Mlenny

This is a difficult article to write because we were expecting to remain Castellum AB (OTCPK:CWQXF) shareholders for many years, but we recently decided it was best to reallocate those funds into another opportunity. We still believe Castellum AB shares to be undervalued, and that they have a good likelihood of recovering, but we like the risk/reward profile of Deutsche Post DHL (OTCPK:DPSTF) a lot more, which is where we reallocated the capital.

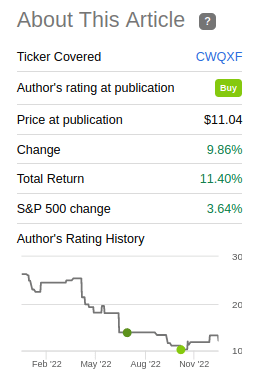

In our last article, we pointed out that while Castellum’s valuation remained very attractive, risks were already mounting. Since then the dividend was put on pause in mid-November, the CFO Maria Strandberg stepped down shortly after, and the CEO Rutger Arnhult left in mid-December. Despite all this turmoil, shares are actually a bit higher than they were when we wrote our last article in late October, showing that the low share price was already discounting a lot.

Seeking Alpha

We believe there are still a lot of things to like about the company, but we now consider it to be a very high risk investment. With the dividend paused, there is also less incentive to wait for things to improve, especially when there are similarly undervalued opportunities with a more attractive risk/reward profile.

