Angela Gonzalez/iStock via Getty Images

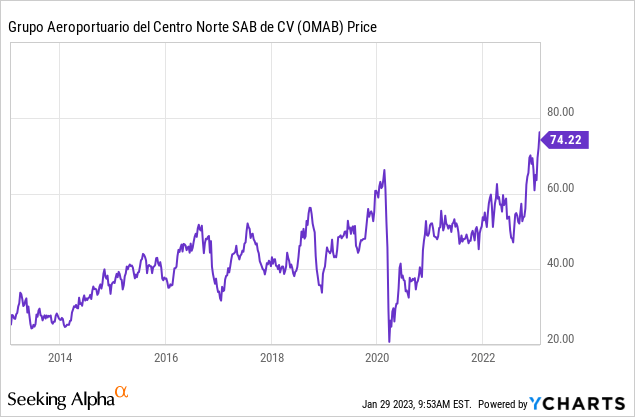

Mexican airport operator Centro Norte Airports (NASDAQ:OMAB) is on a hot streak, with shares rising 45% over the past year. The stock is currently at new all-time highs, and has moved above its prior Covid-19 peak with ease:

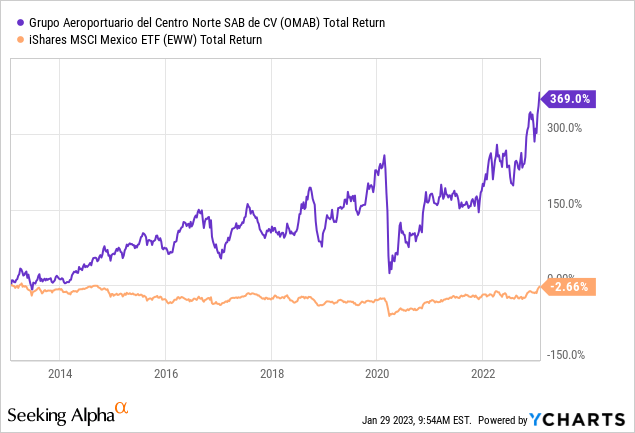

Centro Norte’s performance is even more noteworthy when considering that the company typically pays a 5% or greater dividend yield on top of its share price gains. This gets particularly impressive when compared against the Mexican stock market (EWW) as a whole:

Over the past decade, Centro Norte has returned 369% for its shareholders, meanwhile the Mexico ETF is down 3% over the same period. It makes you realize that once the Mexican stock market has a bull run, the airports could really lift off.

Why Centro Norte Is Well-Suited To Lead The Next Mexican Bull Market

I’m getting ahead of myself, though. Let’s review what’s gotten Centro Norte to its present heights, and why I believe shares have considerable upside ahead.

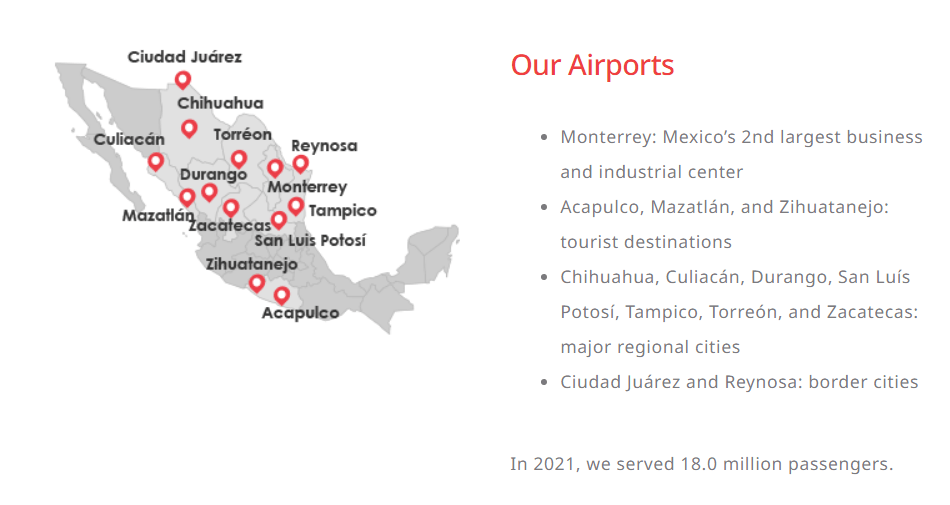

OMAB’s airports (Corporate presentation)

The Monterrey airport is the key asset, with it accounting for roughly half of the company’s total passengers and EBITDA. Monterrey’s urban area has grown from less than half a million people in 1950 to more than five million today. It continues to add roughly 75,000 new people to its metro area every year. Monterrey is also the capital of the most prosperous region in Mexico. On a purchasing-power-adjusted basis, the Monterrey area is already wealthier than several of the United States’ 50 states.

