bjdlzx

(Note: This article was in the newsletter on August 9, 2022.)

(Note: This is a Canadian company reporting in Canadian dollars unless otherwise noted.)

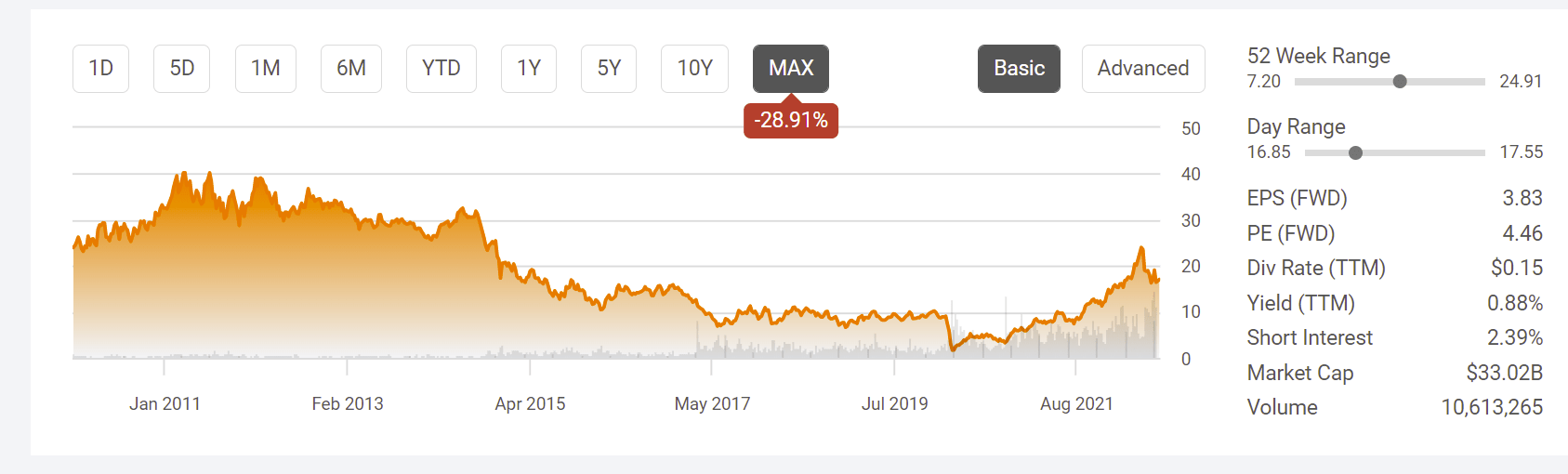

Cenovus Energy (NYSE:CVE) was once a subsidiary of what is now Ovintiv Inc. (OVV). The former Encana spun off the company back in 2009. The primary asset of Cenovus at the time was a partnership with ConocoPhillips (COP) that Encana management believed was noncore and really had a less than desirable future. More importantly, Encana management wanted to focus on what it thought were the best assets at the time with more profit potential. As shown below, the stock price began trading at optimistic prices commensurate with the thinking at the time that high oil prices would only go higher.

Cenovus Energy Common Stock Price History And Key Valuation Measures. (Seeking Alpha Website August 9, 2022.)

As shown above, by most measures, the spinoff was a success because the stock price initially rose to give many investors a chance to take profits.

But no one saw 2015 coming. When it did, the thermal partnership with ConocoPhillips was largely seen as a “dog” by many in the industry because everyone “knew” that the thermal business was relatively high cost and prices were now rock bottom. The thermal product was a discounted product at the time of low prices. So, the stock price action shown above was no surprise despite the company possession of some refining capacity to raise the value of some of the production.

