Joe Raedle/Getty Images News

The party that started for Carvana Co. (NYSE:CVNA) in March 2020 has well and truly come to an end. From $30 during the Covid crash, CVNA stock surged to $360 in August last year – highs unlikely to be tested in the foreseeable future, if at all. The unique car vending machines and the seamless online shopping experience offered by the company quickly got the attention of not just car shoppers but investors as well. The company, however, was simply not ready to deal with macroeconomic challenges that came to light with the reopening of the economy. Today, Carvana’s future seems to be hanging by a thread, and it’s hard to find Carvana bulls in the market as well. The objective of this analysis is to evaluate whether Carvana can still make it out of the woods in one piece.

Why Did Carvana Stock Drop Over 90%?

The initial decline in Carvana stock was fueled by the news of weakening auto sales demand. As an online used car retailer that operates in 311 metropolitan markets across the United States, Carvana, similar to other car dealers, will naturally face challenges when demand weakens. Investors need to take a step back to understand what worked for Carvana to get a better understanding of what went wrong for Carvana.

Carvana offers an online platform where consumers can research and identify a vehicle, inspect it using 360-degree vehicle imaging technology, get financing and warranty coverage, buy the vehicle, and schedule delivery or pick-up. The company is also known for its multi-story car vending machines, with 33 vending machines operating in the United States. As physical dealerships were closed at the height of the pandemic, the company experienced rapid growth. In 2020, Carvana became the second-largest online used-car retailer in the United States. Additionally, there was an increase in demand for used cars during the pandemic as auto production was slowed due to supply-chain constraints, which caused used-car prices to soar.

Prices of used cars have been falling sharply from their peak this year as global supply chains began to normalize, reducing the margins of used-car dealers. Carvana reported in early November that sales volumes fell by 8% due to rising interest rates increasing the effective monthly payment for most car buyers as well. The company also said in a filing with the Securities and Exchange Commission in November that it is laying off around 1,500 employees following previous rounds of cost cuts to boost its finances as demand for used cars declines.

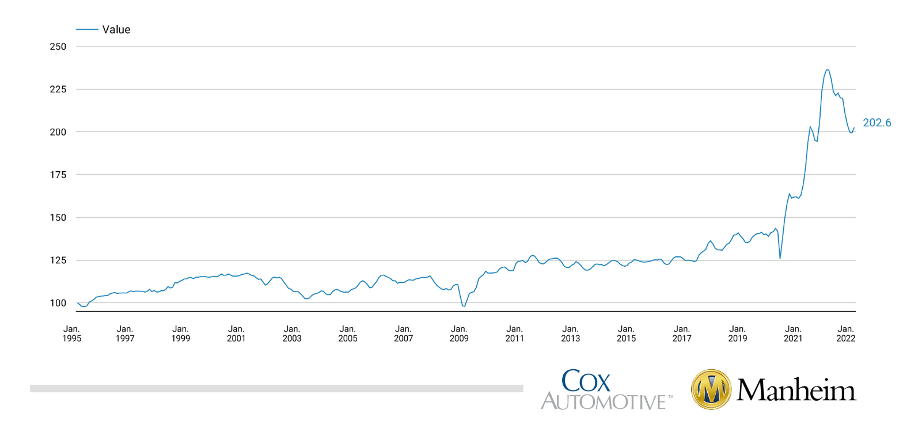

Exhibit 1: Manheim Used Vehicle Value Index (December 2022)

Manheim

Falling used car prices reveal the tip of the iceberg. Carvana’s business is facing fundamental challenges as well, and Mr. Market has not been oblivious to these developments.

One of the biggest problems the company is facing stems from the weakening securitization business. The company sells its finance receivables without keeping them on the books and realizes a gain/loss from this securitization process which is recognized immediately. Here’s a note on this business practice from Carvana’s third-quarter 10-Q.

The Company sponsors and establishes securitization trusts to purchase finance receivables from the Company. The securitization trusts issue asset-backed securities, some of which are collateralized by the finance receivables that the Company sells to the securitization trusts. Upon sale of the finance receivables to the securitization trusts, the Company recognizes a gain or loss on sales of finance receivables.

With interest rates rising at a record pace, Carvana now faces difficulties in securitizing its receivables. In Q3, Carvana reported a gain of $126 million from loan sales in comparison to a gain of $191 million in Q3 2021. Although these numbers might seem insignificant compared to the $3 billion+ quarterly revenue generated from retail and wholesale vehicle sales, a closer look at the company’s financials reveals that gains from loan sales account for a major share of its gross profit. To add some color, more than 35% of Carvana’s gross profit in 2021 was contributed by the securitization business. Interest rate hikes have had a double whammy on Carvana’s financial performance this year by discouraging used car buyers and negatively impacting the securitization business.

Carvana’s troubles do not end here either.