Things still going well

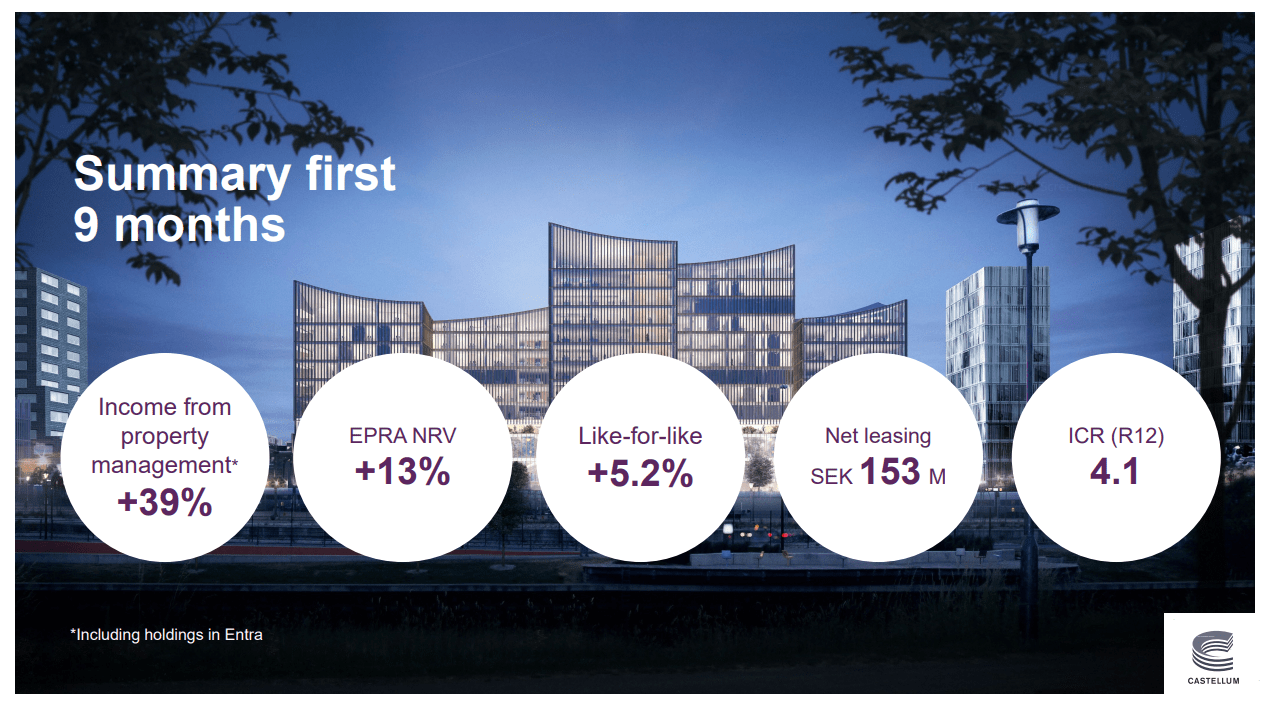

Operationally, we believe the company is still performing well. It has experienced positive net leasing for the eleventh consecutive quarter, its rental income like-for-like was 5.2% in the first nine months, the occupancy rate remains at a reasonable level of 93.4%, and 99% of its leases are index linked. The company is arguably not too leveraged either, with a loan-to-value of 38.8% and interest coverage ratio of 4.1x.

The company also has some projects coming online that should add valuable cash flows. Projects with rental values of SEK 183 million should have been completed by the end of last year, and SEK 280 million during 2023.

Castellum AB Investor Presentation

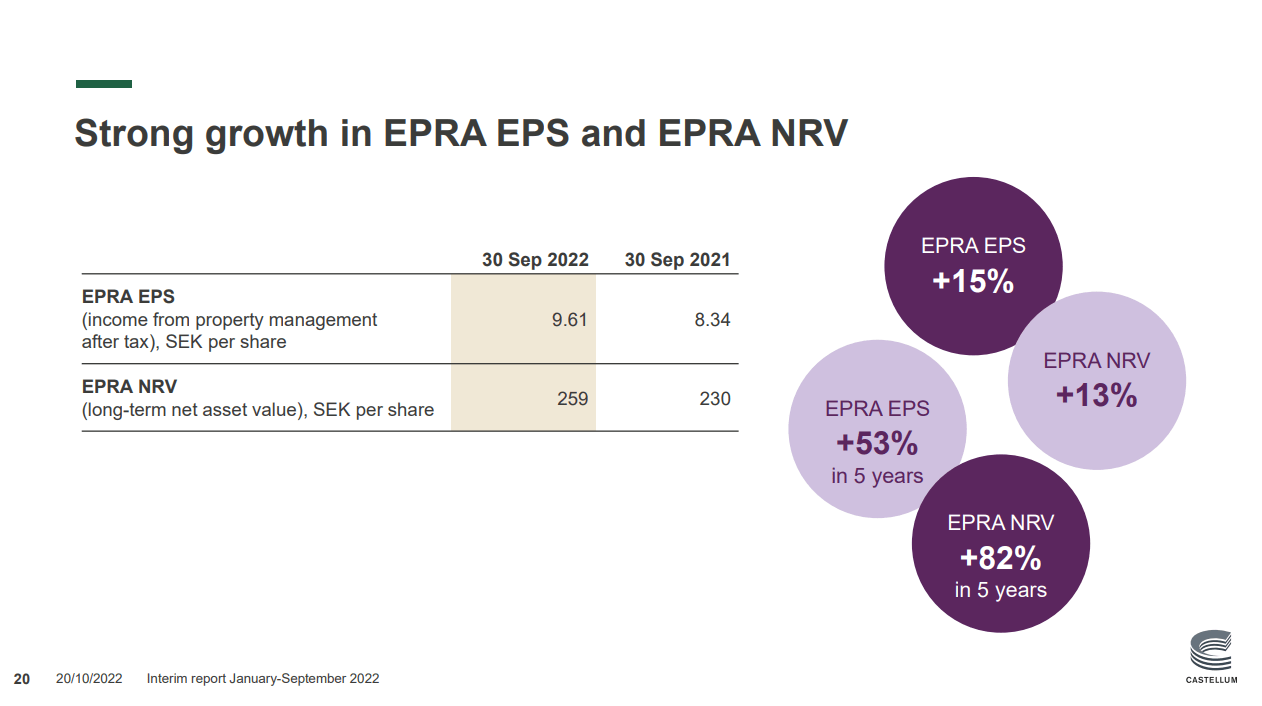

Despite the numerous issues, the company managed to increase both earnings per share and book value, as can be seen in the table below. For these reasons, we believe the company is still performing relatively well operationally.

