Serjio74/iStock via Getty Images

Railroads are well known for having moat-worthy characteristics, and while Union Pacific (UNP) and CSX (CSX) generally come to mind, Canadian National Railway (NYSE:CNI) is also worth being on the radar. CNI recently released its fourth quarter results, and in this article, I highlight whether the stock is currently a buy or hold, so let’s get started.

Why CNI?

Canadian National Railway is a leading rail operator that is literally economically essential, transporting more than 300 million tons of natural resources, manufactured products, and finished products through North America annually. It’s been in existence since 1919, and derives its moat-worthy positioning from being the only railroad connecting Canada’s East and West coasts with the American South through its 18,600-mile rail network.

Notably, CNI recently announced a strategic partnership with Union Pacific (UNP) and Norfolk Southern (NSC) in the EMP Program (Equipment Management Pool). Fellow SA contributor sees advantages in the formation of this partnership, noting as follows in a recent article:

The EMP program is an interline service that enables shippers to use more networks, providing seamless access to most of the major cities across the whole North-American continent, from Canada to Mexico. I think this move is an important strategic move that aims at making Canadian National strong against Canadian Pacific (CP). It really gives access not only to three different hubs on three coasts, but to all major hubs and cities across all the main commercial routes of the continent.

CNI just delivered a solid Q4, with revenue growing by 21% YoY to C$4.5 billion, with 6% higher RTMs (revenue per ton mile). This was driven by very strong volumes in Canadian grain, including an all-time single month record for tons shipped in October. Coal demand also remained high driven by a strong commodity pricing environment, with over 30 million tons shipped for the full year 2022. Lastly, Automotive volumes were strong as supply chain bottlenecks due to chip shortages early last year eased.

Nonetheless, strengths in the aforementioned categories were partially offset by a softening in international intermodal volumes. Signs of a manufacturing slowdown are also beginning to emerge, as there was lower volumes in chemicals and plastics used as feedstocks into manufacturing due to small outages and lower market demand.

Remarkably, through all this, CNI was able to maintain a stable margin profile, with operating ratio unchanged at 57.9% from the fourth quarter of 2021. The big story, however, is the soft guidance that management provided for the current year, guiding for low single digit EPS growth on softer economic outlook. This sent the shares down to $120 in aftermarket trading.

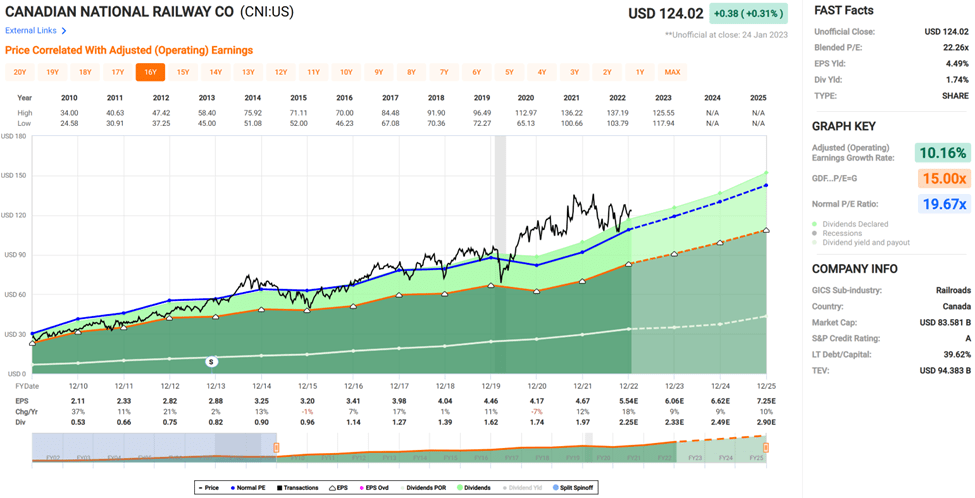

Considering the weak outlook, I find the shares to be expensive at the current price of $124 with a forward PE of 22.1, sitting above its long-term normal PE of 19.7. As such, I’d be more interested in the stock after a 10% to 15% pullback in price from current levels.

Nonetheless, CNI remains a shareholder friendly company, raising its quarterly dividend by 8% to C$0.79, translating to USD $0.59 and a 1.9% dividend yield. The dividend is well-covered by a 37% payout ratio and comes with a 5-year CAGR of 12%. Management also announced a C$4 billion share repurchase plan. However, buybacks at the current price aren’t all that accretive due to the elevated valuation.

CNI Valuation (FAST Graphs)

Investor Takeaway

Overall, Canadian National Railway remains a strong rail operator with an economically essential business. With the EMP partnership on the horizon and high grain and commodity shipments, CNI should be able to balance out softness in other segments of its business. That said, the manufacturing segment is starting to show cracks and that could result in weak earnings growth for CNI in the near term. As such, at current prices, I believe investors should wait for a pullback before buying in.

Be the first to comment