andresr

Investment Thesis

Chase Corporation (NYSE:CCF) is a specialty chemicals company based out of Westwood, Massachusetts, United States. The company recently posted third-quarter results for FY22, which I will go through in this report. The inflation has caused severe problems for the company, limiting its gross margin and affecting future growth. I believe the company is struggling to maintain organic revenue growth, and this is a serious cause of concern.

About Chase Corporation

Chase Corporation is an American specialty chemicals company that produces protective materials across diverse market segments. The company can be categorized into three business segments; Adhesives, Sealants and Additives segment, Industrial Tapes segment and, Corrosion Protection and Waterproofing segment. The Adhesives, Sealants and Additives segment has a wide range of products comprising end-use products and products that are integrated with another company’s products. This segment’s products include adhesive systems for electronics, polymeric microspheres, polyurethane dispersions, moisture protective coatings and cleaners. The Industrial Tapes segment caters to other manufacturers with wire and cable materials, specialty tapes and other laminated and coated products. This segment sells products to cable manufacturing, utilities and telecommunications, and electronics packaging industries. The Corrosion Protection and Waterproofing segment serve the infrastructure development companies across oil, gas, highway, wastewater pipelines and bridge deck projects. This segment’s main products include protective coatings for pipeline applications, coating and lining systems for waterproofing and liquid storage applications, high-performance polymeric asphalt additives, and joint expansion systems for waterproofing applications in transportation and architectural markets. Chase Corporation operates several manufacturing facilities across the United States, Europe, and Asia.

Third Quarter 2022 Results

Chase Corporation posted quarterly results on 11 July, 2022 for the quarter ending 31 May 2022. As per my analysis of the Q3 2022 results, the company underperformed across business segments. The results were inconsistent with the estimates, and the company witnessed contracting margins across all segments. I think the company was highly affected by the rising commodity prices, putting significant stress on the product pricing, eventually resulting in weakening demand and contracting profit margins.

Now let us look at the numbers. The company’s declared a total revenue of $88.6 million, a growth of 11% compared to $79.5 million last year. The revenue growth reflects an increase in the sales price of the products. According to my analysis, the inflationary pressure has forced the company to hike product sales prices, and the company did not witness any organic revenue growth. The Adhesives, Sealants and Additives segment revenue grew 9% to $36.7 million compared to Q3 2021. The Industrial Tapes segment’s revenue witnessed a 19% increase to $38.3 million from the corresponding quarter previous year. Revenue from the Corrosion Protection and Waterproofing segment was flat at $13.5 million compared to the same quarter last year with less than a 1% increase. I believe apart from the Industrial Tape segment, the company experienced a decline in the organic revenue growth if we take out the product price increase. The gross margin was 38.6% in this quarter as against 41.8% in Q3 2021. Even after serious cost-cutting measures and sales price increases, the gross margin contracted due to increased product costs. The net income saw a marginal increase of 8%, from $14.3 million in Q3 2021 to $15.5 million in Q3 2022. The diluted earnings per share (EPS) was $1.64 compared to $1.50 in Q3 2021. The company saw a reduction in the free cash flow from $15.9 million to $13 million majorly due to increased inventory levels. The company is expanding its inventory levels to execute the backlog orders.

As per my analysis, the company has a strong balance sheet with no long-term debts and a cash balance of $124.7 million. Chase Corporation also has a revolving credit facility of $200 million. This is one factor that stands out for the company, solid liquidity. But the firm’s main issue is the rising inflationary pressure that is contracting its margins. The problematic macro-economic factors will limit the firm’s organic growth, and unless the company finds a way to sustain its demand with an effective cost of production, I recommend not to take any new positions in the stock.

Adam P. Chase, President and Chief Executive Officer of Chase Corporation said:

Chase Corporation has continued to encounter headwinds resulting from global raw material inflationary pressures, labor shortages, and supply chain constraints, which is anticipated to persist throughout the remainder of the year. As such, we remain highly proactive in our efforts to mitigate the effects of these macro-economic challenges including engaging in close conversations with our suppliers, as well as implementing appropriate pricing actions as needed. Our Company remains committed to protecting our margins as well as serving our customers, shareholders and employees through appropriate staffing, excellent safety standards, and achieving optimal business efficiency.

What is the major risk faced by Chase Corporation?

