cemagraphics

It’s been about 4 ½ years since I wrote my “avoid” piece on Perdoceo Education Corporation (NASDAQ:PRDO), formerly “Career Education”, and in that time the shares have fallen about 15% against a gain of 36.25% for the S&P 500. I absolutely hate to write about the success of my call, so I’m not putting this in front of you this morning simply to brag, though that’s a pleasant enough byproduct. Today I want to review the name again to see if it now represents good value or not. Much has changed over this relatively long span of time, obviously, and a stock that’s trading at $14.50 is a much less risky investment than the same stock when it’s trading at $17. I’ll review the latest financial results, and I’ll review the valuation. I also want to write about options in this instance because I think there is an interesting, and (for me) surprising options “play” on this stock.

You’re busy, I’m busy, and so I assume that you’d prefer to get the “gist” of my thinking immediately so you can get back to scheduling routes on your large gauge model railroad or feeding your emus or whatever other thing you’re into. For that reason, I include a “thesis statement” paragraph at the beginning of each of my articles. You’re very welcome. Anyway, since I last looked at this company, it’s become consistently profitable, though it’s hardly a growth machine. At the same time, the capital structure is very strong, suggesting little risk of insolvency anytime soon. I’d be happy to buy this low growth business at the right price. In terms of the price, it is much better than when I last reviewed the name, though shares remain somewhat optimistically priced in my view. There’s a good chance that they’ll drop in price from here, though that’s certainly not inevitable. Given the above, I recommend buying the shares and writing covered calls against them. This is a strategy I employ only rarely these days, but I think it makes sense in this instance.

My Expectations

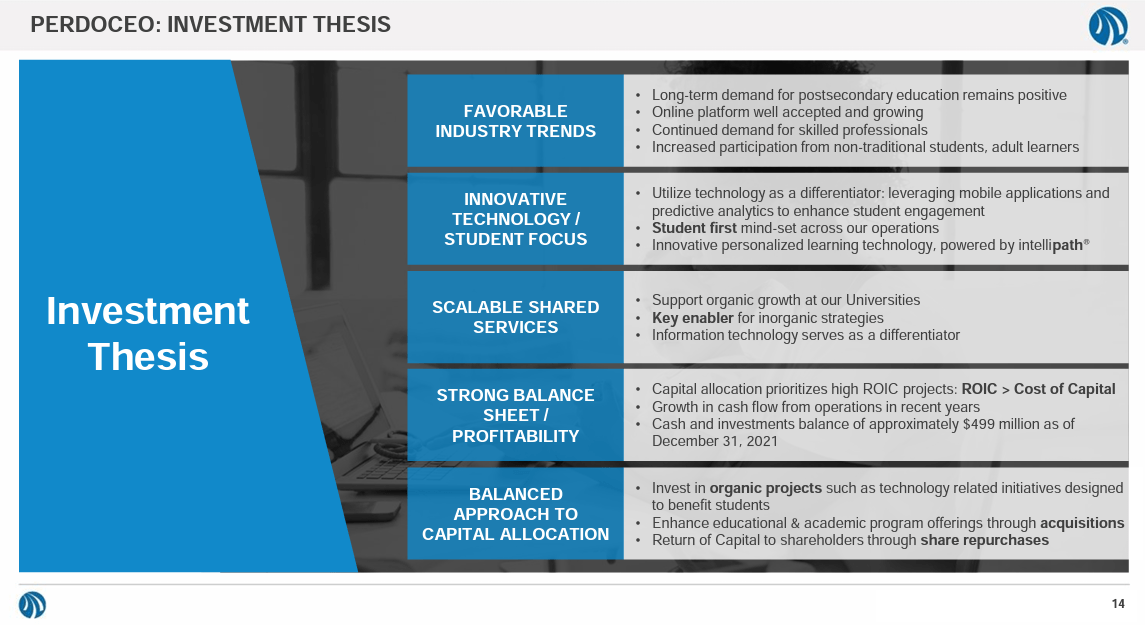

As they summarized in their latest investor presentation, and reproduced below for your enjoyment and edification, the company has a host of strong positive tailwinds that it should be able to take advantage of. It’s with that as a starting place that I want to review the financial history here.

