ipopba

Thesis

Stocks in the technology sector have a tendency to go through up and down cycles and it’s not a sector known for its consistency. Investing in the sector can also be fraught with challenges and so many times you buy into a dream. If you get lucky you are richly rewarded. But when I was looking at Cass Information Systems (NASDAQ:CASS) several things stood out to me and for a small cap stock, I was amazed in how differentiated it was in all these aspects –

- Stable and steady, top and bottom line growth with a squeaky clean balance sheet

- A business that is resilient even during recessions

- Consistently rewards shareholders

- Extremely low correlation to the index

Let us dive into each of these further in my analysis.

Company overview

Cass Information Systems is a payment and information processing service provider to large enterprises in the US (Its services include freight invoice rating, payment processing, auditing, and transportation information generation). Cass also processes and pays for facility-related invoices, including electricity, gas, waste, and telecommunications expenses. Cass Commercial Bank is a subsidiary of the company and supports its payment operations. It also provides banking services to privately-owned businesses and non-profits in selected cities in US.

A dumbed down version of my understanding on what Cass does is that it basically helps big companies pay their bills and keep track of their money. They also help people who run non-profits with their giving and has its own bank to help with all of these services.

Cass’s customers (Company Investor Presentation)

Past performance and its resilience

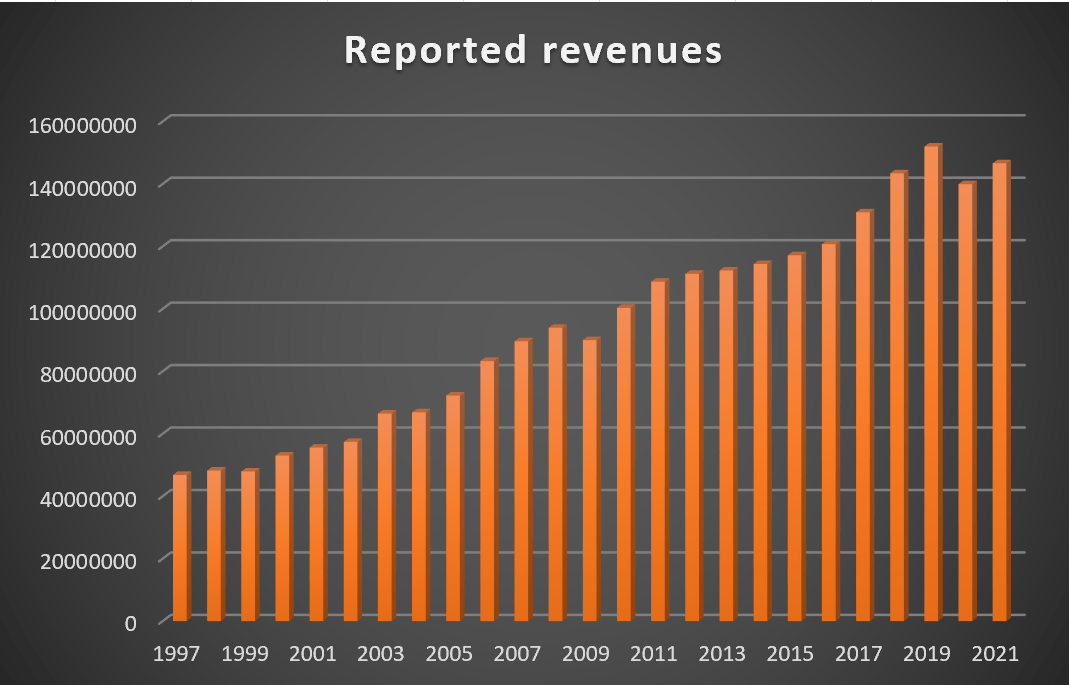