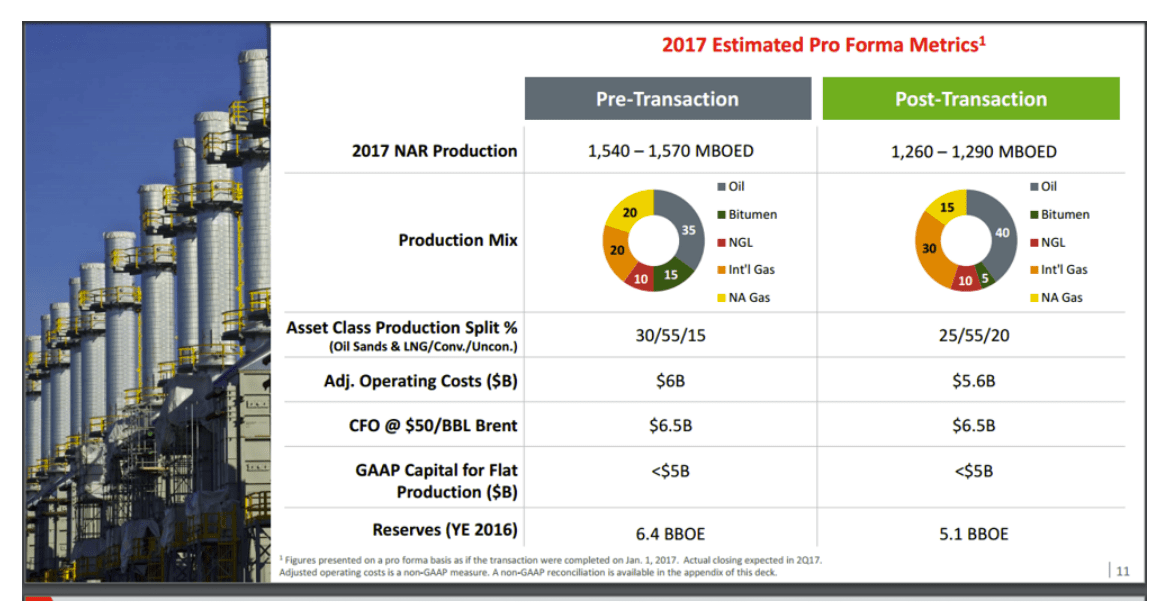

ConocoPhillips Sale Of Partnership

Then in 2017, management took advantage of a gift. ConocoPhillips sold the interest in the thermal partnership to Cenovus Energy at some of the lowest oil prices around.

ConocoPhillips 2017 Presentation Of Partnership Sale To Cenovus Energy (My Article “The Clock Struck 12, So ConocoPhillips Sold A Pumpkin”)

ConocoPhillips presented the sale as a great way to cash in on something that was not generating a lot of cash. The reason management could state that there was not a lot of cash generated was ConocoPhillips management only used partnership distributions received by ConocoPhillips (not profits or partnership cash flow) in the presentation. So, distributions basically covered interest and not a lot more.

But ConocoPhillips as a partner had to have approved several capital projects that were underway (using cash that could have been distributed) at a time when commodity prices were low. Probably the safest time to expand operations is when commodity prices were low. Therefore, cash generated by the partnership was not quite as low as management presented because management had elected to spend some of the generated cash on growth projects. In succeeding articles, I covered these projects as they completed.

Cenovus Energy also received a large position in the great basin that was largely producing natural gas at the time. Cenovus Energy management has spent the last few years looking at the possibility of liquids rich drilling. In the meantime, that natural gas production is now worth many times what Cenovus Energy valued it back in 2017 because natural gas prices are far higher. (As an aside note: that business by many was considered self-financing back then. Imagine what it is considered now.)

Prices began firming in 2017 to the point that cash flow from operating activities had more than doubled by the August 2017, second quarter report. There would be more cash flow “doubles” comparisons as management sold assets to reduce acquisition debt while completing capital projects the partnership undertook to grow production over the next few years.

Husky Merger

Management had long realized that thermal upstream does far better if the product is upgraded to valuable end-market products rather than letting someone else do it. Husky (OTCPK:HUSKF) was acquired in October of 2020.

This follows the similar pattern of an acquisition at the beginning of a market recovery while industry pricing was still weak. In theory, it is hard to overpay for acquisitions made near market bottom because the coming recovery will lead to rising commodity prices that often make these deals look good for several years. That appears to be the case here.

Stock Price Action

Notice that despite debt reduction efforts and the benefits of downstream diversification (not to mention possession of a fair amount of midstream assets), Mr. Market concentrated on one bad news item after another to keep the stock in the doghouse. The way the stock was performing, one would have thought finances were going down the drain. It was the exact opposite view from when the stock went public. That makes knowing where you are in an industry cycle extremely important. There is only one thing that happens when the “good times” prevail in a cyclical industry just as there is only one thing that happens when the “bad times” prevail in a cyclical industry.

Generally, Mr. Market assumes that good times will prevail (as he did after the spinoff) and that bad times will prevail in the future (he did for several years after the partnership acquisition despite rising cash flow).

Now And The Future

The big difference going forward is that Cenovus is no longer handicapped by a bunch of partnerships as it was when it was spun off from Encana. At that time the company was nearly all partnerships. Even if the company is the operator, partners still have to agree, or things do not get done.

