Traitov

Check Point (NASDAQ:CHKP) is well positioned to capitalize on the strong demand for cyber solutions and profit from cloud storage and IoT segments growth. The advantage of Check Point is the wide range of solutions offered, which cover almost all segments of the cybersecurity market. The company is delivering strong financial results on superior profitability, while the growing IT spending and cyber security awareness could allow CHKP to expand by double-digits further. This will be facilitated by the development of Infinity architecture, which provides comprehensive solutions in the fields of network, cloud and mobile cybersecurity, and reinforcing it with advanced solutions across all vectors. I am bullish on CHKP, as the stock appears undervalued compared to the sector, and has good upside potential.

Outlook

Amid the key trend in the TMT sector in 2023 of digitalization and metaverses development, strengthening of cyber defense also align here. Against the backdrop of the digital transformation, information security is becoming a priority. With the introduction of a large number of technologies and devices, the risks of encountering cybercrime is rising, which requires investments in protection.

Check Point occupies one of the leading positions with a wide range of solutions offered, which cover broad segments of the cybersecurity market. I believe that the company has a good prospect to further strengthen its position amid the backdrop of fast-growing sectors like cloud storage and the IoT.

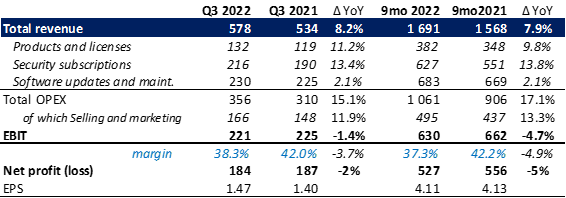

Robust demand for cyber security solutions has enabled Check Point to deliver strong performance, even in the current challenging economic environment. Revenue in the third quarter of 2022 accelerated by 8.2% YoY and reached $578 million due to continuation of double-digit growth in products and security subscriptions.

Q3 2022 financial results (company reports)

Additionally, deferred revenues saw 13% YoY growth to $1.7 billion, while billings amounted to $559 million, up 8% YoY in Q3 alone.

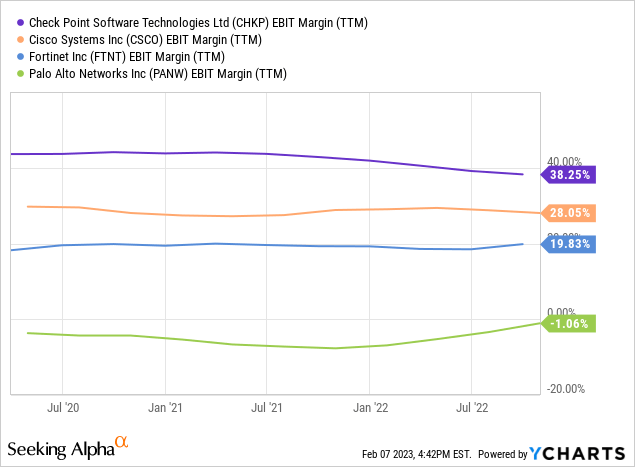

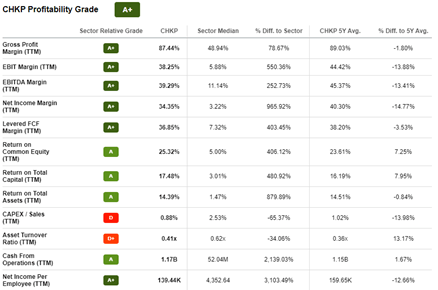

Another strength of the company, which splits up CHKP from its competitors with a moat, is high profitability readings compared to the sector’s players.

From the 88% gross margin in Q3, the operating margin stood at 38.3%, which is 370bps down on the back of cost pressure (+15.1% YoY). The latter came across as the cost for raw materials and shipping increased as a result of the shortages. Although management noted some relief in the shortages, some pressure on profitability could take hold for a while, steaming form the need for higher spending on promoting new products and services.

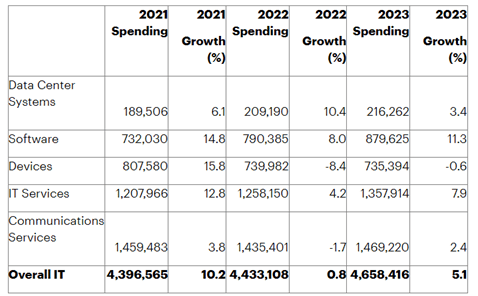

With global software spending expected to grow 11.3% in 2023, I expect cyber defense spending to follow suit.

Worldwide IT spending forecast (in millions of USD) (Gartner)

Following the outperforming growth of data center systems in 2022, software spending should now take over, ensuring the high utilization of that infrastructure as a result of increased implementation of machine learning, IoT, cloud and big data. I believe Check Point, as one of the major players in the cyber industry, is well positioned to benefit from this trend.

On the balance sheet, a strong cash position coupled with resilient cash flow generation capacity gives the company an ability to further drive organic growth and M&A activity, as well as capital return to shareholders though buyback programs.

To sum up the industry trends, the pandemic tilted business models and consumer behavior to digital technologies. The popularity of various cloud and online services and digital payments is growing rapidly, while the hybrid work environment has become the new normal. This is a perfect landscape for the intensification of cyberattacks. Against this background, information security will most likely continue to be one of the priority items in the context of further digital business transformation.

Valuation

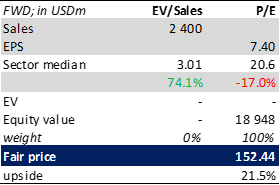

The company also gives an updated full-year projection, with revenue ranging from $2.2 billion to $2.4 billion and EPS (non-GAAP) in the $7.2 to $7.4 range, where both are at the high end of expectations. I am bullish about the prospects of CHKP delivering financials at the high end, and incorporate $2.4 billion sales and $7.40 EPS for the fair value estimate.

Comparable valuation (seekingalpha data, author’s estimates)

Based on the Seeking Alpha valuation section, Check Point is currently trading at a 17% discount to the sector median on forward P/E. However, the significant premium of 74% to the sector median levels could be spotted on the forward EV/Sales multiple. I believe that P/E is a more suitable multiple for the valuation of Check Point due to the superior profitability of the company compared to the sector’s peers.

Profitability grade (seekingalpha data)

I will put it another way, if we incorporate EV/Sales multiple in the valuation, we will disregard the company’s huge profitability advantage compared to the competition.

Applying the EPS of $7.40, the model yields Equity value of circa $19 billion and corresponds to $152 fair value per share with a 21.5% upside potential to the current price. During the third quarter, Check Point conducted a buyback for $325 million, and continuation of the repurchases will give an additional boost to fill the fundamental gap.

Risk factors

Further tightening of monetary policy could increase the volatility of technology sector, which continued to gradually acquire the features of traditional industries that are highly responsive to the changes in the macroeconomic situation. In addition, recession fears could restrain spending on cybersecurity, which will negatively affect Check Point’s financial performance.

Conclusion

I believe CHKP deserves a Buy recommendation, and represents an attractive opportunity steaming from the low valuation compared to the sector and its own historical levels as well. Check Point kept on growing with double-digits in product and security subscription revenues, while rising software spending should provide for sustainable demand for the company’s cyber security solutions going forward, especially on the backdrop of the growing application of big data, IoT and cloud computing. Additionally, the e-gov initiatives around the world, along with demand from healthcare and manufacturing will underpin the use of cyber security solutions. It’s worth also highlighting the strong balance sheet of the company with zero debt, which allows it to generate good cash flows and allocate significant funds to shareholders through buyback programs.

Be the first to comment