Castellum AB Investor Presentation

Where we have some concerns

There are some areas where we have some concerns, such as Castellum making a big investment in Norway based Entra ASA (OTCPK:ENTOF). Entra is focused on office properties, and we believe this investment was probably a mistake for Castellum. Castellum’s share in Entra represents ~15% of its property value. Shares of Entra have not exactly been making new highs recently, and we found its recent results very disappointing.

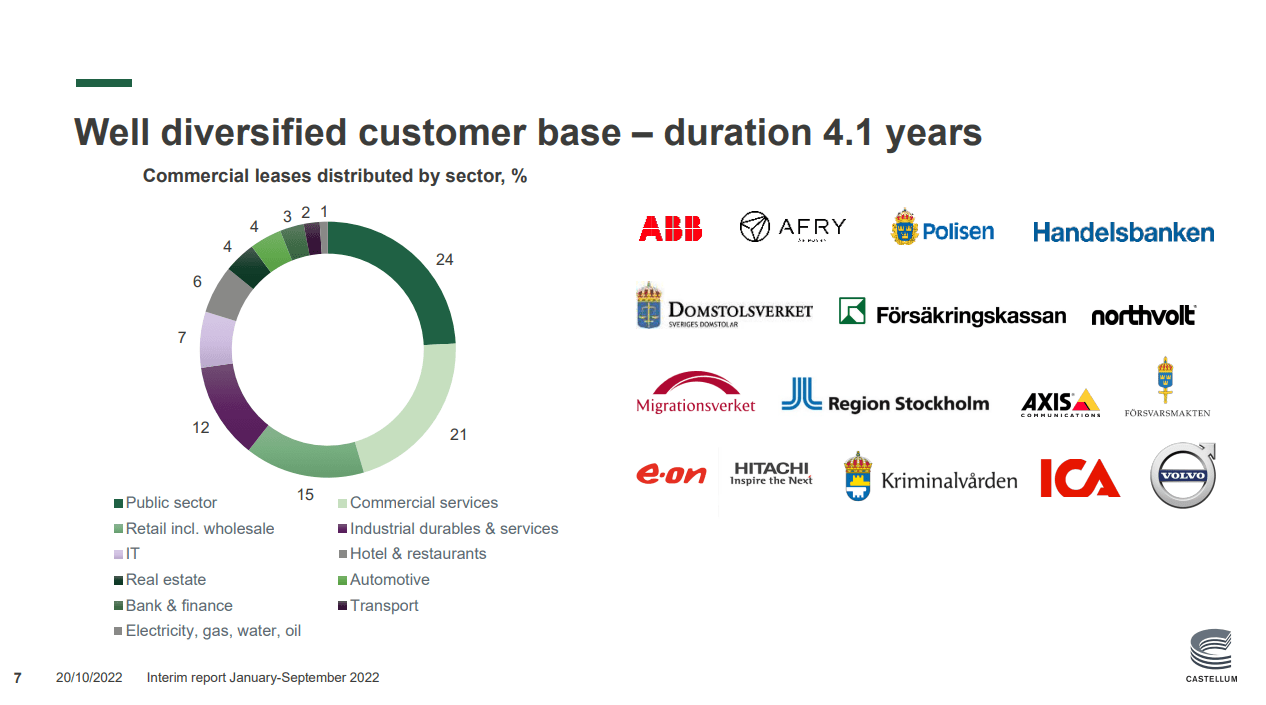

We also have concerns regarding the average lease duration of 4.1 years. Despite having a big list of blue-chip customers, we believe that lease duration is not long enough and that poses a risk, especially if many of them decide to reduce the space they lease due to reduced needs as a result of the work-from-home trend or economic weakness.