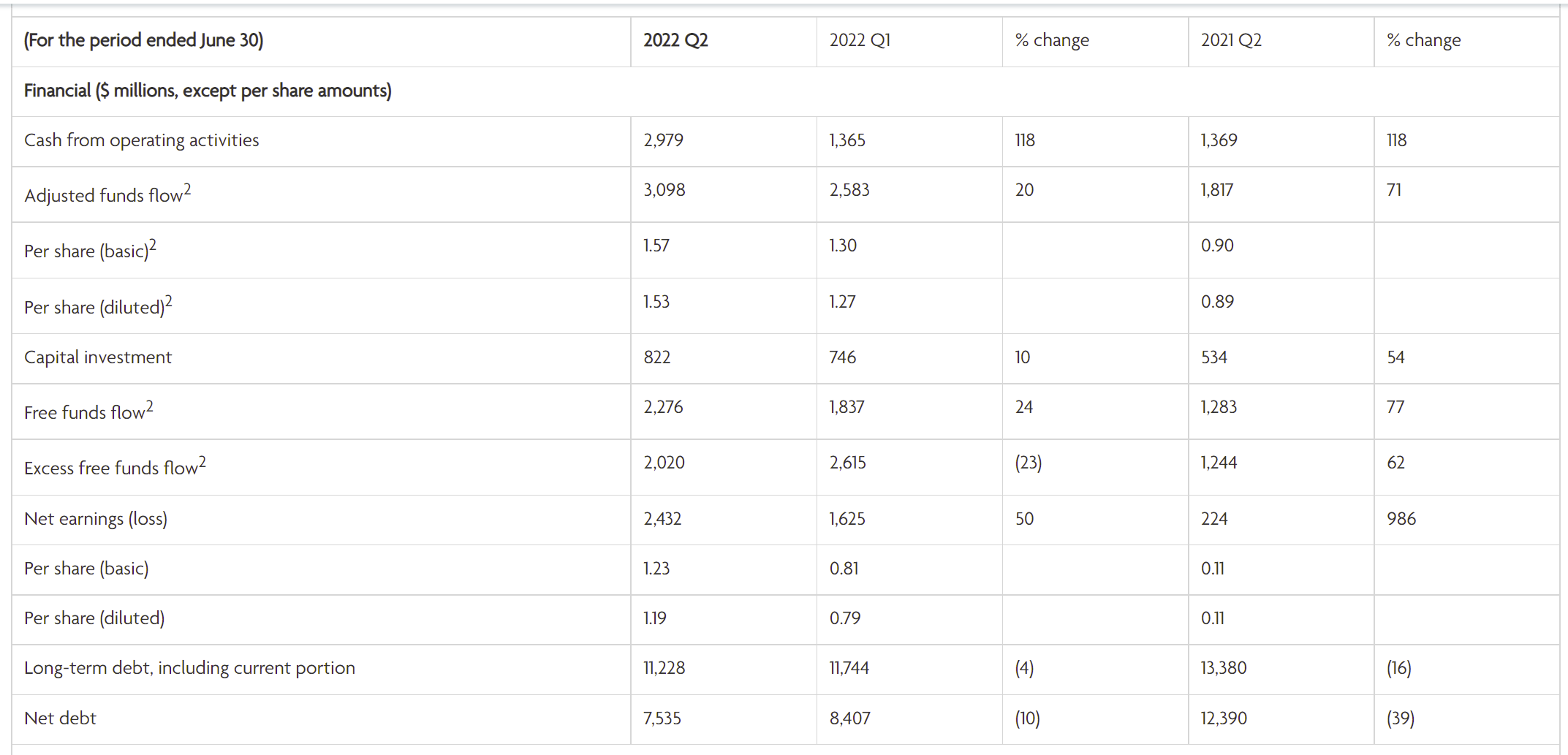

(Canadian Dollars Unless Otherwise Stated)

Cenovus Energy Summary Of Operating Results Second Quarter 2022. (Cenovus Energy Second Quarter 2022, Earnings Press Release.)

Cenovus Energy clearly has improved cash flow even though selling prices are considerably better than they were back in 2017 when the company acquired the partnership interest. I noted in my article back then that cash flow from operating activities was roughly C$300 million (before the acquisition) in the first quarter of 2017. The adjusted funds flow above is much better than rising prices can account for and points to the wisdom of the strategy employed by management since that large purchase.

The market attitude for the outlook of oil and natural gas has improved tremendously since management began the current strategy. Clearly management has the company positioned to take advantage of that outlook.

Furthermore, management is still buying bargains. They recently agreed to buy a 50% interest in a refinery that they will now own solely. This came after an agreement to enlarge an interest in a thermal property. Typically, this management goes in and modernizes as needed while cutting costs. The latest purchases should be no different.

What may take a while is the changeover of feedstock for the Husky refineries to Cenovus product as contracts expire. Cenovus has some industry leading costs to produce thermal oil. Those low costs are likely to widen the refining margins over time compared to the purchases made when Husky was independent.

As far as profit history comparisons can be made, it is extremely clear that the future is going to be far more profitable for this company than the past was. Partnerships can be a major profit headache. This company has demonstrated since 2017 that it can run things far better alone than in a partnership. Going forward, there are still some partnerships. But there is nothing close to the situation at the time of the spinoff from Encana.

The market has yet to realize this. On the other hand, it is also clear that the stock is coming out of the doghouse. The market will want to see the newly integrated company results before assigning a regular value to the stock. But that should not take any extraordinary effort by management. That makes this stock a bargain for a wide variety of shareholders that want to invest in an integrated company because the downstream and midstream assets offset some of the upstream profit volatility.

The thermal business is now far less exposed to market pricing because the company continues to expand its presence in the refining (and upgrader) business. That is going to help profits tremendously in the future. By most accounts, the refining business effectively upgraded about 25% of production back in 2017 after the purchase of the ConocoPhillips interest. Clearly after the latest purchase of refining interest, the majority of production will now head towards one method or another of upgrading or refining.

That makes this company the latest to join the integrated majors. All shareholders have to do now is wait for the shares to be valued like the other integrated majors.

Be the first to comment