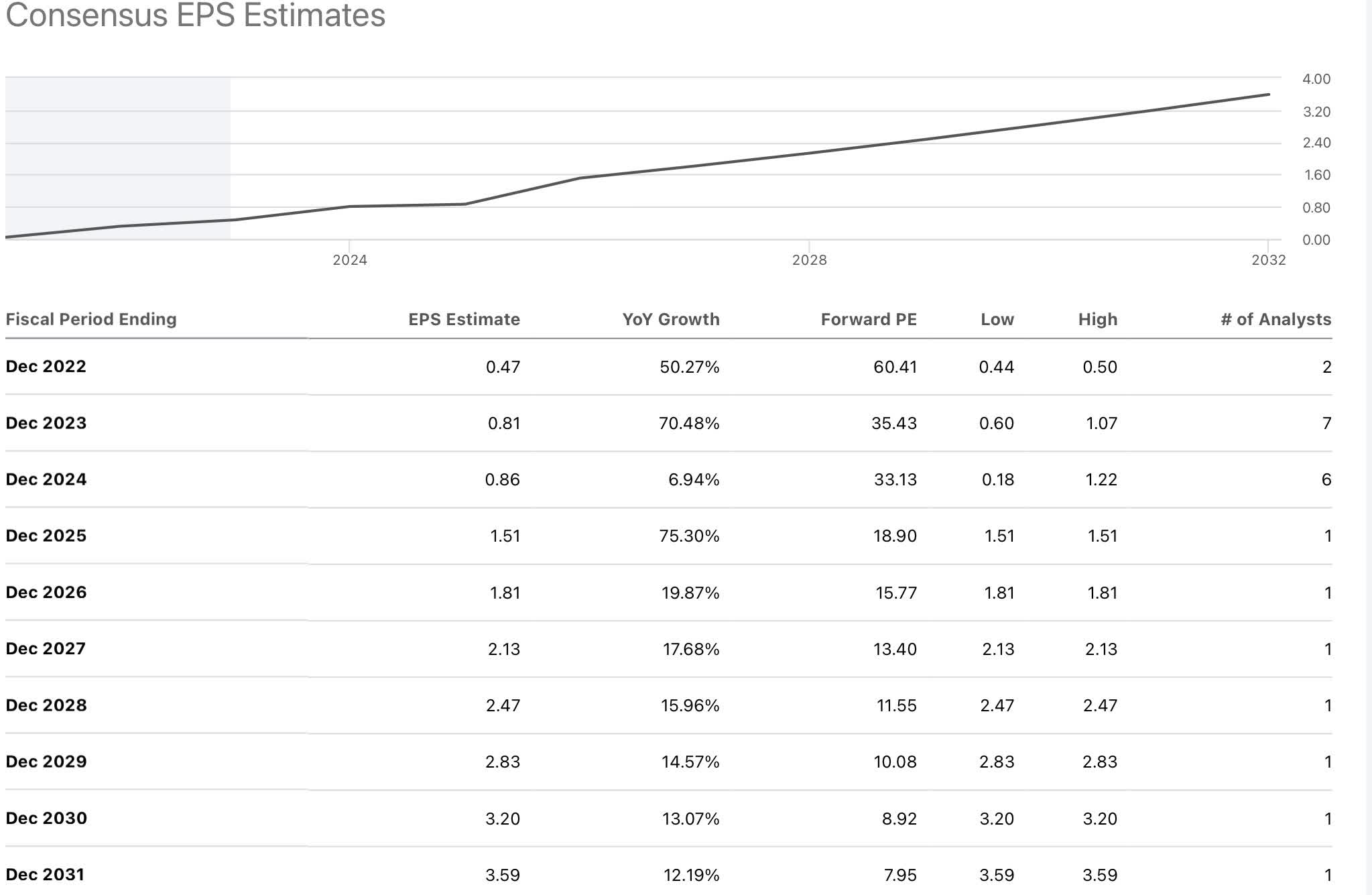

Looking ahead, you can see the chain of analyst expectations for both revenue and EPS into 2030 in the charts below. It’s worth noting that EPS is estimated to climb YoY across this period, which could certainly be accretive to CVS’s bottom line as well. The same can be said for its projected revenue clip, as seen in Exhibit 1.