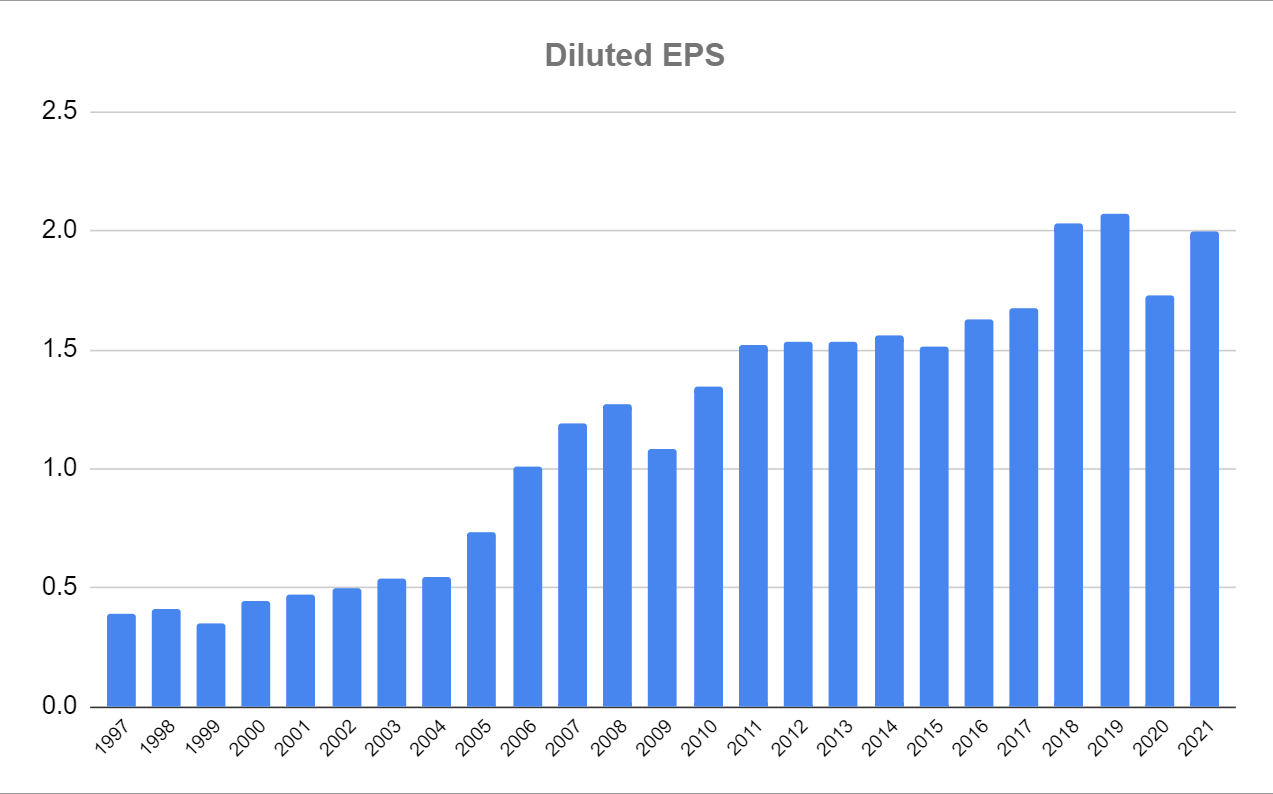

What I like most about Cass is its consistency. They have managed to grow revenues for 22 out of the last 26 years. Their worst year for growth was 2020 where revenues dipped by 8% closely followed by 2009 where revenues dipped by 4%. Earnings per share also shows a similar trajectory where their worst years were 2020 (-16%) and 2009 (-15%)

Author generated from Financial Modelling Prep

Author generated from Financial Modelling Prep

This resiliency in their performance can probably be attributed to the nature of their business. Even though they are in the technology sector, the businesses they serve are distributed across different segments. Their revenue mix is from information services and banking services and within information services they are distributed across transportation, energy and telecommunications. No revenue from any customer of any segment exceeds 10% of the Company’s consolidated revenue.

- Some of the sectors they operate in are less dependent on economic cycles (Ex: Telecommunications)

- Their diversified revenue streams mean any sector or customer from any individual segment has less effect on the overall revenue mix

- Cass’s business model is built on providing essential services to its customers, which has helped the company maintain its revenue stream even during challenging economic conditions.

2022 will be their best year yet as comparable growth for every quarter was at least 15% and EPS growth was at least 20%. I for one will be eagerly awaiting their next earnings release to see if this trend continues.

Balance Sheet

The company has been very good at maintaining a clean balance sheet.