Perdoceo investment theses (Perdoceo April 2022 investor presentation)

Financial Snapshot

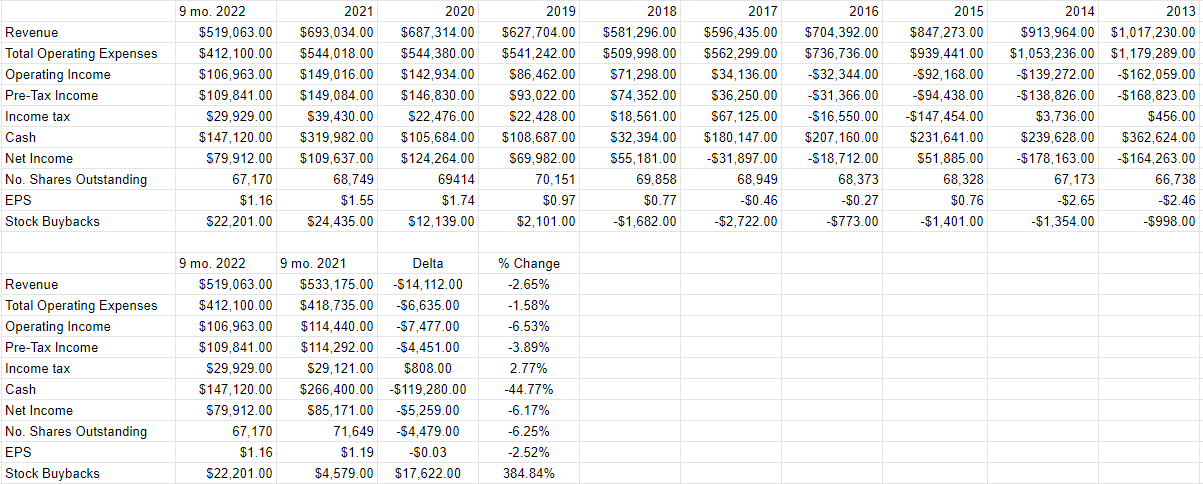

In my view, the financial history at Perdoceo is a bit of a mixed bag. On the one hand, growth has slowed fairly dramatically over the past while. In theory, this is because the company is concentrating on more profitable lines of business as very ably argued here. The problem, from my point of view, is that if it’s all about lower revenue and higher profits now, where are the profits? For example, net income in the first nine months of 2022 was down about 6% relative to the same period in 2021. We should also keep in mind that net income in 2021 was itself lower than 2020 by about $14.6 million, or fully 13.3%. Revenue, though, is higher. Thus, I wouldn’t characterise this as a “growth” business anytime soon, and I don’t think it deserves the valuation of a growth business. That said, the company has been solidly profitable since I last reviewed the name, so that’s a plus.

At the same time, it’s not all bad news at Perdoceo. The capital structure is fairly strong in my view, given that cash on hand represents about 76% of total liabilities. That, cooped with the ongoing profitability suggests that this is a “going concern” in the drab language of accountants, so I’d be happy to buy it at the right price.

Perdoceo Financials (Perdoceo investor relations)

The Stock

If you subject yourself to my stuff regularly, you know that I think the stock is distinct from the business in many ways. A business invests in a number of inputs, like new educational systems, adds value to those inputs by marketing to non-traditional adult learners, and then sells the results for a profit. The stock, on the other hand, is a traded instrument that reflects the crowd’s aggregate belief about the long-term prospects for a given company, and the stock is buffeted by a number of forces some of which may have little to do with the underlying business. Inflation may impact a business like this one significantly, as it might curtail the education budget of some of their potential students. The crowd may form a view about the relative attractiveness of stocks in general, and that drives shares up or down. Strangest of all in my mind, stock investors can be mesmerized by the pronouncements of Fed officials, as if the difference between a 50 and 75 basis point move in the overnight rate matters all that much.

Although it’s tedious to see your favorite investment get buffeted around for reasons having little to do with the health of the business, within this tedium lies opportunity. If we can spot discrepancies between the price the crowd dropped the shares to, and likely future results, we’ll do well over time. It’s typically the case that the lower the price paid for a given stock, the greater the investor’s future returns. This is why I only ever want to buy a stock that is relatively cheap, and it’s why I’m reconsidering Perdoceo. In order to buy at these cheap prices, you need to buy when the crowd is feeling particularly down in the dumps about a given name.