Exhibit 1. SGFY consensus revenue forecasts, FY22-31‘

Data: Seeking Alpha SGFY, see: “Earnings Estimates”

Exhibit 2. SGFY consensus EPS forecasts, FY22-31′ (note, these are non-GAAP estimates)

Data: Seeking Alpha SGFY, see: “Earnings Estimates”

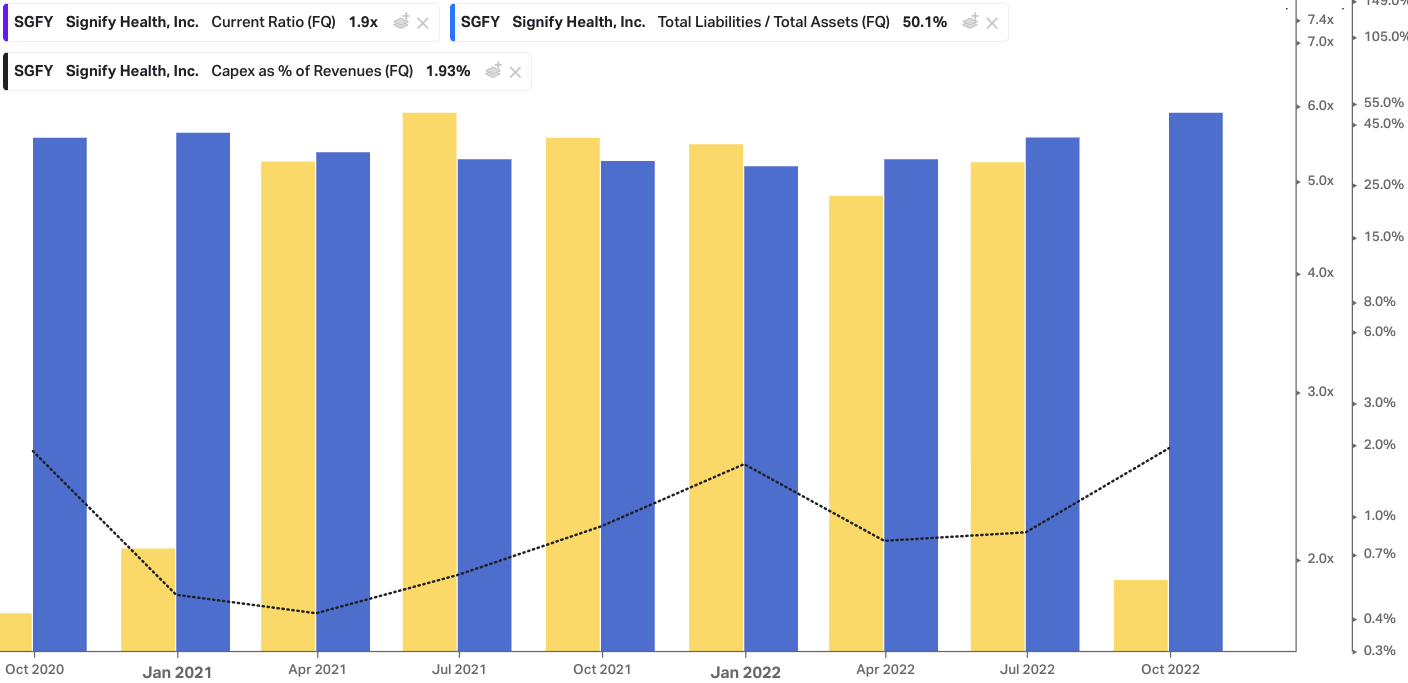

Turning to the balance sheet, SGFY is in a reasonably strong current position. Short-term liabilities are covered ~2x by liquid assets, whereas the capital structure is evenly split between primary claimants and equity holders (Exhibit 3).

Meanwhile, quarterly CapEx at longer term average of ~$2.7-$3mm is only c.200bps of overall revenue, in-line with historical ranges. These pointers, along with the catalysts described above, tell us that SGFY is adequately positioned to reach the top-bottom line forecasts listed above.

Exhibit 3. SGFY Solvency ratios (debt ratio, current ratio) and CapEx as function of quarterly revenue

Data: HBI, Refinitiv Eikon, Koyfin

Valuation and conclusion

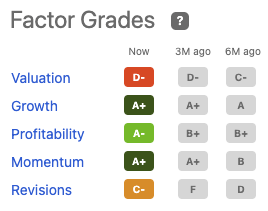

Objectively, there isn’t support for SGFY’s valuation upside, based on quantitative analysis provided by Seeking Alpha’s proprietary factor grading (Exhibit 4).

Despite this, in terms of growth, profitability and momentum, ratings are high, which balances the investment debate, and potential for capital appreciation. Moreover, the stock trades below the CVS offered bid price of $30.50 per share. All things considered, we believe there’s scope for the stock to push higher towards the offer price, and this creates an upside potential of ~710bps.

On this fact, we continue to rate SGFY a buy. There is good potential to collect the 710bps premium discussed, and this confirms our buy call on the stock until H1 FY23 when the deal is expected to close.

There is also upside risk to the deal, if there are new factors in the consideration, or, if another bidder were to come along with a more favorable bid. At this point, this seems unlikely, but shouldn’t be discounted entirely in our view. Rate buy.

Exhibit 4. Quantitative Factor grading suggests valuation is a concern, but the stock trades below the offer price, allowing investors to potentially collect ~710bps in upside premium before H1 FY23

Data: Seeking Alpha quantitative factor grades, SGFY

Be the first to comment