Miro Nenchev/iStock via Getty Images

Note: I have covered Castor Maritime (NASDAQ:CTRM) previously, so investors should view this as an update to my earlier articles on the company.

Four weeks ago, junior Cyprus-based shipping company Castor Maritime reported respectable first-quarter results.

Despite Q1 traditionally being the weakest quarter of the year, rates for the smaller vessel classes held up well, thus resulting in the company reporting EBITDA of $27.9 million and $13.1 million in cash flow from operations.

While the average Time Charter Equivalent (“TCE”) rate of $17,809 doesn’t look great when compared to dry bulk peers, investors should note that the company also owns eight, fairly old crude tankers which pressured the average TCE rate in Q1.

That said, the company’s tanker exposure should benefit Q2 results after the Russian assault on Ukraine has caused charter rates to rally in recent months.

In January, Castor Maritime refinanced five dry bulk vessels with a European bank at a rate of SOFR +3.15% for net proceeds of $54.3 million.

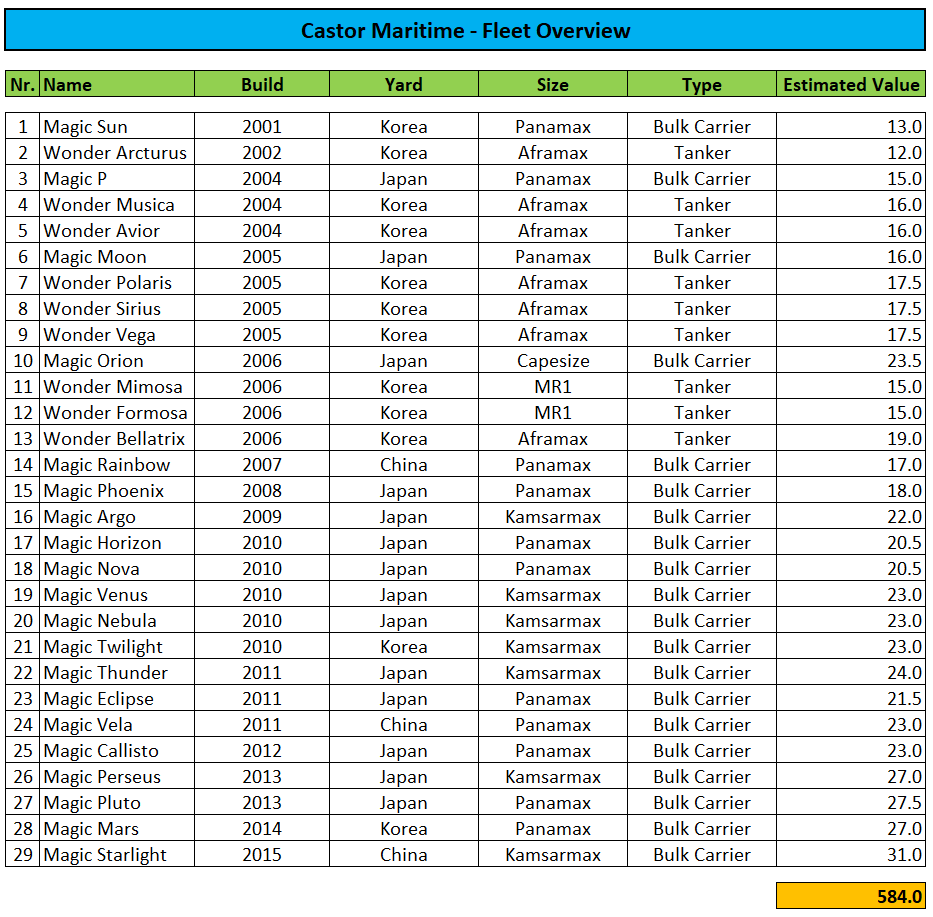

At the end of Q1, the company’s cash balance amounted to $84.0 million. Net debt amounted to $70.5 million or just 12% of Castor Maritime’s estimated fleet value of $584.0 million.

Company Press Release / Compass Maritime

In late March, the company reduced the maximum amount under its ongoing at-the-market common stock offering program (“ATM Program”) with Maxim LLC from $300 million to $150 million. So far in 2022, Castor Maritime has not utilized the ATM program which is currently scheduled to expire next week but is likely to be extended or replaced soon.

Last month, the company sold the 20-year old Aframax tanker Wonder Arcturus for gross proceeds of $13.15 million. The transaction will result in an approximately $3.8 million gain which should be recorded this quarter.

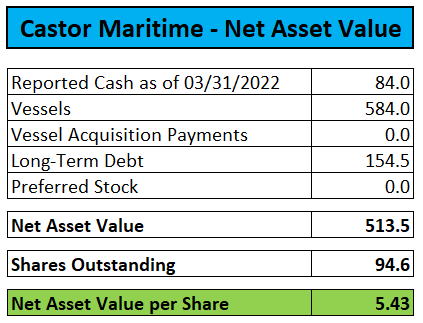

Company Press Release / Compass Maritime

Castor Maritime continues to trade at a large discount to net asset value (“NAV”) likely due to:

- The above-discussed ATM overhang.

- The company not paying a dividend like most of its peers.

- Castor Maritime’s past involvement in capital raising schemes to the detriment of common shareholders very similar to smaller peers Globus Maritime (GLBS), and OceanPal (OP).

- CEO, CFO and Chairman Petros Panagiotidis retaining full control of the company via supervoting preferred shares.

- A company controlled by the CEO’s sister is responsible for the technical management of Castor Maritime’s fleet.

-

A company controlled by the CEO is providing the commercial management for Castor Maritime.

In aggregate, the CEO and his sister managed to extract a whopping $13.2 million in management fees, charter hire commissions, administration fees and sale and purchase commissions during 2021.

Bottom Line

Castor Maritime’s shares appear inexpensive for good reason as investors remain wary of potential further dilution and related party dealings.

In addition, unlike most of its peers and despite a pristine balance sheet and plenty of liquidity, the company is not paying a dividend.

That said, with recent tailwinds from the company’s tanker exposure and substantially improved dry bulk charter rates anticipated for the second half of the year, I am keeping my “buy” rating on the shares for now.

Investors looking for a cheap, dividend-paying dry bulk shipper should consider an investment in Seanergy Maritime (SHIP). While certainly not flawless either, the company is trading at a more than 40% discount to NAV despite an estimated dividend yield of 13%.

Be the first to comment