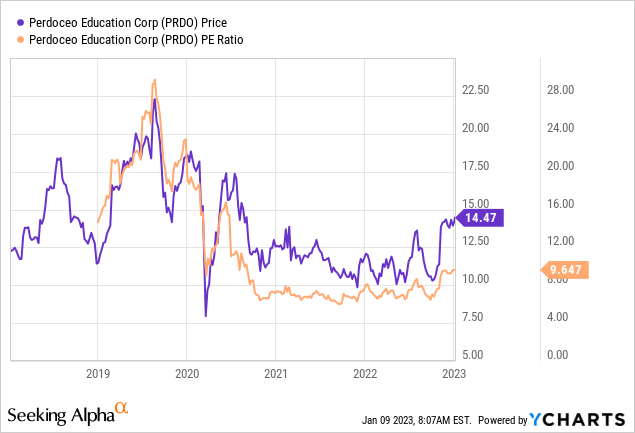

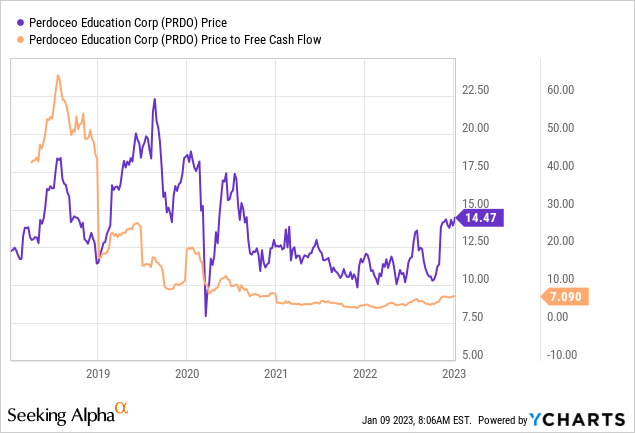

As my regulars know, I use a host of measures to judge the relative cheapness (or not) of a given stock, some of which are quite simple, some of which are quite sophisticated. On the simple side, I like to look at the ratio of price to some measure of economic value, like earnings, sales, free cash, and the like. Because I think “cheaper wins”, I want to see a company trading at a discount to both the overall market, and the company’s own history. In case you’ve forgotten, I eschewed Perdoceo (then called “Career Education”) when it was trading at a price-to-free cash flow ratio of about 60.4 times. Fast forward several years, and profitability is consistent and the valuations are much more reasonable looking per the following:

Source: YCharts

Source: YCharts

Taking into account the newfound consistent profitability, the strength of the capital structure, and the cheap valuation, shares of Perdoceo are rather compelling at the moment. For that reason, I’m considering a long position with this stock.

In order to validate (or refute) this view, I want to try to understand what the crowd is currently “assuming” about the future of a given company. If you read my articles regularly, you know that I rely on the work of Professor Stephen Penman and his book “Accounting for Value” for this. In this book, Penman walks investors through how they can apply the magic of high school algebra to a standard finance formula in order to work out what the market is “thinking” about a given company’s future growth. This involves isolating the “g” (growth) variable in this formula. In case you find Penman’s writing a bit dense, you might want to try “Expectations Investing” by Mauboussin and Rappaport. These two have also introduced the idea of using stock price itself as a source of information, and then infer what the market is currently “expecting” about the future.

Applying this approach to Perdoceo at the moment suggests the market is assuming that this company will grow at a rate of about 4.5%. I consider this to be fairly optimistic, actually. This disagreement between ratios and assumptions puts me on the horns of a dilemma. I want to buy the shares at current prices, but there’s a very good chance that they’ll drop from here, in the short run at least. If only there was a way to “play” this stock more safely. It should come as no surprise that thankfully the options market offers a viable alternative for me.

Options as Alternative

My regular readers know that I’m a fan of selling put options, preferably deep out of the money put options. I’d like to do that in this circumstance too, but the problem is that the premia on offer are too thin. The July put with a strike of $10, for instance, is currently bid at $0. Zero is too little a return in my estimation.

I don’t want to be too dogmatic in my thinking, though, so in this case I would recommend a different approach than usual. Today I would recommend buying shares of Perdoceo, while simultaneously writing calls against them. In particular, I’m a fan of the July call with a strike of $15, which is currently bid at $0.40. That means that a call that’s about $0.50 out of the money at the moment would net the investor a yield of about 2.7% on their capital for six months of, uh, let’s call it “work.” This annualizes to a rate of about 5.6%, which I consider to be quite good. The shares may fall from here, but the covered call lowers the net adjusted cost base of the investment, and therefore the risk.

In case you’re not aware, I think it would be helpful if I describe some of the risks associated with this approach. One is emotional in nature, and one is financial.

The emotional risk involves missing out on upside if the stock spikes in price. When you write a call, for the duration of the option, your returns are capped at the premium received plus the delta between your purchase price and strike price. So if the shares skyrocket to, for example, $30 per share, the call writer’s return is limited to $0.40 for the call premium plus ~$0.50 for the delta between price paid today and strike price. In my view, that 6% return in six months would be very acceptable, but it is definitely emotionally painful when the stock soars well above the strike price.

The financial risk involves the fact that the covered call offers only limited downside protection. The shares may tank, and the income earned on the call cushions this blow somewhat but still produces economic pain.

If you understand and can tolerate these risks, I would recommend buying these shares and immediately selling the July call with a strike of $15 as a way to generate some immediate income.

Be the first to comment