- It is debt free and has held no long term debt for more than 10 years

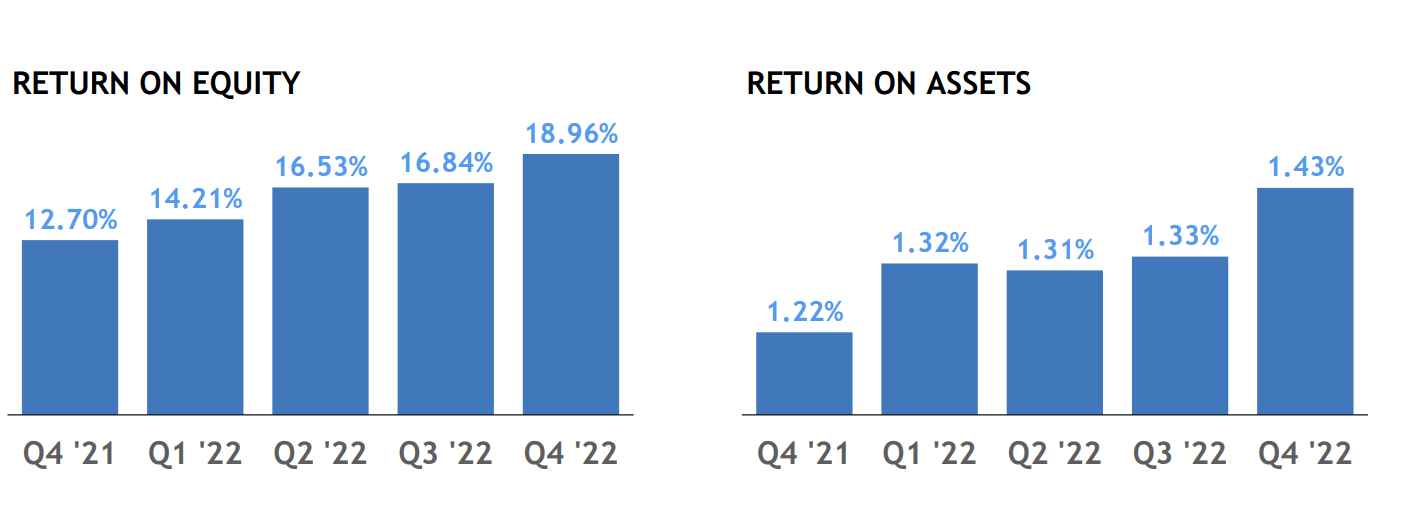

- Bringing their balance sheet and income statement together, high return on assets and return on equity are recognized as hallmarks of Cass

Company investor presentation

-

Zooming in on their banking arm, they have seen good organic loan growth in their most recent quarters and have not incurred a loan charge off since 2015

-

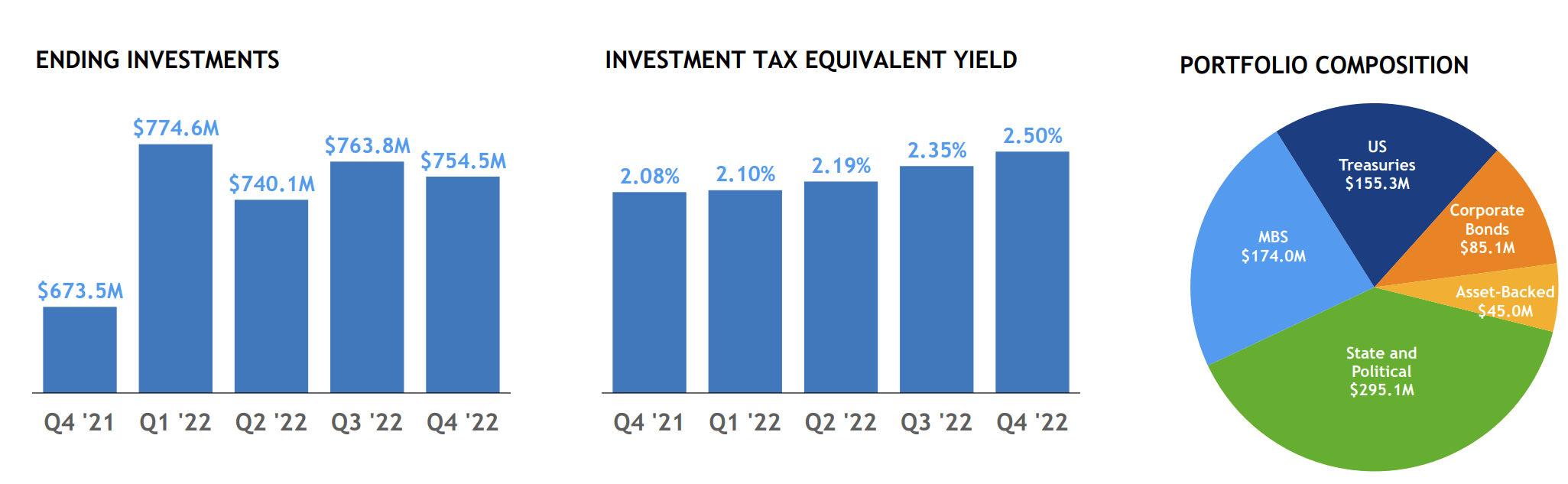

They have a high quality investment portfolio and are expected to benefit in a rising rate environment

