Joe Raedle

Carvana Co. (NYSE:CVNA) shares are popping 40% premarket today on July 19th after reporting a small positive “adjusted EBITDA” number along with a massive debt swap deal to restructure debt.

If you’re an equity holder that views this as a long-term investment, rather than just a trade hoping for a short squeeze, I’m not sure how this is viewed as good news.

Quick Take on Valuation

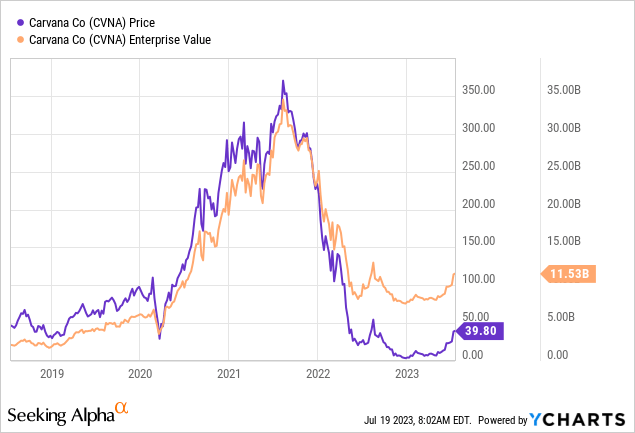

I won’t go too deep here because this article is primarily about the debt swap, but I want to touch on valuation for just a second. Yes, Carvana is still far down from its all-time high, and below where it traded pre-COVID. But you have to look beyond the stock price and see its Enterprise Value is still way above where it was in 2019.

In 2019, Carvana had 46.8 million outstanding shares. Now, they have more than 106 million, and that number is set to increase dramatically again. Net Debt is also up substantially, from $1.45 billion in 2019 to $8.2 billion now.

Quick Take on Q2 and “Positive Adjusted EBITDA”

Despite all the positive headlines this quarter, they still posted a GAAP loss of $58 million, and this is after a benefit of $70 million of non-recurring items, per the company.

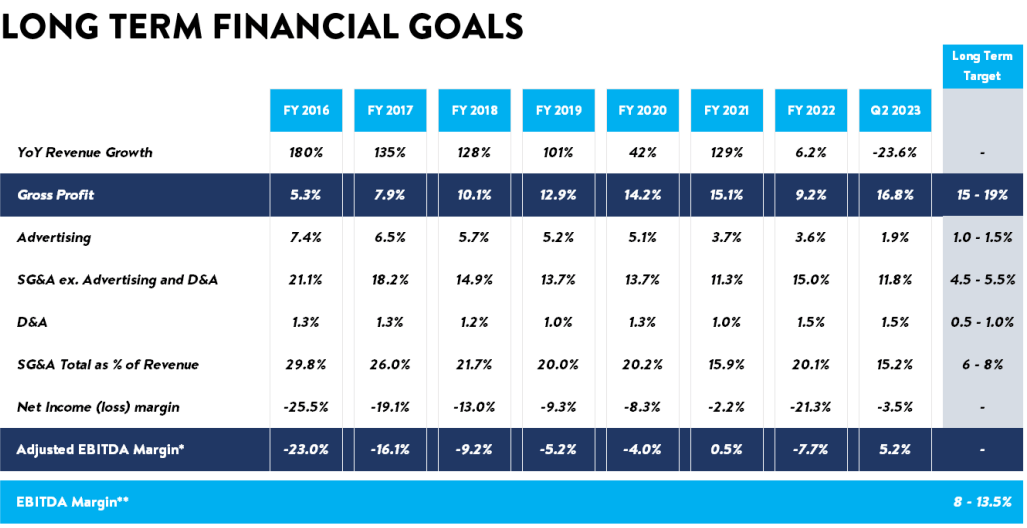

Carvana Long Term Goals (Carvana Investor Relations)

Digging deeper, to do this, they cut their advertising budget to a level not seen ever in their corporate history, along with large cuts to non-advertising SG&A. How excited should shareholders be for this? Any company can cut near-term spending to the bone to make the current quarter look better. This hardly looks like a sustainable positive change in operating fundamentals.

The Debt Swap

The press release on the debt swap deal sure sounds positive, which is likely a big part of the reason the shares are up so much pre-market. From the press release:

Carvana entered into a transaction support agreement with a group of noteholders representing over 90% of the aggregate principal amount outstanding of the retailer’s existing senior unsecured notes. The deal will reduce cash interest expenses by $430M per year for the next two years.

Sounds great, but why would the debt holders agree to this? For real details, you need to look at the SEC filing, because it’s ugly.