Rising Commodity Prices

Chase Corporation has been severely affected by the rising commodity prices globally. The high commodity prices have resulted in an increased cost of production for the company. The company depends heavily on petroleum-based raw materials for production, and in FY21, the company struggled to manage sales prices with the sky-rocketed oil prices. I think the inflation across all raw material segments will continue in the FY22 and limit the firm’s gross margin. Going ahead, the company might face a weakened demand given the slip of the US and the European economy into a possible recession. The company is taking steps to manage this risk by improving inventory levels and employing drastic cost-cutting measures, but these efforts are not translating into significant results.

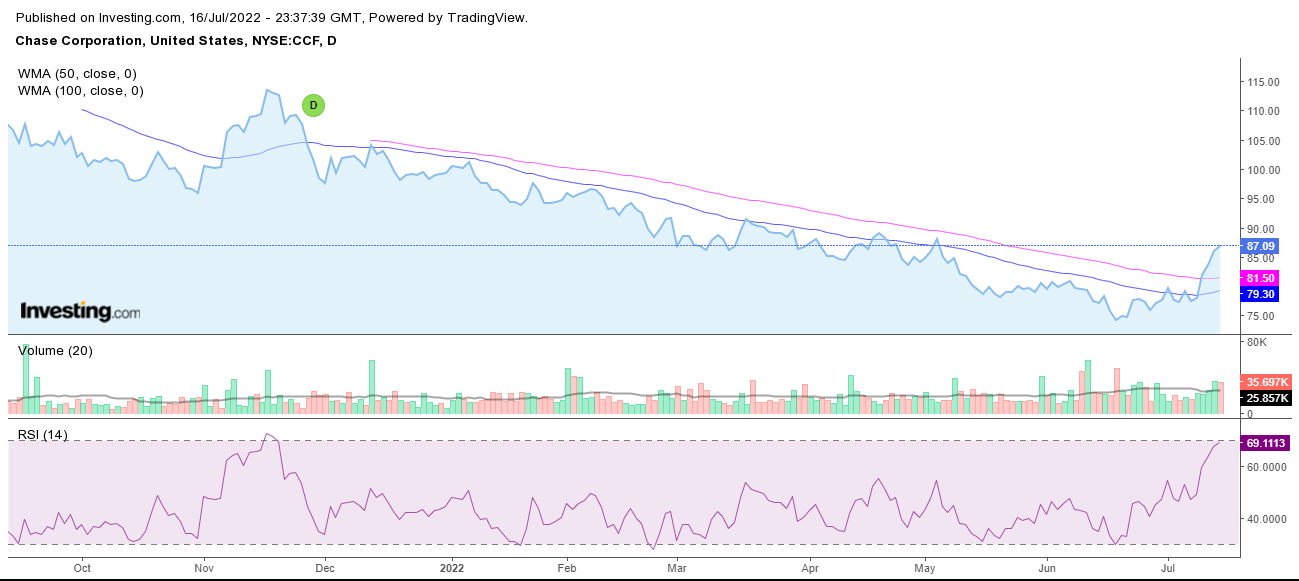

Technical Analysis and Fundamental Valuation

Technical Analysis (Investing.com)

Chase Corporation has recently crossed its 50-day, and 100-day weighted moving average (WMA). This generally reflects a fresh momentum in the stock. But I believe it is early to make a decision based on the WMA, and I advise waiting a couple of weeks to see if the stock sustains above the 50-day and 100-day WMA. The RSI indicates that the stock is heading towards the overbought territory by breaching the 70-band range. The stock might take a sharp turn downwards after testing the 70 band, so I recommend not to make any new position in the stock currently.

I think the Chase Corporation is fairly valued at current levels. The company has a P/E multiple of 18.20x. The stock price has seen a decline of 26% from its 52-week high of $119 and is currently trading at $87. Given the weak future prospects of the company, I would recommend not making any position in the stock currently, and for the investors who already are invested in the stock can hold the stock and wait till the macroeconomic situation improves.

Conclusion

Chase Corporation is struggling to maintain its gross margins given the increasing inflationary pressure. The company is trading at a P/E multiple of 18.20x, which I believe is a fair valuation for the firm, and the stock price has accounted for the negative market trend. I believe the company has weak growth prospects given the rising inflation in the economy. I recommend a hold rating for Chase Corporation after considering all these factors.

Be the first to comment