Company investor presentation

Rewarding shareholders

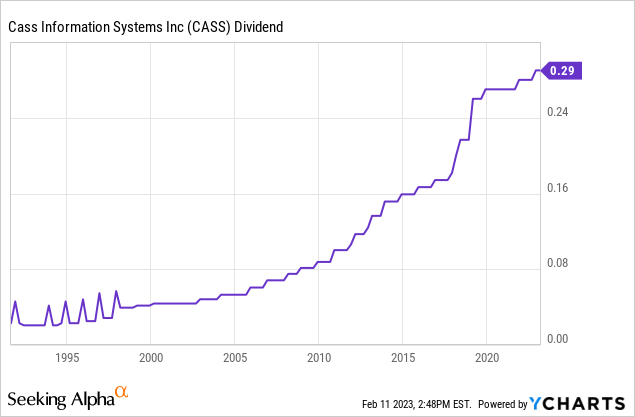

Another win for consistency is their regularly scheduled dividends that has been unbroken since 1934! Their dividend payments have increased over the last ten years and currently the yield stands at 2.3%. With a reasonably low payout ratio, its dividend payments are well covered by its earnings and cashflows.

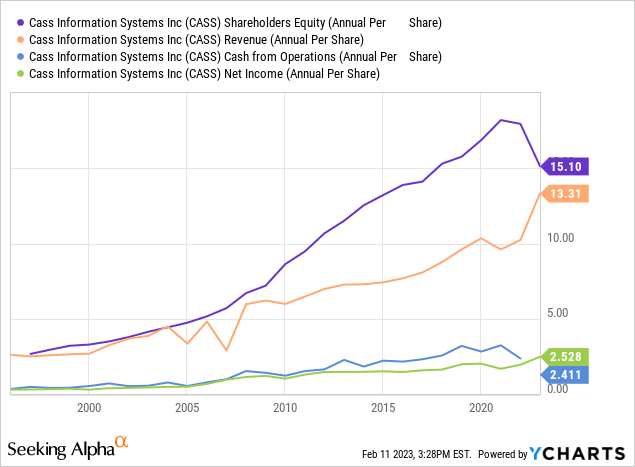

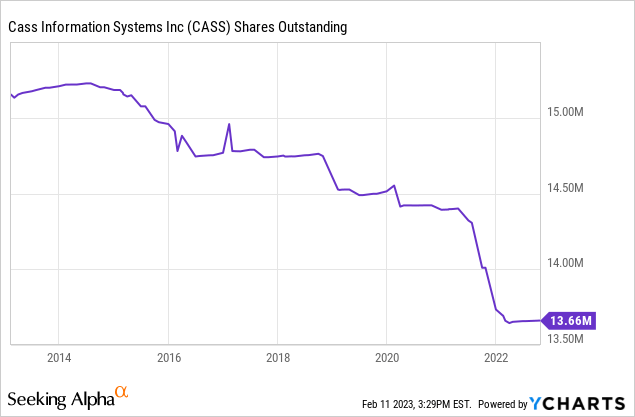

Another way I like to see if I am being rewarded as a shareholder is looking at my share of the pie and it is clear that this has been trending up in all these years. This is also helped by the fact that the company has been buying back its stock and has reduced its share count significantly over the last decade.

Low Beta

I try to look at this for every long term investment I make and its mainly because I hate to have my portfolio over exposed to market movements. Although I have high beta stocks in my portfolio, I try to diligently balance this out for stocks that are less exposed to the market volatility. Cass has a 24-month beta of 0.57 and a 5 year beta of 0.6, which suggests that this would provide the much needed cushion against market movements. Of course this is not the only metric that defines an investment and that is the reason I attacked this investment from multiple angles and concluded that this would indeed suit my portfolio.

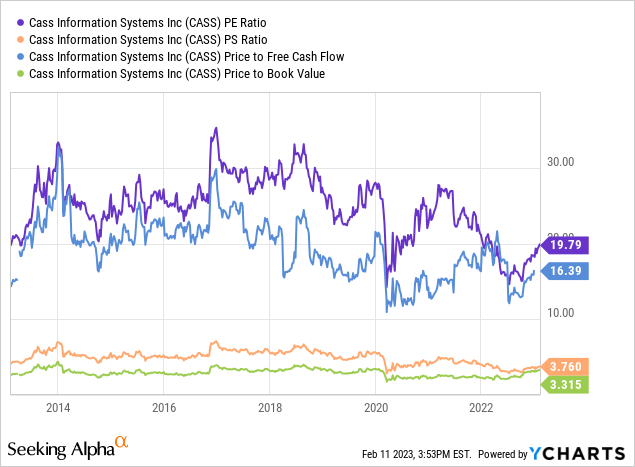

Is this a buy now?

Looking at its valuation ratios, we see that it has not changed much over the last 10 years but during this time we saw every underlying metric significantly move up. This is quite favorable to see and suggests that it would continue to get attractive from a valuation standpoint if this trend continues. I will be adding CASS stock to my portfolio and hope to benefit from its growth, dividends and low exposure to the index.

Be the first to comment