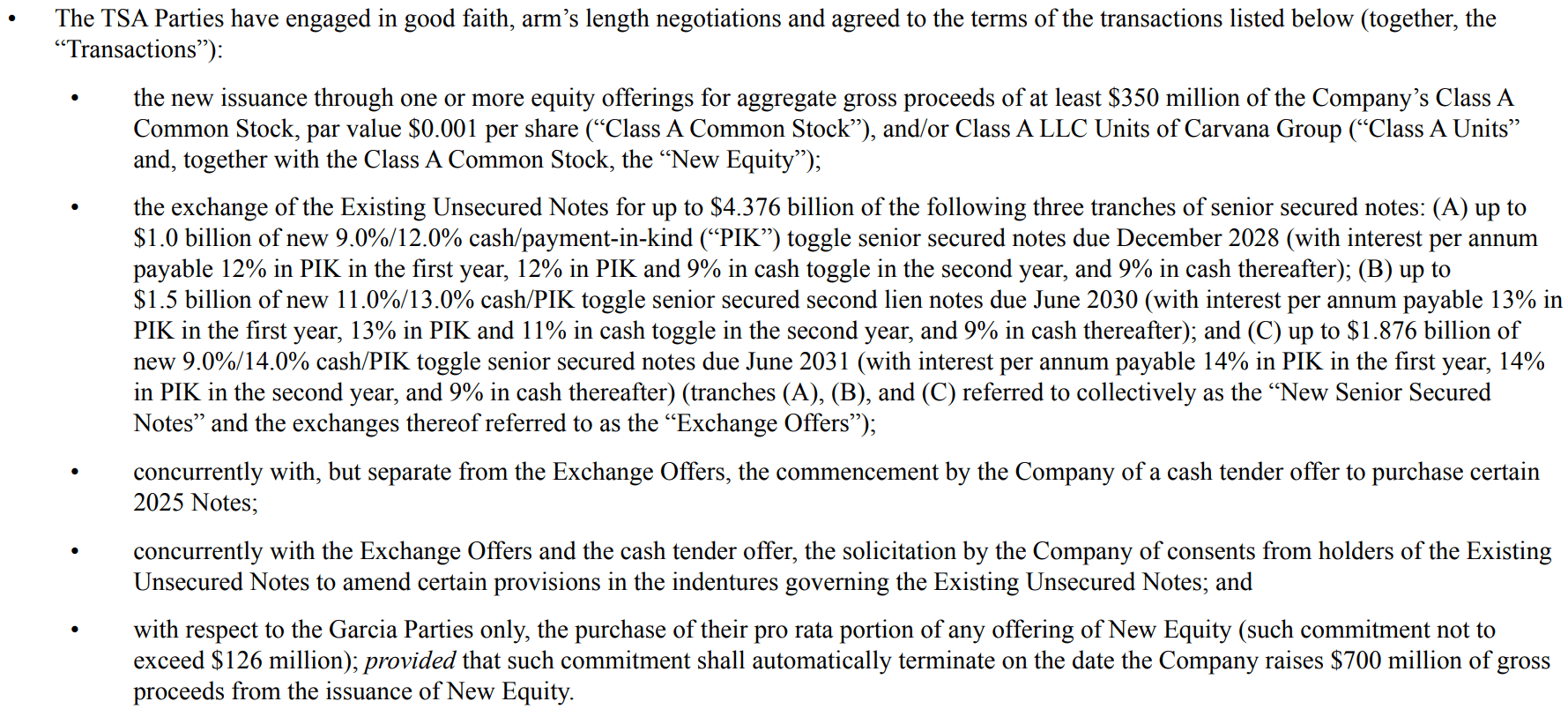

Debt Swap Terms (SEC Filing)

The exchange pushes the maturity dates out a few years, but drastically increases the interest rates, from 4-6% up to 9%. The company agreed to this because the new notes allow the company to “Pay in Kind” for the first 2 years, which means that the debt holders agree to receive more debt instead of a cash payment, but at even higher rates: 12-14%!

This is like a credit card company agreeing to charge you a higher interest rate on your balance for 2 years, in exchange for not charging late fees or reporting you to the credit agencies.

GAAP interest charges for Carvana will be going significantly higher as a result of this, but cash going out will lessen for the first two years.

With all of this, the company also announced they are selling 35 million new shares “at the market” almost $2 billion worth at the 8:30am premarket price of $52. The Garcia parties have agreed to purchase a small portion of it, but it is a pittance compared to what they sold near the top 2 years ago.

This is a fantastic deal for Carvana’s debt holders at the expense of the equity holders.

Conclusion

Whether this morning’s results are going to induce a massive short squeeze, I do not know. At least in the premarket, it sure looks like it.

I do know that this is a company that has only had one quarter of profitability since 2015, that operates in a competitive, low margin, moat-less business, that just accepted a deal that doubles the interest rates on outstanding debt (and nearly triples it for the next couple years while it is paid in kind.)

For anyone holding Carvana, this looks like a golden opportunity to sell, before the company begins to issue shares.

Be the first to comment