The company has come under the scrutiny of regulators because of title transfer and registration issues. According to Maryland Motor Vehicle Association, Carvana accumulated 386 late title fee infractions between June 2021 and July 2022, leading to a fine of $17,121. Last November, Carvana was banned from performing motor vehicle titling and registration actions in Philadelphia and Bridgeville. The company has faced similar issues in North Carolina, Kansas City, Michigan, and Florida as well. Carvana has acknowledged these challenges but many customers are yet to receive their state license plates, meaning that the company is still working on resolving these issues. At a time when the company is already facing challenges, these title and registration issues will only harm the brand image of Carvana.

All these reasons coupled with the deteriorating investor sentiment toward growth stocks have played a part in Carvana losing more than 98% of its market value this year.

Can Carvana Recover?

The company reported a loss of $2.67 per share for the third quarter compared to an expected loss of $1.94 per share. Revenue declined 2.6% YoY to $3.39 billion and nearly all metrics of Carvana’s financial performance including retail units sold came in well below the numbers reported last year. The gross profit per vehicle fell to $3,500, resulting in a 31% drop in gross profit to $359 million. With vehicle prices continuing to decline, the company is likely to report another fall in gross profit per vehicle in this quarter as well. Net losses increased dramatically in the third quarter and the company is now laying off more workers in order to achieve better margins in the coming quarters. The financial performance of the company is unlikely to show any improvements in the next few quarters because of a few reasons.

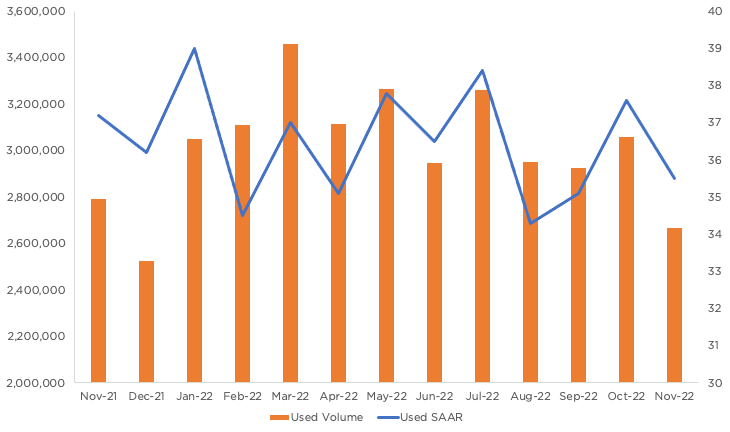

The Manheim Used Vehicle Value Index, which tracks the prices of used vehicles sold at its wholesale auctions in the United States, has dropped 14.2% this year through mid-December. According to Cox Automotive estimates, the used car market will end the year down more than 12% from the 40.6 million used vehicles sold in 2021. Total used-vehicle sales in November were estimated to be close to 2.7 million units, a 4.5% YoY decline. Carvana is likely to book losses as the company clears its inventory at a time when used car prices are giving back recent gains.

Exhibit 2: Used car sales volume and the seasonally adjusted annual rate

Cox Automotive

The interest-rate environment is not helping either, and the company is likely to report a further deterioration in gross profit margins before seeing any improvements in the long run.

Carvana took loans to fund its expansion plans and operations, including the all-cash $2.2 billion acquisition of ADESA’s U.S. physical auction business from KAR Global in May. As previously stated, Carvana expanded rapidly during the pandemic because customers shifted to hassle-free online purchasing and home delivery. Carvana lacked the resources or vehicle inventory to keep up with the surge in consumer demand, prompting the company to purchase ADESA and a record number of vehicles at exorbitant prices. In a previous earnings call, Carvana CEO Ernest Garcia acknowledged this and said, “we built for more than showed up“.

Carvana’s business is built on marketing, so the company will have to continue spending on marketing to remain relevant even in this economic downturn. Although recently-announced cost-cutting goals sound promising, they will not be sufficient to change things around for Carvana. Carvana has sufficient liquidity to survive the next few quarters, but investors should not be surprised if the company taps into capital markets in 2023 to keep the company afloat. The company carries over $6 billion in long-term debt, and looking for more credit or diluting shareholders will not look good if it comes down to that.

Carvana’s mission of changing how people buy used cars is promising and attractive, but the company is unlikely to recover meaningfully in the next 12 months.

Is CVNA Stock A Buying Opportunity?

With no sign of recovery in the foreseeable future, many Wall Street analysts have downgraded CVNA stock. All hope is not lost, however. Investors should carefully monitor how Carvana executes its turnaround plan in the next few quarters, in particular how the company streamlines its business by focusing on efficiency gains. The company management’s attitude toward growth should also be monitored carefully as empirical evidence suggests Carvana has gotten ahead of itself in the past. The next couple of quarters will give a good indication of how Carvana will survive this downturn – if at all – and how the company will perform in the next phase of the business cycle. For now, I will avoid CVNA stock as things will likely get more difficult from here before we see any improvements.

Be the first to comment