For the airport specifically, Monterrey has grown from 3.5 million passengers per year at the turn of the century to an annualized pace of approximately 12 million passengers today.

In addition to the domestic market, Monterrey has seen route growth to various American industrial cities such as Detroit. It’s only logical to have direct flights from the automakers’ HQs to their primary manufacturing plants in Monterrey. In addition to a burgeoning U.S. market, Monterrey also has direct international flights to other countries, including Panama and Spain.

Following Monterrey, most of the rest of Centro Norte’s value is in its other airports serving industrial cities near the U.S. border. These include cities like Ciudad Juarez, Chihuahua, and Reynosa. As manufacturing continues to boom in Mexico, these cities that are particularly near to Texas, Arizona, and other growing American economic regions should particularly benefit. Every time you hear about a new $20 billion semiconductor plant going up in Dallas or Phoenix, just think about all the basic electronic, packaging, and other input goods which will be made just over the border in Mexico to support those new plants.

Centro Norte does have a few airports in beach cities. However, these are either past their prime, like Acapulco, or are not yet prominent tourist destinations, such as Zihuatanejo. As such, Centro Norte is an almost pureplay on the growth of Northern Mexico, which is driven by industry and manufacturing. With Mexico enjoying a boom in foreign direct investment and manufacturing activity, Centro Norte is perfectly situated to cash in on this development.

Further to that point, I’d note that both the major highways and railroad running to Texas pass through Monterrey, making it a logistics hub for trade between Mexico and the U.S. This, in turn, drives additional demand for the airport.

Traffic: Still Booming

Centro Norte has already released its full-year 2022 traffic statistics, shown below:

OMAB’s 2022 traffic figures (Company press release)

For 2022 as a whole, traffic leaped 29% from 2021 levels. Meanwhile, traffic was up 21% for December 2022, year-over-year. The fact that traffic is still growing at a more than 20% annualized rate should speak to the fact that we’re experiencing a secular growth trend for Mexican industry, this is far more than just a Covid-reopening phenomenon.

Further to that point, Centro Norte served 2.0 million passengers in December 2019, whereas it is now up to almost 2.3 million passengers for the same month in 2022. Traffic is now running close to 115% of pre-pandemic levels and is growing at a 20% annualized rate. It’s not just rising load factors either; airlines are adding new routes to Centro Norte’s airports. In December, for example, they picked up six additional routes including an attractive Los Angeles-Monterrey route from Aeromexico.

Profit margins have also ticked higher. All this to say that Centro Norte is worth a lot more today than it was in 2019 thanks to the improving traffic numbers, profitability, and manufacturing outlook for Mexico going forward.

The Bottom Line

Centro Norte isn’t at a knockdown dirt-cheap valuation anymore. The market has started to wake up to the tremendous manufacturing/reshoring story that began playing out a few years ago. Valuations have started to approach more reasonable levels for many Mexican assets.

However, we were starting off such an absurdly low base that Mexican asset prices today still represent excellent value. Here are Centro Norte’s numbers today, for example:

OMAB valuation metrics (QuickFS)

Centro Norte is now trading at 21x trailing earnings and 14x trailing EBITDA. This is about in line with its 10-year historical norms; Mexican airports, for example, have run a long-term median multiple of approximately 15x EV/EBITDA.

However, 21x earnings and 14x EBITDA is hardly expensive for this business. It has, after all, grown earnings at more than 12%/year compounded and free cash flow at a sizzling 17%/year compounded over the past decade. And that was a decade, which, I’d remind you, included a brutal Mexican equity bear market and sluggish economy, and then a global pandemic. Passenger traffic (and thus EPS and EBITDA) are currently growing at more than 20%, after all.

Judging from the last two years, Centro Norte is going to post much stronger growth figures in the 2020s than it did in the 2010s. And yet, the market is still offering us this opportunity at a downright reasonable starting valuation. To add further to that point, shares offer a roughly 5% dividend yield at today’s entry point. Sure, the stock yielded even more than that last year, but it’s still attractive. Especially in light of the balance sheet, which has minimal leverage.

A lot of people are probably going to look at the Mexican airports, now up close to 50% over the past year, and say they missed the ride. Whereas, I’d counter, Mexican stocks had been in a bear market since 2013. Now that a new bull market has finally begun, leadership can continue for a long time.

I have little interest in cashing in Mexican assets, including Centro Norte stock, in the second inning of what should be an extended bull market. With earnings and free cash flow growth accelerating, OMAB stock remains a great investment, with shares a touch below its median historical valuation.

Be the first to comment