Castellum AB Investor Presentation

The Big Challenge

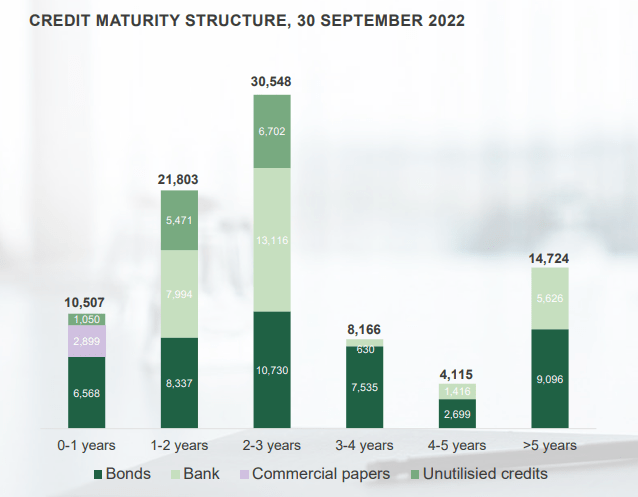

The big issue we have with Castellum is its credit maturity structure, with a lot of debt coming due in the next few years. We are worried as to whether Castellum will be able to refinance on good terms, especially given that the bond market remains challenging with historically high spreads and low liquidity.

The company is trying to reassure investors, saying it has SEK 15.3 billion in cash and unutilized credit facilities, covering all bond maturities during 2022-2023. It also had written credit approvals of ~SEK 6,200 million from Nordic banks which were expected to be signed in Q4 2022. The company is planning to use SEK 2,000 million for refinancing short-term bank debt.

In any case, we believe the average term of 3.2 years (3.9 including non-signed but credit approved financing) is too short and poses a serious refinancing risk if market conditions get worse by the time the company needs to access the credit market. The rising interest rate environment adds even more risk to the equation.

Castellum AB Investor Presentation

Valuation

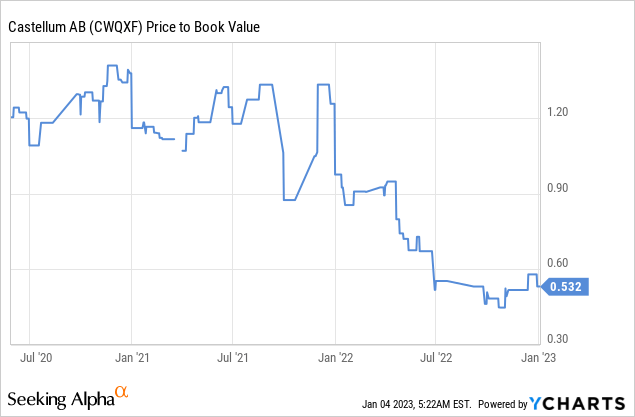

One thing shares still have in their favor is an attractive valuation, with the stock trading at roughly half of its book value per share. We believe this gives investors some margin of safety, and we believe shares have a decent chance of recovering if the refinancing risk is properly addressed.

Risks

What is very important to keep in mind is that Castellum AB is now a high risk investment, with the dividend paused and both the CEO and CFO departing. The real estate market is also currently facing some headwinds, particularly the office segment, due to the work-from-home trend. To complicate things further, the bond market remains challenging, and interest rates are on the rise. There are concerns too about a potential recession on the horizon, which could further impact the company’s financial performance.

Conclusion

We decided to sell our Castellum AB shares, mostly because we found another opportunity that we believe has a better risk/reward profile, but also because we now consider Castellum to be a high risk investment. There are still many things to like about the company, and it has been performing relatively well operationally. There are a few other areas where we have some concerns, but that we don’t consider dealbreakers, such as the Entra ASA investment. What we consider the big issue facing Castellum is its credit maturity structure, with very significant amounts of debt maturing in the next few years, which is not great given that the bond market remains challenging. Shares remain undervalued, trading at roughly half of its book value, but investors should weight the risks against the potential rewards given the current situation.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment