courtneyk

Thesis

CCC Intelligent Solutions Holdings Inc. (NASDAQ:CCCS) is a leader in automotive estimating software, which is mission-critical for insurance carriers and auto repair facilities. The business is well-positioned to achieve the top-line growth profile of 7-10% in the long-term, with 40% medium-term margins. I believe the company’s current valuation is in line with peers and see very limited margin expansion potential from current levels. I keep a December 2023 price target of $11 on the stock with an assumed forward CY24 EV/EBITDA multiple of ~20x, in-line with the company’s historical forward EV/EBITDA multiple.

CCCS stock price movement over the past year (Seeking Alpha)

Why I Keep a Hold rating on CCCS?

CCCS is a leading provider of estimating software for auto insurers and repair facilities

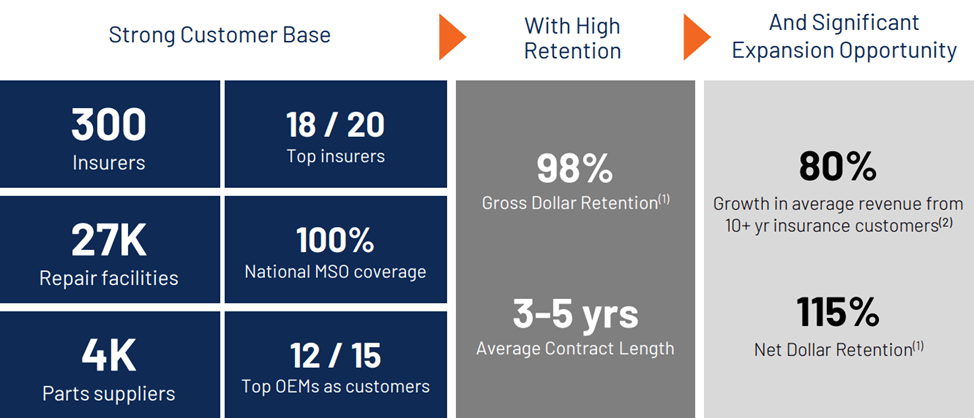

CCC’s core offering is estimating software for automotive physical damage, which helps give insurers and repair facilities the tools to estimate the costs of repair accurately. The reason this is important is estimates drive claims, which is the main expense for insurers, but also the main experience for the insured customer. For insurers, CCC provides different regional parts/labor rates specific to the car make/model, allowing them to give an accurate estimate at a time when the costs of repair are growing faster than historical levels as cars become more complicated with technology. Furthermore, a more accurate estimate is not inflated, reducing leakage, which CCC estimates to be a $50 billion annual expense to the global insurance industry. For the insured customer, the experience with a CCC-based ecosystem is more seamless- more carriers operate direct repair programs with repair shops that allow customers to receive quicker, accurate estimates and expedite the time to getting their vehicle back or getting compensation in a total loss scenario. I believe CCC is adding value to both the carrier and the repair facility, which is why it counts 18 of the top 20 US insurance carriers and ~27k of the ~40k repair shops in the US as customers, making it the leading vendor in the United States.

Sticky customers with long-term contracts and high gross retention rates

CCC’s mission critical tools, its blue-chip insurance carrier base, and established base of repair facilities drive long-term engagements with high gross retention rates. Specifically, I believe CCC’s insurance carrier customers have average contract durations of 3-5 years, while the repair facilities have average contract durations of 3 years – in many instances customers in both segments have renewed multiple times over CCC’s 40-year life. Most importantly, I see this from the dollar perspective as well, with the gross retention rate of ~98% showing that CCC’s core tools and the strength of its end vertical support long-term engagements. In addition, I believe CCC has been able to command higher run-rates from existing customers, as shown by net retention rates (NRR) that have been in the 103-107% range over the last 3+ years. I believe CCC can at least maintain this NRR because of (1) growth from its core estimating tools through either pricing or additional volume; (2) new products that capture more wallet share from the carrier or repair shop. On the second point, I think two products could be particularly interesting, Estimate Straight-Through-Processing and Diagnostics. Estimate STP would allow carriers to use AI tools to examine images of auto physical damage, and come up with an accurate estimate without using a human adjustor in the process. Diagnostics would be a tool used by repair shops to more accurately diagnose problems with cars to also improve their estimates. With these new products and the strength of its core estimating tools, I think CCC can see ~110% NRR long-term, which would support most of its 7-10% long-term revenue growth target.

CCCS has a high customer retention (Company Presentation)

Years of proprietary automotive repair data and a tough competitive landscape make it difficult for new entrants in this market

There are at least two structural dynamics that create barriers to entry – (1) CCCS’ proprietary vehicle/repair/cost data; and (2) a tough competitive landscape. First and perhaps most importantly, CCC has been a technology leader in the P&C insurance economy for several decades and has processed over $1 trillion worth of transactions during its history. Through its transaction history, CCC has built up a large database that spans insurance claims, vehicle repairs, automotive parts, and other vehicle-specific information. In my view, CCC uses this historical data to give carrier and repair shop customers more accurate estimates no matter what the car or repair procedure, which is difficult to replicate by newer entrants or the internal databases of its customers.

CCCS Valuation is in-line, I see the current multiple difficult to expand in the long term

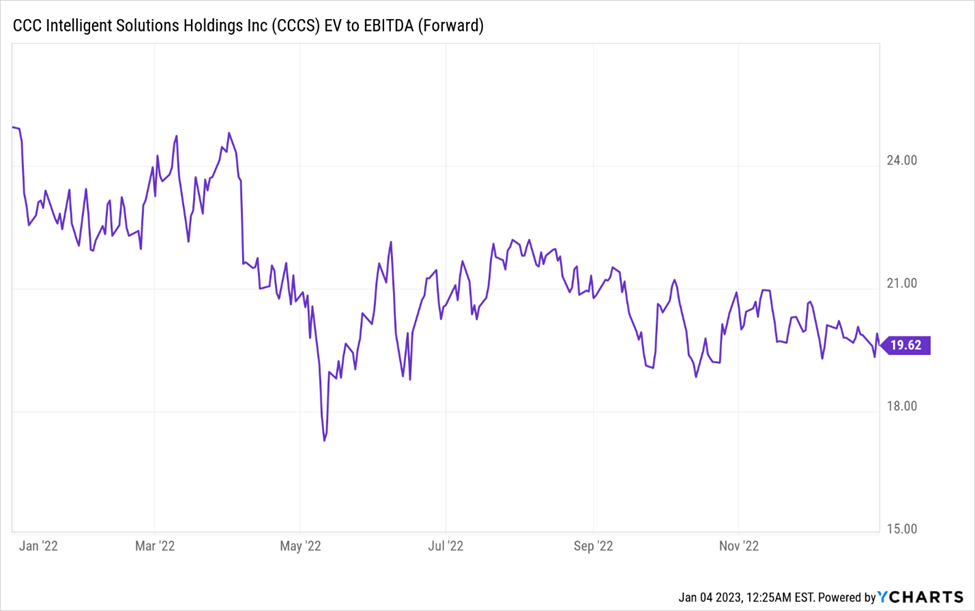

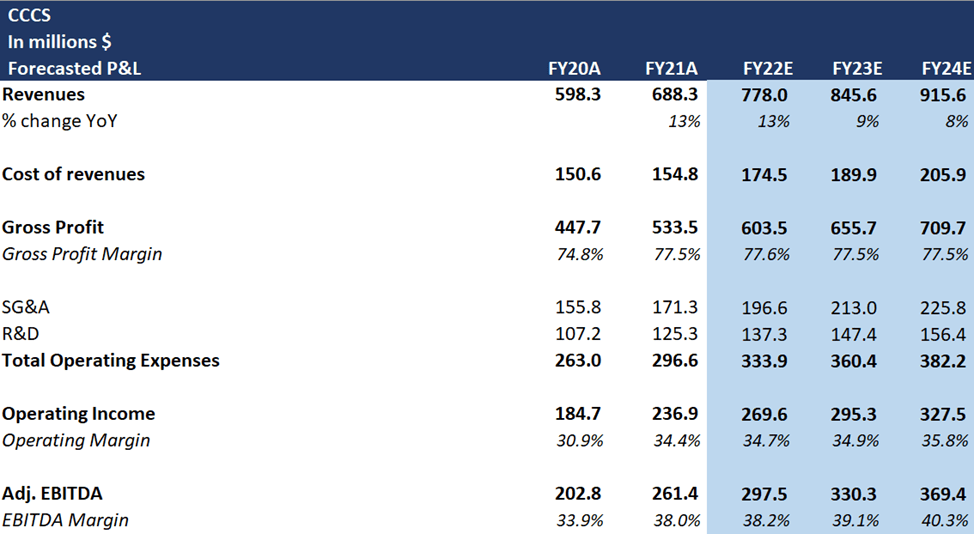

CCCS is a mature software business targeting 7-10% long-term revenue growth and ~40% EBITDA margins, so I believe valuation should triangulate across multiple metrics, where I see CCCS trading either in-line or at a slight premium to peers. Because the company manages to/guides to EBITDA, I believe more investors gravitate towards EV/EBITDA valuation – which is in-line with Verisk Analytics, Inc. (VRSK) and Cadence Design Systems, Inc. (CDNS), two comparables of the company. My December 2023 price target of $11 is premised upon ~20x CY24E EV/EBITDA, in-line with the company’s historical forward EV/EBITDA multiple.

CCCS Forward EV/EBITDA (YCharts) CCCS forecasted P&L (my estimates)

Final Thoughts

CCCS is a leader in auto estimating software for insurance carriers and repair shops, with 98% gross retention and barriers to entry. The company’s estimating software has a leading share with 18 of the top 20 auto insurance carriers and 27k auto repair facilities. CCC has a mature financial profile, and I see limited multiple expansion potential from current levels. I view EV/EBITDA as the main valuation metric to value CCCS, and my December 2023 $11 price target multiple works out to ~20x CY24E EBITDA, in-line with the company’s historical forward EV/EBITDA multiple.

Be the first to comment